Jagoinvestor

Jagoinvestor

May 27, 2013

May 27, 2013

SBI MaxGain Home Loan Review – With FAQ’s

In this article we are going to share SBI Maxgain Home Loan review with you. Now a days many home loan borrowers are opting a particular type of home loan from State Bank of India which is called Max Gain because it has many advantages compared to other kind of home loan scheme’s. In this SBI Max Gain home loan, an Overdraft (OD) account is assigned to the customer’s home loan & any amount parked by customer is treated as loan repayment for the purpose of interest calculation, for the days, the amount stays there in that OD account. As on date following banks are offering similar types of home loan to their customers. I would like to thank to Mr. VKS Nathan who gave the Idea of this article.

SBI, IDBI, CITI, HSBC & Standard Chartered. Punjab National Bank can also be added in this list but it’s offering a combo of normal loan + Overdraft. In this article, we are going to discuss only SBI Max Gain as in OD linked home loan, the maximum business is with SBI & the most discussed topic on Jagoinvestor Forum is also related to SBI Max Gain Scheme

What is an Overdraft account?

Before we discuss Max Gain, first understand, what is an Over Draft Account? All of us are well aware of functioning of an ordinary saving bank (SB) account. Here account operates between zero to positive & positive to zero. As we deposit our money, it’s used by bank & we get interest on our money from bank. In case of an OD account, bank first ask for a security & then assign a credit limit on the basis of the market value of that security. This security may be Fixed Deposits, Insurance Policies, National Saving Certificates, Shares, Mutual Fund units, house/commercial property etc. Now when we are using this assigned credit limit, the amount is going from zero to negative zone & when we are repaying, it’s coming from negative to zero. As we are using bank’s money in this case, the interest ‘ll be paid by us to bank. That’s how an OD account works.

So what is the correlation between Max Gain home loan & Over Draft account?

For Max Gain borrowers, State bank of India opens an Over Draft account where the Credit limit as discussed above is equal to the loan value assigned to the borrower. Here underlying security is the home you have purchased or constructed from that loan amount. Now as & when you are parking any surplus amount into this OD account, the parked amount is treated as payment towards loan (effectively you are bringing down your loan liability from negative towards zero position) and thus the interest ‘ll be charged only on the difference amount i.e. total loan amount – parked surplus amount.

What is the primary benefit of SBI Max Gain Scheme?

Well the primary benefit of MG is to keep your liquidity intact & still bringing down your interest outgo. To understand it better, please imagine a situation you are running a home loan of 30L Rs. & now you do have 2L Rs. with you to prepay. In normal home loan, your 2L Rs. ‘ll be accepted by bank & adjusted towards home loan & your amount is gone forever so no liquidity for you of that 2L Rs. amount. On the other hand, if you are MG customer, simply park those 2L Rs. in your MG account & your interest outgo ‘ll be lower from that month itself till those 2L Rs. or a part of it is there as surplus in MG account.

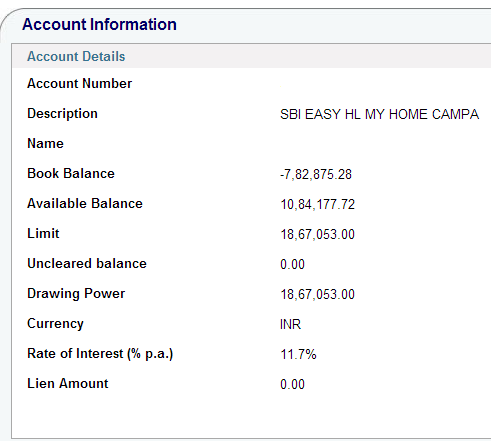

What is Drawing Power ?

Drawing Power is nothing but your as on date actual outstanding loan amount. Before final disbursal or start of loan repayment, it’s your sanctioned loan amount. Once your EMI starts, it’s your as on date actual outstanding loan amount. Please check Image below, Drawing Power here is 1867053 Rs. as on date. (Click here to understand it better)

What is Available balance?

