Team Jagoinvestor

Team Jagoinvestor

September 6, 2019

September 6, 2019

Apollo Munich Optima Restore Policy – Detailed Review + 13 Benefits

In this article, we will see various features of Apollo Munich Optima Restore Health Cover policy. We will be covering its benefits, exclusions, eligibility and premiums details.

Apollo Munich is one of the most respected and well known health insurance company in India, which offers different health insurance plans for family, individual and senior citizens. Optima restore is its flagship health insurance plan, which has recently got some more features and we will discuss that in detail.

Let’s start.

Benefits of Apollo Munich Optima Restore policy

Below are the benefits you will get as a policy holder.

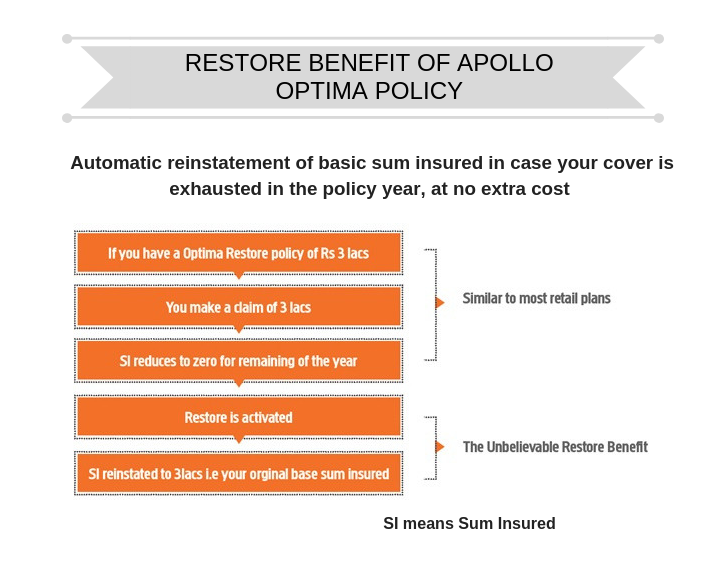

Benefit #1 – Restore Benefit

In Apollo Munich Optima Restore policy there is restoration benefit, which means that when you file for a claim in any year and the sum insured (plus the bonus, if any) is totally exhausted, then it will automatically be refilled to the extent of your basic sum insured. So in a way you get the full sum assured benefit again in the same year.

Let’s take an example – Suppose you are having health insurance of Rs. 5 Lakhs per year so, restoration benefit will work as follows –

[su_table responsive=”yes” alternate=”no”]

| Cover Amount | Claims made | Restoration Benefit |

| 5,00,000 | Claimed Rs. 3 Lakhs after 5 months of policy in force | Zero – as balance health cover is still there |

| Balance Left 2,00,000 | Claimed Rs. 1.5 Lakhs in next 2 months after first claim (7 months over) | Zero – as balance health cover is still there |

| Balance Left 50,000 | Claimed balance Rs. 50,000 in next 1 month after second claim (8 months over) | As the whole sum assured is exhausted, the restoration benefit will trigger now and the sum assured now will again be Rs. 5,00,000 – for next 4 months |

[/su_table]

So, as per the example, you can again claim up to Rs. 5,00,000 in remaining 4 months of your policy without paying any premium or any charges. If restored sum insured is not utilized in a policy year, it will expire. Note, that the restore benefit is available once in a year and it will be available to all Insured Persons for all claims under In-patient Benefit during the current Policy year.

**Restoration benefit is different from recharge benefit offered by different health insurance policies. Recharge benefit says that, your sum insured will be refilled to the amount of basic sum insured, every time when your sum insured amount is utilized for any claim, it does not matter what amount has been reduced from the total amount of sum insured cover.

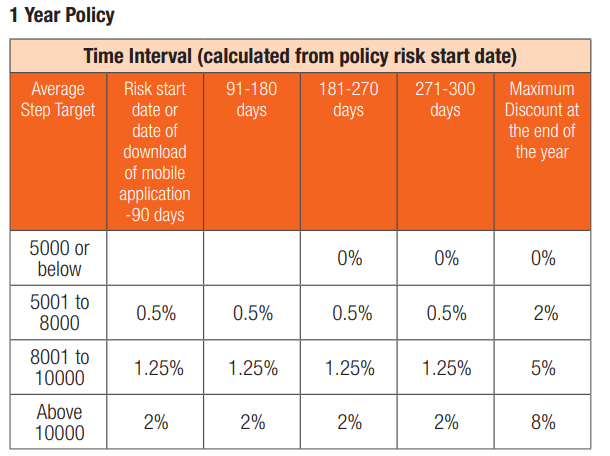

Benefit #2 – ‘Stay Active’ – Get discount for staying healthy

In order to encourage policyholders to stay healthy, this policy provides stay active benefit which says that, if you walk certain number of steps on daily basis, you will get discount at the time of renewal. Your activity will be tracked on a mobile application provided by them (Health Jinn app). The discount can vary from 2%, 5% or 8% depending on average steps you made during the year.

