Jagoinvestor

Jagoinvestor

February 24, 2014

February 24, 2014

5 must know rules before Opening PPF Account for minor child

PPF account is one of the most favorite investment product in India and every person wants to open a PPF account for minor child. However, there are lots of myths about the rules on opening PPF account for minor kids.

In this article, we will look at some of the important points you should know if you want to open a PPF account for your children. We will discuss about tax exemption, limit on the amount you can invest and PPF maturity rules. Here they are

UPDATE: The limit was 1 Lac when this article was written. Now it has increased to 1.5 Lacs.

1. Who can open PPF account for minor Child ?

As per PPF rules, a guardian can open Public Provident Fund account for minor child, where guardian is

- Either Father or Mother

- Or incase of Parents are not alive, then any other guardian under the law can open PPF account for minor children, like Uncle, Aunt, Grandmother, Grandfather etc.

- Incase a surviving parent is incapable of acting, then also some other guardian (as mentioned above) can open PPF minor account

2. How much can I invest in PPF account of Minor Child ?

There is a very big confusion around this topic. The most common question is – “Can I invest more than 1 lac in PPF account ?”

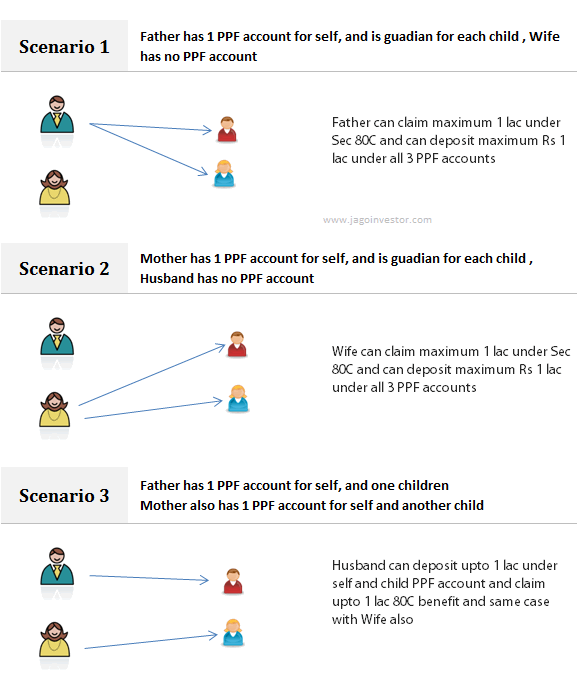

As per my understanding and all the readings I did on this topic, I came to know that One can invest maximum of Rs 1 lac in all the combined PPF (Public Provident Fund) account a person has which is self , and for minor children. Example – Imagine there is a Father (F) and Mother (M) and there are two minor children – C1 and C2 . Now follow scenario’s are possible

- Father (F) can open PPF account for himself, C1, and C2

- Wife (W) can open PPF account for herself, C1 and C2

- Father can open PPF account for himself and C1 (or C2) , Wife can open PPF account for herself and C2 (or C1)

Here are these 3 scenarios possible

3. Can I deposit more than 1 lac in PPF account even if I don’t need income tax exemption ?

This is one question which really needs clarity, because a lot of people open PPF accounts for minor children and invest Rs 1 lac in all the Public Provident Fund accounts (Here are articles on opening PPF account with ICICI Bank and with SBI Bank).

You don’t get income tax exemption under 80C for more than total Rs 1 lac, which is fine for many people, but are you eligible to get benefits on more than 1 lac invested or not ?

As per PPF rules, you are just not allowed to invest more than Rs 1 lac in your own PPF account or any other PPF account where you are guardian. So if you have 2 kids and you have opened PPF account in their names, you might be thinking that you can invest 1 lac in your own PPF and 1 lac in each kid PPF account so that you can enjoy tax free maturity income later for your kids PPF account .

But I dont think its allowed, because as per PPF rules, the 1 lac limit is for an individual , not on per account basis .