Before final disbursal, it’s the sum of undisbursed amount + parked surplus & post final disbursal, it’s your parked surplus amount which is available to withdraw. Please check Image below, Available Balance here is 1084177.72 Rs. as on date. (Click here to understand it better)

What is book balance?

It’s the adjusted loan amount arrived after deducting the Available Balance amount from Drawing Power. In your account statements it’s shown with a negative sign. Please check Image below, Book Balance here is – 782875.28 Rs. as on date. (Click here to understand it better)

Is there any extra interest for Max Gain?

No, the interest for home loan is same in SBI be it for normal home loan or for Max Gain.

I’m an existing SBI home loan customer. Can I convert my old term loan to Max Gain?

Yes, you can. Please contact your loan serving branch or RACPC for the required paperwork to be done. This may be an outdated info so please do check with your loan serving branch for current day rules on conversion.

I have taken the Max Gain for an Under Construction Property. Can I park surplus amount to save on interest outgo?

The answer is yes & no both. Yes you can park your surplus during under construction phase but do remember SBI is disbursing partially at this juncture & in case due to any emergency you want to liquidate your surplus, SBI ‘l not allow the same. so park only that much surplus, you feel you ‘ll not need even in an extreme emergency.

If I’m parking some money on monthly basis or in lump sum, will my loan term come down or EMI go down?

No. Neither your EMI ‘ll come down nor your loan term. The only saving is in terms of interest outgo. To understand it better, Let’s assume a test case of loan amount 30L Rs. @ 10% Rate of Interest for 20Y term. The normal EMI for these nos. ‘ll be 28951 Rs. The break up of your EMI for first month ‘ll be 25000 Rs. interest & 3951 Rs. for principal repayment.

Now if you do have 2L Rs. surplus in the very first month & prepay the same as below –

Case – 1 Normal home loan

Your 2L Rs. is gone & outstanding loan amount ‘ll come to 2796049 & interest outgo ‘ll still be 25000 Rs. but the no. of months ‘ll come down from original 240 to 198 months.

Case – 2 Max Gain home loan

Your 2L Rs. are parked in that OD account & the interest for the very first month ‘ll be calculated on 28L Rs. & thus it ‘ll be 23334 & thus there‘ll be an interest saving of 1667 Rs. which‘ll remain available in your OD account as surplus along with your parked surplus 2L Rs. so for next month, the parked surplus amount ‘ll be 201667 Rs.

Please do note in case 2 above, Your loan term is still 240 months but the saving of interest ‘ll keep on increasing on mly basis from the parked surplus & of course the liquidity of those 2L Rs. is there.

How can I calculate my saving in Max Gain?

To know your actual saving, first of all please demand a loan amortization schedule from your loan serving branch & now for each month compare the scheduled interest outgo as per your loan amount. schedule & the actual interest outgo.

What should I do to maximize the savings in Max Gain?

If you are paying your EMIs from SBI’s SB account, you can maximize your benefits. How? here it goes. Say 15th is the EMi date on which EMi amount is debited from your SB acct. Now in a normal home loan, people ‘ll keep at least 2-3 months’ EMI amount as buffer in SB account. but in case of Max Gain, you do not need to keep buffer in SB account. Keep this buffer amount also in your MG account along with your routine surplus amount. now use the power of net-banking of SBI for your own good & create a schedule transaction of your EMI amount 28951 Rs. (in the above example) to be transferred on 13th of every month from MG account to SB account. At a time you can schedule for next 12 months by using standard instruction. So it’s technology that’s helping you.

I can transfer to MG account from my existing net-banking enabled SB account but reverse is not happening. why?

The answer lies in the fact that Net-banking transaction rights on your MG account is not enabled yet by your loan serving branch. if final disbursal is done, you can apply for transaction rights. if only partial disbursement has been done, sorry, you can’t apply for transaction rights till final disbursal.