They have defined the time intervals of 90 days starting from the date of policy to average out total walking steps taken during this period. The year is broken down into 4 parts as follows – 90 days, 91 – 180 days, 181 – 270 days and 271 – 300 days. You can refer following table to understand how this benefit will work –

In year 2 of policy, calculation will be bit complicated but, the point is, if in a year you can manage to have average walking steps of 10,000 and above, you will be able to avail 8% discount on renewal premium, provided that, the mobile app must be downloaded within 30 days of the policy risk start date to avail this benefit.

In an individual policy, the average step count would be calculated per adult member and in a floater policy it would be an average of all adult members covered whereas, dependent children covered either in individual or floater plan will not be considered for calculation of average steps. So, dependent child is not eligible for this benefit.

For this you simply need to download an app called Health Jinn app on your phone, sync it with Google Fit or Apple Health and aim to walk 10,000+ steps every day to earn the complete 8% discount. Walking is one of the most beneficial things one can do for health and fitness. So, you will enjoy discount on premium amount as well as be motivated to exercise regularly.

However, we are not sure how many policy holders will have this level of discipline to track their walking steps and buy all the equipment’s, so in a way it’s a benefit only tech savvy policyholders will be able to enjoy who can also be disciplined for the whole year at the same time.

Benefit #3 – E-opinion (Second Opinion for critical illnesses)

In Apollo Munich optima restore health insurance, if insured is diagnosed with any critical illness (listed in policy) then he will be able to take second opinion from a medical practitioner appointed under penal of medical practitioners. Following illnesses are covered under critical illness –

- Cancer of Specified Severity

- Open Chest CABG

- Myocardial Infarction (First Heart Attack of specific severity)

- Kidney Failure requiring regular dialysis

- Major Organ/Bone Marrow Transplant

- Multiple Sclerosis with Persisting Symptoms

- Permanent Paralysis of Limbs and Stroke resulting in permanent symptoms

However, this benefit is available only once in a policy year.

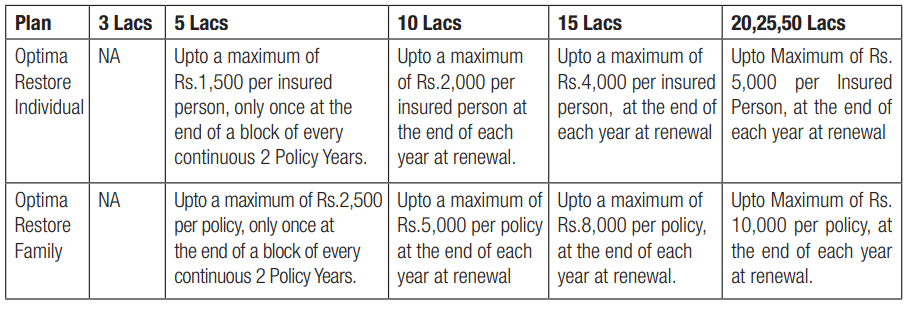

Benefit #4 – Preventive Health checkup

We all know that health is wealth but, even after knowing this, we tend to neglect regular health check-ups. In this policy, the health checks costs are included, which in a way gives the policyholder a great push to do their health checkups.

So, in this plan, the policyholder will get the cash reimbursement for taking preventive health checkups.

In Optima restore, for a sum assured of Rs. 5 Lac they provide cash reimbursement at the end of a block of every continuous 2 Policy Years and once a year on the sum assured of Rs.10 Lac or more.

You can refer following to know what amount of cash will be reimbursed –

**Preventive Health Check-up means a package of medical test(s) undertaken for general assessment of health status, it does not include any diagnostic or investigative medical tests for evaluation of illness or a disease.

Note that these checkups are great for people because if you keep doing these checkups, then you will be able to detect any illness or major issue before it becomes critical.

