We will today discuss some of the best practices and must do things while taking a Term plan.

Click here to read what is Term Insurance and its Importance

1. Take a policy just before your Birthday.

Term Insurance premium depends on your Age. So if possible try to avoid taking the policy just after your Birth date. What i mean by this is that try taking it before you turn +1 year in age. If your Date of birth is 10/11/1983, and you take the policy on or before 10/11/2008, you will be considered of age 24.

But if you do a delay of 2 days … and you take a policy on 12/11/2008. You will be considered 25 yrs old and hence your premium will increase by 4-5%.

Note : It does not mean that if your birthday just passed by and now you want to take Insurance, then you should wait for another year. that’s not what i am saying 🙂

For example:

For a male with DOB on 10/11/1983 (24 yrs old), the premium for Rs 50,00,000 cover with tenure of 25 yrs, is 10157, if the policy is taken on 09/11/2008 (just 1 day before the birthday). Where as if he takes the policy on 12/11/2008, the premium will shoot up to 10647 (Rs 490 more) .. though 490 is a small amount, but if we can avoid it by taking the policy little early .. always try to do it.

Even a small amount like 490 saved over 25 yrs in a PPF would give 45,000 and in mutual fund with 12% return will give 77,000.

Note : The gist of the point is that try to see this small point while taking the Term insurance, it does not mean that you wait for 8-9 months just to take the policy before a birthday.

2. Try to diversify your Policy

If possible try to diversify your policy amount over different Insurance companies. If you want to take an Insurance of 50,00,000, it would be better if you take 2 polices, rather than 1 single policy.

How it helps?

– If you hold a single policy and the company does not honour the claim, dependents wont get anything, but if there are 2 parts, then there are less chances that both the companies with not honour the policy.

– If your liabilities come down or you have less dependents after a couple of years and ultimately you need to bring down your Life insurance cover, you can simply stop one of the policies and continue the other one.

– It helps in diversifying the risks involved with the Insurance company.

3. Buy a policy early in life and for longer Tenure.

Its always recommended to buy a Term Insurance early in life and for maximum tenure possible. In your early life you are more healthy and hence your premium will be lowest. Also by taking insurance for a large tenure you are making sure that you are covered for a large period, but the premium will be marginally more.

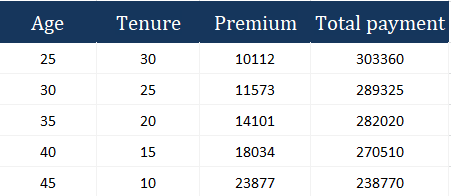

For example : For a cover of 50,00,000

You can see here that you have to pay marginally more for an extra cover of 5 yrs. So for example, a person with age 25 will pay 14,000 more than the 30 yrs old, but he will be insured for 5 additional years. So it always pays in long term.

Also taking a 30 years term insurance once will be very cost efficient than taking a 20 yrs term insurance now and then taking a term insurance of 10 additional years after 20 yrs. Because after 20 yrs, the premium you will pay for that 10 yrs tenure term insurance will depend on your Age that time and health that time.

Note : Premiums are from Aegon Religare Life Insurance.