Is it mandatory to purchase property insurance & life insurance along with Max Gain?

Having property insurance as well as sufficient life insurance is compulsory but purchasing the same from SBI’s sister cos. like SBI General ins. & SBI Life ins. is not at all mandatory. if you feel that policies are being cross sold to you to exploit your position (home loan seeker), please contact the AGM of your local RACPC where your loan application is under processing.

Is SBI charging higher processing fee for Max Gain?

No, as on date there is no differentiation in fee for term loan & Max Gain but SBi reserves the rights to charge different fee.

Can I claim section 80C principal repayment benefit for the surplus amount parked in Max Gain?

The answer is NO. Only the regular principal repaid by you from your EMI as part of your loan amortization schedule is available for tax benefit under section 80C. the parked surplus amount is liquid money & you can withdraw it any time, hence it’s not considered as actual repayment of loan & thus not eligible for tax benefit.

Can I avail cheque book & ATM card for my Max Gain account?

Yes, as & when you‘ll demand these, SBI ‘ll offer you the same. In case you are already holding an SBI SB acct. linked ATM card, you have the option to link your MG acct. also with this existing ATM card.

Can I enroll my MF SIPs in Max Gain?

Yes but do note, there should be a surplus balance i.e. available balance on the date of SIP, else your ECS or SI mandate ‘ll bounce.

Can i pay for my utility bills, credit card payments, online shopping from Max Gain?

Yes, you can do all this & more. In fact it’s in your best interest that you treat your MG account as your primary money parking account & route all your transactions through it so that money is lying there for maximum possible time & thus helping you to bring down your interest outgo.

I used my MG account ATM card to withdraw cash from other bank’s ATM & I was charged the money very first time in the month. Why?

The reason is, as per RBI’s circular 5 transactions on other banks’ ATM are free only for SB account & in this case, you forget the point that your MG account is not SB account. it’s an overdraft account.

For an imaginary situation, my loan amount is 30L Rs. & parked surplus amount is also 30L Rs. Does it mean, my loan is closed & I can claim my property papers from SBI?

No, your loan is not closed. Only interest outgo ‘ll become zero & EMi ‘ll remain continue as it is. Yes the interest part of your EMI ‘ll keep on accumulating in your MG account. If you want to close your loan at this point, you w’d have to inform SBI in written & now SBI ‘ll adjust your parked surplus amount towards the outstanding loan amount. you ‘ll lose the liquidity of your money but loan ‘ll be over & now you can get your property papers back.

How can I transfer my loan from other banks to SBI Max Gain?

For loan transfer, first of all contact your existing lender & ask for following things.

- Loan Account statement from day one.

- List of Documents, which were submitted by you at the time of availing original loan. In day to day language of bankers, it’s called LOD.

- As on date outstanding loan balance with applicable interest, penalty & any other fee to close the loan.

Now contact, the nearest SBI Branch (if you do have an existing SB account with SBI, it’s advisable to contact there for ease of operation). Inform in that branch that you want to transfer your loan from existing bank to SBI Max Gain. fill the application form, submit the necessary papers & SBI’s RACPC ‘ll do the back ground job.

Once SBI is ready to accept the transfer, it ‘ll issue you a sanction letter of the loan amount & ‘ll ask you to go for loan related agreement documentation work with SBI. If you are not having property insurance, SBI may ask to purchase one. Same ‘ll be the case for your life insurance. Once legal documentation is over, the cheque of the loan balance ‘ll be issued directly into the name of the bank in question. After the amount is credited to your existing bank, within next 20-30 days, you ‘ll get the original documents submitted by you, from the existing bank. Now you w’d have to submit these documents to SBI. In some states like Gujarat, Maharashtra, Karnataka, SBI may ask to go for registration of mortgage deed on your property in the office where your property was originally registered in your name.

|

SBI Max Gain |

Normal Home Loan |

|

Liquidity of your part prepayments is there |

No Liquidity. Money is gone for ever, once you prepay. |

|

A bit complex to understand |

Easy to understand |

|

For people who can generate regular surplus amounts |

For people who can only manage regular EMIs |

Click here to know the real life example of Mr. Sudhir S for SBI Max Gain.