Benefit #5 – Daily cash Benefit

Daily cash is the cash benefit, which you get by the insurance company on a day to day (in case of hospitalization above 24 hrs.) basis, if you have been hospitalized in a shared accommodation in network hospitals of insurance company for more than 48 hours.

This cash benefit is already decided amount irrespective of your actual daily expenses. In this policy, you will get Rs.800 per day as daily cash which has a limit of up to Rs.4, 800.

For example: If “A” and “B” both get admitted to a hospital (both of them are covered under this policy). Suppose A’s daily expenses are Rs.600 per day and B’s expenses are Rs.1000 per day, in this case, though the expenses are different, both of them will get Rs.800 as a daily cash because it is decided previously in their policy.

So here A will save Rs.200 and B has to pay Rs.200 extra from his own pocket per day.

In another case, a person “C” is hospitalized and his daily expenses are Rs.800, but he has to stay there for 7 days. Here the total daily expenses of the person will be Rs.5600 (for 7 days)but as it is mentioned in his policy clearly, he will get only Rs.4800 as daily cash and the rest he has to pay by his own.

However, daily cash benefit is not given for an insured admitted in Intensive care unit. And the limit is higher for higher sum insured i.e. it is Rs. 1000 per day up to Rs. 6000 for sum insured of Rs. 20 Lakhs, 25 Lakhs and 30 Lakhs.

You can watch this video given below to know the plan details of Apollo Munich Optima Restore policy:

Benefit #6 – Multiplier Benefit

There is something called as Multiplier benefit under this policy which gives additional sum assured to policy holder when there is no claim in any given policy year. It is like a bonus included in sum insured amount in case of no claim made during a year.

One can get a bonus of 50% of the basic sum insured for every claim free year, accumulating up to 100%. In the event of a claim, the bonus shall be reduced by 50% of the basic sum insured at the time of renewal. It simply means insurance company will take back benefit of bonus on making any amount of claim.

Example : Suppose you had a policy cover of Rs. 10 Lakhs for a year, but you didn’t claim anything in that year. So, policy sum insured will be increased to Rs. 15 Lakhs (10 Lakh + 50% of 10 lacs). And next year again, if there is no claim then it will be increased to Rs. 20 Lakhs.

But, once you claim any amount against your insurance, then renewal amount of sum insured will be reduced by 5 Lakhs (50% of 10 Lakhs) and it will Rs. 15 Lakhs.

It’s a great thing, because this way you are actually getting upto 20 lacs of health insurance even if you have taken just 10 lacs at the time of buying the policy.

Benefit #8 – Cashless Service

Like most of the policies, there is cashless service in this policy too, which means that the insurance company will make payment directly to the hospital provided it’s within its network and there was prior approval taken for the hospitalization at least 48 hours before.

In case of unplanned or emergency hospitalizations, one can still do all the expense from their end and claim for reimbursement later.

Benefit #9 – Pre and Post hospitalization

Apollo Munich Optima Restore policy covers pre hospitalization expenses up to 60 days immediately before hospitalization and post hospitalization expense of 180 days immediately after hospitalization.

Whenever a person is hospitalized, before that he might have gone through various tests/consultations and even after getting discharge from hospital, he will have to pay bills of medicine and other tests.

Benefit #10 – Organ donor Expenses

When insured is having an organ transplant surgery then all the expense related to that will be paid by insurance company. But it will exclude pre and post hospitalization expense of donor. Provided the undergoing of a transplant must be confirmed by specialist. However, any other expenses incurred by an insured person while donating an organ is NOT covered.

Benefit #11 – Domiciliary Expenses

Apollo Munich Optima Health Restore policy also provides for domiciliary expenses which means medical treatment for an illness/disease/injury which in the normal course would require care and treatment at a hospital but is actually taken while confined at home under any of the following circumstances:

- The condition of the patient is such that he/she is not in a condition to be removed to a hospital, or

- The patient takes treatment at home on account of non-availability of room in a hospital.

Benefit #12 – Portability

If you are insured with some other company’s health insurance and want to shift to this policy on renewal, then without starting a new cycle of waiting period, you can shift to this policy. Apollo’s portability policy is customer friendly and aims to achieve the transfer of most of the accrued benefits and makes due allowances for waiting periods etc.

Benefit #13 – Day Care Procedures

This health insurance also provides for Day Care Procedures i.e. Medical treatment or surgical procedure (eg. cataract), which require admission in a Hospital/Day Care Center for stay less than 24 hours. Treatment normally taken on out-patient basis is not included in the scope of this definition.