But I have been investing more than 1 lac each year, already from many years !

I know, a lot of investors who have been investing more than 1 lac in PPF each year. Due to technological challenges, it might be possible that no one stopped you from doing it, but in future if govt comes to know that you have been avoiding the rules, you might not get any interest on the excess amount, so you might get back only the principal amount at the time of maturity.

A lot of Bank staff are also not clear on these rules , here is an incident which was shared by one of our readers

Today I met manager of the branch of bank (State Bank of India) where I have all these three accounts. I narrated the whole scenario. He does not see any problem with the situation.

I am really confused as to continue this mode of financial plan or to change it in the light of your clarification regarding the total ppf investment limit.

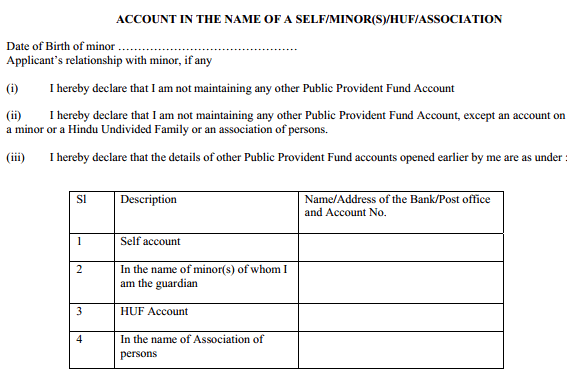

4. Do I need to declare about my personal PPF accounts at the time of opening minor PPF ?

A person can not have more than 1 PPF account on self name, but they can have it as a guardian for his children , but you need to declare about all your PPF (Public Provident Fund) account as self and for other children at the time of opening a new PPF account with other kids.

Because when you fill up the PPF opening form, there is a declaration you need to give about it , here is a snapshot of how it looks like

Which means that legally you need to declare about your other PPF accounts , if you don’t do so, you are breaking the law and if in future its detected that you have been doing what is not allowed, all the money you have deposited in PPF account in excess to the limit allowed will just be returned to you without any interest, and that might be a big blow to your overall planning.

So, a small change you can do in your overall planning is that, you can ask your spouse to open PPF account as guardian for the child, this way, one husband can avail upto 1 lac benefit and wife can also avail upto 1 lac benefit.

5. What happens when the minor kid becomes a major ?

Case 1 : If PPF account matures before the child attains 18 yrs –

In this case the guardian can either withdraw the money from PPF or extend it for another 5 yrs block . In this case, the money withdrawn will be treated as guardian income and now when this money is invested somewhere else and any interest income is earned (learn how PPF interest is calculated), then it will be treated as guardian income only.

So imagine PPF (Public Provident Fund) account is matured and the kid is still minor (assume you opened the PPF when he/she was 1 yr old) and you get Rs 10 lacs from PPF account, now when you invest this 10 lacs into FD , you get Rs 1 lac as interest in a year, this interest income will be treated as your income (guardian income) and will be added into income and taxed accordingly.

Case 2 : If PPF account matures after the child attains 18 yrs (become’s major) –

In this case, the account will then be operated by the child (who has become major) and there will be no guardian. The child will then take his/her own independent decision.

In this case, because the PPF account has matured after the child has attained maturity age, all the maturity amount will be income of the child itself, Now any interest income earned on this amount in future will be kid income.

Conclusion

PPF account for minor children is a good idea if you want to build a long term corpus for their education or other requirement. However if you are already exhausting your own limit for PPF (Public Provident Fund), then it might not be that useful because their a limit on the investment amount.

You need to see how you want to divide the amount between your own and your kid and whom do you want to make guardian, yourself or your spouse ?

Can you share about your case ? Do you have PPF account for your minor child ?

Dear Sir,

I have received a lump sum amount towards full n final settlement of divorce so i want to open two ppf account one for self and other for my minor child can i do it ? if so pls exlplain in detail..THANKS IN ADVANCE.

Yes, you can do it, but you cant deposit the whole amount in one go . Why are you not investing in something better?