Do you feel, this article was able to answer your all queries related to SBI Max Gain? Was this article helpful for you to understand the overall concept of SBI Max Gain home loan? Please feel free to ask for more help

This article is written by Ashal Jauhari, who manages a great facebook group on investments and also is one of the most active and helpful member of our Jagoinvestor forum. This article was written by him and reproduced from this blog here

I have taken ani maxgain loan in Oct.2013.on 30th may my available balance is504920 and limit is 1480000,but when I checked on 31st May, my available balance is 492396 and limit us 1868000.I have not performed any transaction.Then how can bank debit amount from available balance with information to me.How can I get the debited amount from available balance.As the bank officer say every year limit is changed.kindly guide me so that my available balance is same at the date of 30th May.can bank cut the amount directly without permission of loan holder

May be its due to change in interest rates..

I have a specific query regarding Max-gain home loan. I took a home loan of Rs 2500000 in Sept’2019. Emi started from OCT’2019 for 24600. Till now i have paid 28 EMI’s and total principal deduction from home loan is just 113815. I am surprised as this should have been atleast 2.5 lakhs as per the regular home loan interest payments. Bank manager is unable to provide any satisfactory response.

Will the interest that is accumulated for the surplus amount in over draft account is taxable?

Dear Surya

You don’t earn any interest on Maxgain OD account. Hence, there is no question about interest on surplus being taxable.

However, your interest outgo reduces in Maxgain OD account on the basis of the surplus amount. Which means that you cannot claim tax deduction on the saved interest portion as you have never paid this interest to the Bank.

Regards

Anuj

I have purchased under contruction property, which deliver to me on Dec,2017. I have parked 3L surplus on my SBI max gain Account.

Can i claim as tax benefit under 80C as principle repayment.

If No, how can convert this surplus amount to principle repayment to claim tax benefit.

Please suggest

No you cant claim it under 80C

I could see that current rate of Interest for Max Gain is 9.15% for new joiners. For me it still says 9.35% which was decreased few months ago. Can you please confirm how to reduce my existing interest from 9.35 to 9.15% . Any help would be appreciated.

I consider this as one of the worst.

Since they charge 4.8% for depositing into the maxgaining account. I transferred 16000 from my saving acc to OD account I ended up paying 710 rupees as charges.

The interest rate doesn’t decreases when RBI decreases. You need to pay 0.567% of total loan amount to change the interest rate. Then the SBI MICLR rate will decrease to that’s all.

Thanks for your comment sreekanth s v

Do they charge 4.8% each time you deposit money to the Maxgain account, as Srikanth is saying. If so who will take Maxgain loan?

Dear srrkanth s v

SBI doesn’t charge anything for deposits or withdrawals from Maxgain OD account. The Rs. 710 you have been charged must be for something else. Please verify your OD and SB account statements.

All the banks and HFCs charge conversion fee for converting the spread. This is not unique to SBI.

Regards

Anuj

My Maxgain started from August my loan is 3545000, my available balance on 29Aug2016 was 430018, on 30th Aug2016 i removed 15000 from my Available Balance, So the amount in Available Balance became 415018, 31Aug2016 interest gone was 25189, on 3Sep2016 EMI gone was 29809. My ROI is 9.5 %. My DP is 3531000. My question is why my Available Balance is 406435 whereas it should be 415000 after my EMI on 3rd Sept?

Looks like you need your bank to clarify on this.

Thanks for reply..will check.

Dear BhushanA

Your calculation is correct but please check your OD account statement. It might be that SBI has debited loan/property insurance premium from your OD account.

Regards

Anuj

Dear Sir,

Appreciate your time and valuable advise you give to all the people here.