Indicative list of Day Care Procedures that are covered in this benefit is as follows-

• Cancer Chemotherapy

• Liver biopsy

• Coronary angiography

• Haemodialysis

• Operation of cataract

• Nasal sinus aspiration

Other Rules of the Policy

- Maximum Age – The maximum entry age is 65 years, however, there is no maximum cover ceasing age in this policy.

- Minimum Age – The minimum entry age is 91 days i.e. children between 91 days and 5 years can be insured provided either parent is getting insured in this policy.

- The validity of the policy and Discount – The policy will be valid for a period of 1 to 2 year(s) as opted. If a 2-year policy is chosen then an additional 7.5% discount is offered on the premium

- Eligibility for buying the policy – An individual or his family members such as spouse, children, parents/parents-in-law are eligible for buying this cover on an individual or floater basis.

Exclusions – What is not covered in this policy?

- Any treatment within the first 30 days of cover except any accidental injury.

- Any Pre-existing diseases/conditions will be covered after a waiting period of 3 years.

- 2 years exclusion for specific diseases like cataract, hernia, hysterectomy, joint replacement etc.

- Expenses arising from HIV or AIDS and related diseases.

- Abuse of intoxicant or a hallucinogenic substance like drugs and alcohol.

- Pregnancy, dental treatment, external aids, and appliances.

- Hospitalization due to war or an act of war or due to the nuclear, chemical or biological weapon and radiation of any kind.

- Non-allopathic treatment, congenital external diseases, mental disorder, cosmetic surgery or

weight control treatments.

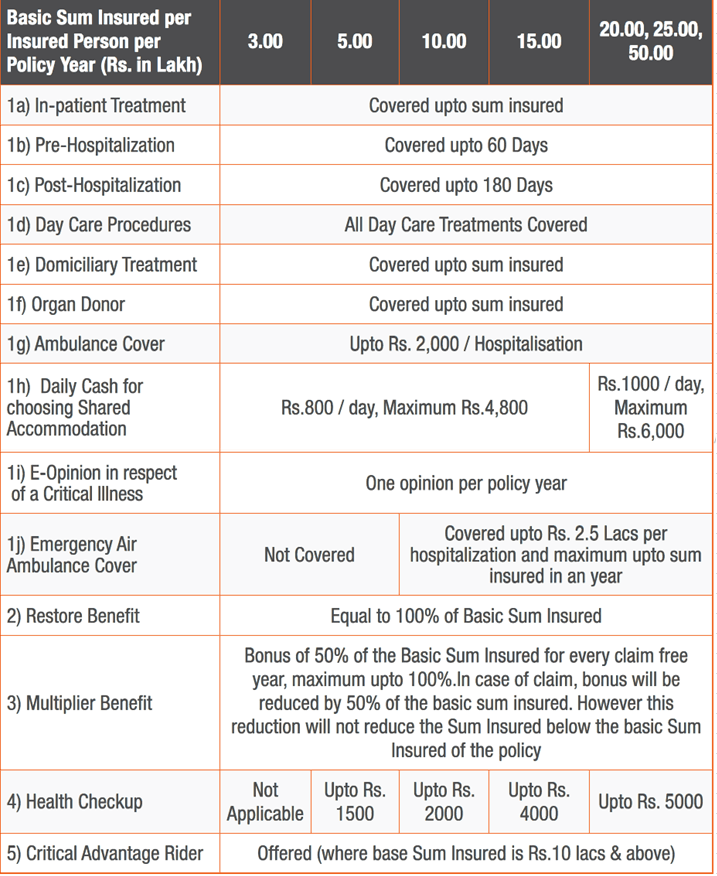

Details of individual policy –

If you are buying health insurance for yourself then following table will be helpful to understand what all benefits you will be having for different amount of sum insured.