I have a daughter. We are all NRI’s. Can i open a PPF account for her?

I dont think you can as of now

if i open ppf account in the name of child, once child becomes major. can he still maintain ppf account in blocks of 5 yrs? if yes, for how many times it can be extended?

YES, they can

Can I open PPF account for 7 month old baby?

What will be the maturity period of this account ?

Yes you can.

It will still be 15 yrs from the date of opening

My friend and his wife both are Indian citizens. Their minor child was born in USA . This child is holding a US passport. . This child is now living with the parents in India . The child is having Persons of Indian Origin Card .Can the parents open a PPF account for this child.

I think they can if the child is also an INDIAN CITIZEN

Dear Sir,

I had opened PPF account of my minor daughter name in 2013. Now i want to change her name from old to new in the bank Passbook. I have revised birth certificate also with the new name. So how can it’s possible to update the name in my PPF account ? Please reply.

Thanks.

Hi Paras

Its simple you just visit the bank and ask them . Usually they will ask you to just submit a name change form with the Proof of Name in the Bank.

sir I have 2 years old son I want open ppf A/C pl guide me

Sir

My PPF account Completed 20 Year..

1. Can I Also extend..

2. Or Can I Open MY Grand son account..

Yes you can do both

Thanks for the article.

As per the point 5 can I conclude that it’s good to open PPF account on child’s name only when she/he attains 3+ years of age. So, that the matured amount can be invested in child’s name and tax can be avoided ( considering child will not earn at the age of 18 years) .

If yes, I am little confused whether it’s 2+ year or 3+year. Please correct me.

Anyways PPF maturity amount is not taxable !

Hi Manish

I have few questions about PPF account

1) If I have a PPF account which is about to mature soon and I want to take all of that money. But at the same time I want to extend that account for block of 5years. Is that possible?

2) What happens to PPF account if I take all the money after maturity? Is the account closed ?

3) If PPF account is closed after maturity and after few months again I want to open PPF account. Should I open new account or can I continue with old account ?

1. No, you can only partially withdraw money

2. Yes

3. Once you close the PPF account, you cant reopen the same account. IN that case again a new PPF account will be active !

Thanks Manish, If I don’t want to close PPF account after maturity, how much minimum amount do we need to keep in account to avoid closure. What is the maximum amount we can withdraw ?

If you extend the PPF account, then you can only withdraw 60% of the amount

Hai,

My husband is having ppf account n he invest 10k yearly once, and now he want to open ppf for our kid 2.8 yrs old. Now my question is if he want to increase the investing amt, is that possible in the existing account. And. He wants to start ppf for kid on monthly basis, what is the minimum amt?

There is no fix amount in PPF , you can invest anything from Rs 500 to Rs 1.5 lacs each year .. no fixed amounts each year !

Me, my non-working wife and minor child – all 3 have PPF accounts. Child account is opened under guardianship of my wife. I want to know how can I invest more than 1.5 lakh in all 3 PPF. Read some below situations and confirm which are valid:

(1) I invest 1.5L in my own PPF account and 1.5L in minor child PPF account (wife is guardian of chils ppf). I also gift 1.5L to my non-working wife (will keep gift deed) and she deposit that 1.5L in her own PPF account. Is this valid situation and can I go ahead with this? I will not claim more than 1.5L tax rebate.

(2) In point 1 above, instead of gift to wife in Saving account, can I deposit 1.5L cheque in my wife PPF and also keep a gift deed saving 1.5L gifted to wife who is depositing that amount in her own PPF account?

(3) If above is not true, can I gift 1.5L to my mother (my mother is senior citizen and non-working) and then she gift 1.5L to my minor child (means to her grand-child) by depositing 1.5L cheque in my child PPF (and will also keep a gift deed). Is this valid?

My only intention is to put more than 1.5L in PPF (as I trust PPF as the best inveestment option). Please suggest

You cant put more than 1.5 lacs legally .