SBI maxgain Homeloan amount 56lacs, EMI 55000 for 20yrs with current ROI 9.7%. Till date I have parked around 8lacs of surplus amount in my home-loan account in bits and pieces and not lump-sum. With my increased salary, I can park more amount than my EMI in my SBI Maxgain Home loan account. Current EMI 55000 and I can add 30000 more to it. Current outstanding is 53lacs excluding the 8lacs surplus amount.

My Questions:

1. Shall I withdraw the 8lacs surplus amount and deposit it back as a lump-sum, if so what benefit will it give me.

2. Can i adjust it towards principal and reduce tenure? If so what benefit will it give me?

3. Shall I increase my EMI to reduce the tenure? if so what benefit will it give me?

4. Can I deposit lump-sum and increase EMI both at the same time and decrease my tenure? if so what benefit will it give me?

4. Or I shall continue parking the surplus 30000 in maxgain account without changing the EMI?

It would be very helpful to hear your valuable advice on my queries.

Thanks in Advance

Aztek

Dear Aztek

1. Shall I withdraw the 8lacs surplus amount and deposit it back as a lump-sum, if so what benefit will it give me.

A: It will not make any difference apart from from loss of interest saving on for the period for which you withdraw Rs. 8 Lakhs.

2. Can i adjust it towards principal and reduce tenure? If so what benefit will it give me?

A: If you part prepay the principal and reduce the tenure assuming you keep the EMI same, your principal component from EMIs will increase and Interest component will reduce by the same amount. However, there will be no impact on the actual interest that gets debited from your OD account. Plus, you will lose the liquid balance of Rs. 8 lakh that you have.

3. Shall I increase my EMI to reduce the tenure? if so what benefit will it give me?

A: If you increase your EMI, of course the tenure will be reduced. In this case the principal component in your first EMI after the increase will be stepped up by the amount of increase. The interest component will remain the same. But now since you will be paying more principal in every EMI, the interest component will start reducing at a faster rate.

4. Can I deposit lump-sum and increase EMI both at the same time and decrease my tenure? if so what benefit will it give me?

A: You will see both the effects as explained above.

4. Or I shall continue parking the surplus 30000 in maxgain account without changing the EMI?

A: That’s totally up to you. Key consideration is whether you want to retain liquidity or not. In my opinion, the best way is to continuously increase the surplus balance till it is equal to the principal outstanding. Thereafter, you can use the surplus balance to close the entire loan. Else you can maintain the surplus balance in your account equal to the principal outstanding. In second case, your net EMI becomes Nil as the interest cost is zero and principal gets paid from the surplus balance.

Regards

Anuj

Thank you so much Anuj, This helps a lot. Appreciate your time and advise

Hi Manish,

I really appreciate your effort in helping the less knowledgeable folks like me in these financial matters.

I have already opted for SBI MaxGain Home Loan, but unfortunately at the time of enrollment I went for 25 years duration. Is it possible to change the duration mid-way?

Thanks for your help.

If you change your EMI, the duration will automatically get calculated ! ..

Thanks Manish. Appreciate the response.

Glad to know that Prateek ..

Hello ,

I just want to know , if it is good to close an existing MAX gain HL account ? I have surplus amount & i can pay it against outstanding loan amount . Will it be good/advisable to close this MAX gain account ?

Apoorv

If your accumulated surplus balance is equal to the principal outstanding, you can withdraw exactly the amount of EMI that you will be paying every month. Which means that it becomes a zero cost loan.

The decision that you need to take are:

1. Do you want to pay off all the principal amount to close the loan and reduce your liquidity?

2. Are you better off continuing with a zero cost loan. In this case, your withdrawals will be equal to the EMI and your accumulated balance will diminish to zero at the end of the loan team.

3. Do you want to maintain liquidity that may become necessary for meeting exigencies.

Please evaluate the above and then you should be able to take the right decision.

Regards

Anuj

Yes you can do it !