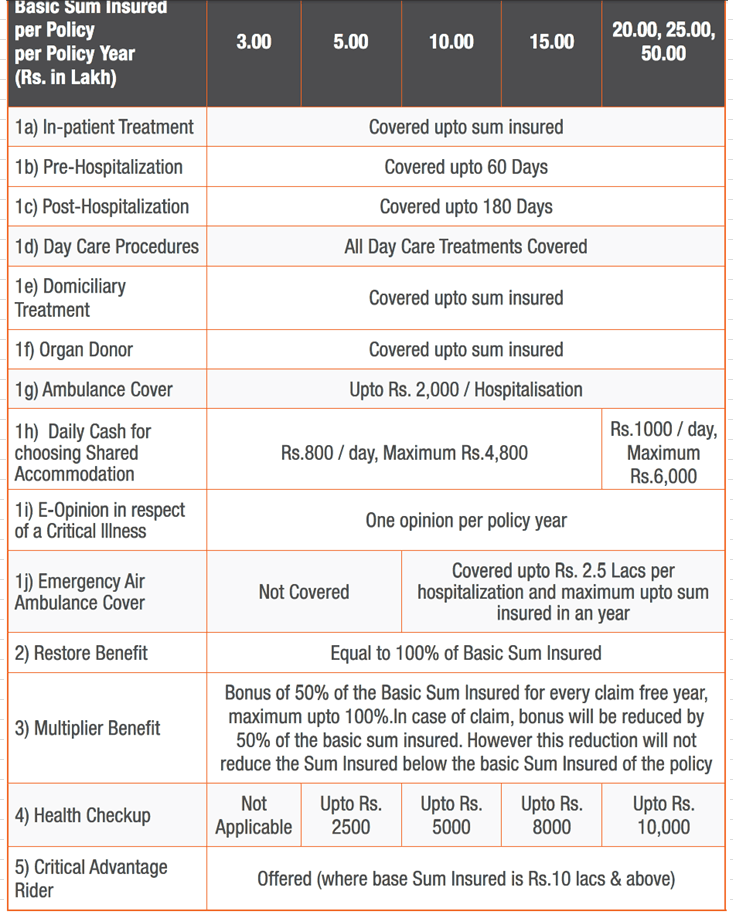

Details of a family floater –

If you are buying health insurance for you and your family then following table will be helpful to understand what all benefits you will be having for different amount of sum insured.

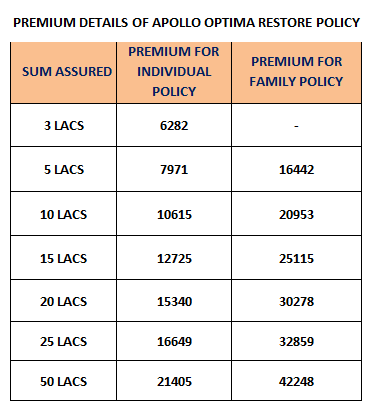

Premium details of individual and family policy:

You can refer below given table to get an idea of the premium amount of this policy. The table shows followings –

- Premium details of a man aged 30 years for an individual policy.

- Premium details of a family policy, comprising of an individual (aged 30 yrs.), his wife (aged 30 yrs.), son (aged 8 yrs.) and daughter (aged 10 yrs.). The family policy starts from 5 lakhs of sum assured.

**This is the premium details of 1-year policy including GST and excluding the critical illness cover cost.

Conclusion

We feel that overall this policy has all the standard features, however there are many other policies which can also be looked at before making the decision.

If you have any doubts regarding this policy cover, you can leave your query in the comment section.

Sir,

I’m 43 and want to take family floater policy for me, wife and child. I’m also have a pre-existing disease.

I would like your suggestion on whether I should take family floater or take one separate policy for me and floater for wife and child.

Are there any drawbacks if taken family floater with pre-existing condition?

I dont think there is a big issue as the premium will anyways be calculated depending on who all have pre-existing illnesses.

To keep it simple, you can go with a family floater!

Manish

Sir,

So there will be increased premium because of 1 member pre existing disease.

Won’t it be beneficial (premium wise) to separate policy for wife+child ?

It will only rise keeping in mind 1 person. Not everyone will have to pay price for that!

Does Apollo Munich Optima Restore has NO ROOM RENT LIMIT & NO COPAY Clause ..I gone through policy document but could not find specific mention of these though online portals are saying that it has No Room Rent limit and No Copay..wanted to verify

I have health policy Appolo Munich Optima restore. Is this ok or we should port to some where else. This is family flotter 5lac for three member. Tell me

Why to port?

Hi,

Nice Informative article. Just wanted to check on these health plans. Suppose I buy health insurance plan for 5 lacs – will it cover critical illness hospitalization costs to the tune of 5 lac or are critical illness excluded from the Health Insurance plans ?

I know critical illness plans would provide lump sum benefits but if person has not taken that, will health insurance take care of costs upto the maximum benefit amount as per the health care insurance policy ?