But many places it is mentioned that I can give gift to my wife. Is this not correct?

Also it is mentioned that I can deposit 1.5L in my account and same in my minor kid whose ppf guardian is my non-working wife. Is this also wrong?

Can you also clarify if I can gift to my sr citizen nonworking mother, who can deposit 1.5L in my kif ppf?

Hi Manish, Please provide your expert advise here:

At many places it is mentioned that I can give gift to my wife. Is this not correct?

Also it is mentioned that I can deposit 1.5L in my account and same amount in my minor kid whose ppf guardian is my non-working wife. Is this also wrong?

Can you also clarify if I can gift to my sr citizen non-working mother, who can deposit 1.5L in my kid ppf?

Check out this info – http://jagoinvestor.dev.diginnovators.site/2015/02/gift-tax-rules-in-india.html

I had opened a ppf account on my daughters name mahima in 1999 , later her name was changed in school to sonika. At the time of maturity after 15 years , i extended it for five years without realising that my daughter will no longer be minor at the time of extended maturity , as her name is chNged , she won’t be able to operate on ppf account name.whats the solution there is stll one tear to go fir her to become Adult.

You need to show the name change proof !

Hi,

I am working professional. Due to many investments I have no need to invest in PPF to reach 80C limit of 1.5 lac. Therefore I deposit only Rs. 500/- to keep the account active.

My mother has received some income by way of share trading and would have to pay tax if not invested.

Can she deposit money in my PPF account and get the benefit of 80C?

No , she cant get benefit by investing in your PPF

Hi,

If parent opens a account in the name of minor and maintaining in his books of account. Now minor becomes major also maintaining books.

Transfer is done at bank from guardian name to minor name after becoming major for all rights.

Now how can we transfer PPF balance as showing in guardian books to child books.

and what will be treatment in both books.

kindly specify.

Thanks,

Hi Maneesh,

I have a PPF account and I deposit Rs 1.5 lacs/ annum. Similarly my wife has a PPF account and she deposits Rs 1.5 lacs/ annum.

I also opened one account each for my two daughters in SBI and have been depositing Rs 1.5 lacs in each account.

I now understand that the PPF accounts I have opened for my daughters are not valid since one adult can have only one account, not even as a gaurdian. Consequently, I will not get any tax benefits at the time of withdrawal. Please advise how do I withdraw immediately. Does the bank give me an FD interest at-least ?

I think thats not true. One can open another PPF account as a guardian, but can only invest max 1.5 lacs in a year !

Refer your Article:

Scenario 2

In the second scenario, the mother has one self-PPF account and opens two other accounts to her two children respectively. Therefore, she manages three PPF accounts. At this stage, she can claim a maximum tax benefit of 1.5 lakh under Sec 80C of the Income Tax Act. Moreover, she will have to invest a maximum of one lakh in all the three accounts.

my Question is : Why she will have to invest maximum of one lakh in all three accounts when permissible investment is one Lakh fifty thousand per year.

Question No.2: I have two sons, 4 years and 2 years old respectively. Can my wife open PPF accounts in both’s name. I mean 2 separate minor accounts ? she doesn’t have any PPF account till date in her name.

Its a type. It has to be 1.5 lacs

Yes, you wife can do that !

Hi Manish,

I am working as well as my son is working. However both of us contribute towards the ppf ac of my son. While I dont go for 80c benefits but my son does claim 80c benefits under the ppf ac. Is it legal to do so?

Thanks

He can claim it for his share ..

Hi Manish,

My kids have PPF accounts. Now they are adults but nor resident in India anymore. How can these accounts be closed and money remitted?

Do they need to be present physically or will a POA suffice?

I think POA should suffice to redeem the money !

hi Manish,

I have 1 ppf account , i want to open ppf account for my kid. and my wife is not working, can she be the guardian for opening ppf account for the kid and deposit money in kids ppf account. Will there be any questions asked as she is not earning but investing in kids ppf? arun

No , there should not be any issue like that !