Hi,

For under construction houses, does SBI Maxgain allow the option of tranche emi? This will mean that the EMI will be calculated based on the disbursed amount, not on the entire project cost.

Hi Arjun

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

Arjun

One of my friends has taken SBI Maxgain loan for under construction house. She had shared her account statement and amortization schedule with me for some guidance. I noted three things:

1. She is paying full EMI calculated on the total loan amount.

2. Interest being debited from her OD account is only for the disbursed amount.

3. Principal is not getting debited from her OD account, and Principal deductions will begin next year.

Due to the above 3 things, she has already accumulated above Rs. 5 lakhs in her OD account, which is a very good thing. However, she will not be able to withdraw this amount till she gets all the disbursements and the transaction rights.

Your case might be similar to the above. For better clarity, please take the Amortization Schedule for your home loan from your branch.

Regards

Anuj

Raj

The first explanation is the correct one.

Regards

Anuj

Hi Sir

I kind of quite understood how max gain works after googling about it. I found two different versions of max gain account explanation regarding available balance and principal amount.

1. The interest saved goes to the available balance. Principal is same as in amortization schedule. Tenure and EMI remains same.

2. The interest saved reduces the drawing power. Principal is EMI – Interest debited for that month. EMI remains same, but tenure comes down.

Which of these two is true? Or SBI has both of these versions?

Hello Sir,

I have applied for Maxgain Home Loan of Rs.30,00,000 and it was approved and Rs.13,95000 has been disbursed to the builder. The property is still under construction and as I have opted for Full EMI, EMI is getting started from next month. There is Available balance of Rs.16,05,000 in my Maxgain loan account as this amount has not yet been disbursed to the builder.

Now my question is if I park surplus funds in my maxgain loan account, will I get interest on the surplus funds? If yes, how much interest will I get?

Dear Hanuman

SBI Maxgain account does not pay any interest on the surplus balance. Instead, the account “does not charge” interest on the surplus balance.

For eg. if you have withdrawn Rs. 13,95,000 from the OD account as disbursement, your account be debited by the interest on Rs. 13,95,000. Now, if you deposit some amount, say Rs. 2 Lakh in the OD account, then your will be debited by interest on Rs. 11,95,000. So you will be saving (not earning) interest cost on the Rs. 2,00,000 that you have deposited as surplus balance.

However, you can only deposit (and not withdraw) money in the Maxgain OD account till your disbursements are not complete. Hence, make sure that you deposit only the amount that you are very sure that you will not require till your disbursements are complete.

Regards

Anuj

I have home loan of Rs 25 Lakh, Amount of 24 Lakh is already transferred to builder. 1 lakh is remaining

I have deposited rs 2 lakh to my OD account.

I need to transfer the 3 lakh (1 lakh pending from full amount and 2 lakh from additional OD saving) to builder. Can I do that?

Pankaj

Since your loan is not fully disbursed, you cannot withdraw the amount you have deposited in the OD account.

You should ask your builder to give you a demand letter for Rs. 1 lakh. Get this amount disbursed. This will complete your disbursements for the home loan.

Thereafter, you can get the transaction rights for your OD account from your Bank branch. After you get the transaction rights, you can issue a cheque in favor of the builder or directly transfer the amount to his account through NEFT/IMPS.

Regards

Anuj

Hi Pankaj

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

Hi Anuj,

Whether available balance changes with drawing power? I could see that when my drawing power reduces, same amount get reduced from available balance. Can you please tell how this works?

Thanks for your answer

Best Regards

Manesh

Manesh

If you are not doing any transactions from the OD account, still the Available Balance will change.

Let me explain step by step:

1. Your Drawing Power at any time is the Total Principal Outstanding on your loan. It does not get impacted by the Available Balance.

2. At the time of monthly EMI credit, your Available Balance increases to the extent of EMI deposit. Drawing Power remains as it is.

3. When the Principal Component of the EMI is debited, your Drawing Power reduces (or you can say, the Principal Outstanding reduces). Your Available Balance reduces simultaneously to fund this Principal Component payment. This is the transaction that you are referring to.