Hi Rajesh,

Health insurance policies provide for regular hospitalizations, it does not cover for critical illnesses.

Critical illnesses are excluded from all health insurance policies. However, you can add a rider to get critical illness cover.

Thanks,

Vandana

I am 42 year old with 2 daughters. Planning to buy some policy for old age when i shall be 55 or 60 with no company cover. It will be for me and my 2 daughters. So would you advice to buy policy right now or shall buy 5 years before i retire. I mean total cost of policy vs benefits

Hi Vineet,

We suggest you to buy the health insurance policy now. Because, you attract any serious illness before retirement then it will be very tough for you to get insurance on your own later. And even if you get one, the premium will be high.

So, don’t delay and buy health insurance. If you need any support in this area, you can reach us at help@jagoinvestor.com

Thank you,

Vandana

Hi,

Now aditya birla 1Cr plan is looking more suitable as premium is almost same but SI is more, can you please provide review for it.

Hi manish

You are talking about its term plan. I will try to provide review on it.

Thank you,

Vandana

Sir once we purchase a policy, all we get is Policy Wordings/Policy Schedule (80D), E-cards

But where will we get ‘My policy’ i.e how will i know that the policy issued to me does indeed have all the things that i selected, example “no room rent”

Hi suhas,

When you buy a policy, you get a policy document in PDF form via mail or in physical form via post. In this document all the details of your policy are written, like benefits, limitations, bonus payable, term etc.

If you haven’t got this from your insurance company so, request them to issue the same.

Thank you,

Vandana

I think the restore benefit also comes in even in the case of partial claim during the year, but this is not mentioned in the above article?

Hi NITIN

Thanks for your comment.

I have revised the wordings of restoration benefit.

Vandana

How are Max Bupa policies compare to Apollo Munich?

Hi Navneet, which policy you want to compare against which ?

ITs not company to company , but policy to policy comparision

Manish

I think Restore benefit is available for same illness as well, as company has mentioned that Restore benefit can be used for any claim arising in a year. so it means it can be used for same illness as well. They have not clearly mentioned anywhere that it can be used for other illness only.

Hi vaishali

Yes, you are right. I have removed that point from the article, it was wrongly written.

Thank you,

Vandana

Do they provide Super Top Up as well?

Hi JK

Yes, you can get super top up policy as well for getting additional cover over, on and above your existing sum assured.

Thank you,

Vandana

I am having oriental family floater for me and my wife SA 6 lac from last 4 years. Should I port to optima restor

Hi Rajesh Kumar

You need to compare both the policies, on the basis of benefits and their premium they charge for required sum assured.

However, I will suggest you to increase the sum assured of your family floater health insurance.

Thank you,

Vandana

Please also give review of ICICI Pru cancer and heart care insurance policy

Hi Anurag Vyas

Thanks for your comment. Soon, We will write on the said policy also.

Vandana

Hi,

Thanks for the detailed info. HDFC Ergo plans to acquire Apollo Munich, what repercussions this can have for existing & new policy holders?

Thanks,

Sonal

Hi Sonal,

I don’t think this is going to affect existing policy holders as, Regulations of insurance regulatory and development authority (IRDA) protect the interests of existing customers at every stage.

This merger can affect some benefits, terms or condition but that will be applicable for all new products launched by aplollo munich.

However, at the time of renewal, some policy terms or premium may change for existing policies, but merger will not be the reason for that. It is going to happen in each and every policy due to decision making on the basis of product review and economical changes like inflation.

Thank you,

Vandana

But what about new policy buyers? They will still be bound by the policy wordings issued at the time of policy issual right? And will the wordings remain same for every renewal?

Hi srinivasan,

In most of the cases, existing policies feature, benefits and policy wordings are kept as it is, even on renewal.

Due to mergers or acquisitions Changes will be in new policy formation and pricing models.

Thanks

Vandana

1. Overall cashless hospitals are less as compared to other big players like HDFC Ergo and ICICI Lombard, Bajaj

2 No Ayush benefits (Ayurvedic, Yunani, Homeopathy) only allopathy

3. Biggest threat – Cashless

prior approval have to take for the hospitalization at least 48 hours before.

Hi Sunil Sharma

You are rights, these are some of the drawbacks of this policy.

Our intention of writing this article was to simplify policy wordings for policy holders. It is not to encourage anyone to buy this policy.

Vandana