4. At the end of the month, the accumulated interest cost for the month is debited from your account. This is funded by your Available Balance and hence the Available Balance gets reduced to the extent of Interest Debited. This transaction does not impact your Drawing Power as you have already paid for the Principal Component in transaction no. 3 above.

I have sent you my personal Maxgain calculator. Hope it helps. Let me know if need any help on that.

Regards

Anuj

Thanks Anuj for the detailed explanation and sharing the Max Gain Calculator.

Hello,

I have SBI maxgain home loan. I have received surplus bonus 3 lac and want to park it in SBI Maxgain home loan account.

Ques 1> If suppose I put this 3 lac in maxgain account I can withdraw it any time lets say after 1 month,1 year or 10 years? and after withdrawal the loan account will be have like normal and charge interest on entire outstanding? .

Ques 2> There are absolutely no charges for withdrawal of this parked amount?

Sagar

If you have the transaction right for your SBI MAxgain OD account, you can withdraw your surplus balance anytime you want, either online or through cheque. SBI calculates interest on daily basis in Maxgain. The interest is charged on the Book Balance, which is equal to your total principal outstanding minus the Available balance in the OD account. Hence, after withdrawal of the entire Available Balance, you will be charged interest on the Total principal outstanding.

Yes, there are no charges for withdrawal of the parked amount. It is your money and you can withdraw it anytime you want without incurring any charges.

Regards

Anuj

Hi Anuj,

I have transfer my Homeloan + Topup loan to SBI in Nov 2015. I have asked for SBI Maxgain account but bank provide me Term loan account. My total loan is 12,00,000+4,00,000. Is it possible to change account to maxgain and if yes what is the procedure.

Hi Abhijeet

Some months back, SBI has put a minimum Rs. 20 lakh loan amount condition for Maxgain product. That is why you could not get the Maxgain Home Loan. It will not be possible to change to Maxgain for this loan amount.

Regards

Anuj

Thanks Anuj.

Does online SBI OD Maxgain account shows the abount debit towards principle like it shows Interest Debit txn? how to know how much amount was adjusted towards principle.

Just check your available balance at one day before end of month. On 1st date the available balance is reduced. Subtract the interest debited from the reduced balance. Thats it you get the principle deducted

Manoj

The best way is to get the Maxgain loan amortization schedule from your branch. This will give you the exact principal components in your monthly EMI from start will end of tenure.

Regards

Anuj

Team,

I hold SBI maxgain with amount 26,60,000 for 15 years. Approved in Mar ’16 EMI starting APR’16.As Loan was sanctioned in March last week I see debit int for 1 week extra aprt from April Debit int.

Now only 1 EMI has completed,i see below pic.Not getting difference between Book balance and drawing Power. Also just to test the feature I deposited 500 Rs in OD maxgain account and expecting available bal as 500 Rs but its still 0 though txn present on OD as credit . Getting confused ,pls help.

Book Balance -26,55,117.00

Available Balance 0.00

Limit 26,39,103.00

Uncleared balance 0.00

Drawing Power 26,39,103.00

Pls help for above Query

Hi Manoj

I had replied to your query about 2 weeks back but somehow it did not get posted.

It seems that the amount of interest debited from your OD account in Mar was less than the chargeable amount. You should immediately park about Rs. 18K in the OD account. Some of it would be debited towards March interest, depending on the date of disbursement and interest rate. Most likely this amount will be debited on last day of May if you deposit now.

It would be better for you to maintain a SBI Maxgain Home loan calculator to be able to predict exactly how much interest you will be paying and saving every month.

Regards

Anuj

Hi,

Can you please provide the max gain calculator? Also, if you have any traditional calculator with pre-payment option, please send to my mail address.

Thanks,

Susanta

Susanta

Please send me a mail on [email protected] for the Maxgain calculator.

Regards

Anuj