Recently all news dailies carried the headlines : ‘inflation rate has crossed double digits’. This indeed is worrying. So what is inflation and how does it affect the common man. In simple terms inflation is nothing but rise in the general level of prices of goods and services in an economy. What leads to this rise in the price of goods? It is ‘too much money chasing too few goods’ which leads to the rise in the prices of goods. It is a simple demand-supply mismatch. Because of inflation, our paper money or currency starts losing its value.

Some 15 years back when I saw my first movie in a movie hall it cost me Rs 15 to watch that movie. Now 15 years down the line, to watch the same movie in a multiplex, it costs me about Rs 225. So in 15 years the cost of watching a movie has multiplied 15 times. Now it might cost you Rs 15 just to park your car in the multiplex basement, forget about watching the movie in Rs 15. That’s inflation for you.

Explanation

Let’s take a simple example to understand this. Suppose you have a currency note of Rs 100. Assume that as on today with this currency note of Rs 100 you can buy 1 dozen apples (mind you this is just an example. In real life good quality apples are much more costly and I doubt if Rs 100 will even buy you half a dozen of good quality apples). But you don’t need these apples as on today and need them 1 year down the line. So you don’t buy the apples today as you can’t store them for one year as they will get spoilt. So you invest this Rs 100 for 1 year in a bank fixed deposit which will fetch you 8% at the end of 1 year. Now at the end of 1 year you have Rs 108. But let’s assume that inflation as compared to last year has risen by 10%. This effectively means cost of living or general prices of products have risen by 10%. So now the same 1 dozen apples which were costing you Rs 100 about one year back will now cost you Rs 110. Your money has grown by 8% (Rs 100 has become Rs 108) but the prices of apples have gone up by 10% (price increased from Rs 100 to Rs 110). So to buy the same 1 dozen of apples now (1 year down the line) you will have to put an additional Rs 2 from your pocket. This effectively means your currency or paper money has lost value. This is because of the effect of inflation. If the cost of living goes on increasing at this rapid rate every year, then 10 years down the line I doubt whether the same Rs 100 rupees will be able to buy even a single apple, forget about buying 1 dozen apples with Rs 100.

Had you bought the apples last year you would have managed to buy 1 dozen apples for Rs 100. But since you are buying them one year down the line and the return on investment (8%) that you have earned is less than increase in inflation (10%), you have to put more money from your pocket. So inflation erodes the value of your money over a period of time if the money is not invested wisely.

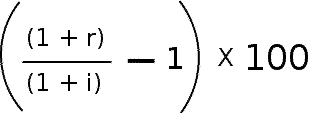

Nominal Returns and Real Returns

At the time of making investments you should make sure that, you earn a return which is higher than the inflation rate. Many people while measuring the returns on their investment forget to consider the effect of inflation. In the above example if we don’t consider the effect of inflation then our investment in the bank fixed deposit has earned 8% return. But this is not the correct way of measuring returns. This is just the nominal return. The return calculated after considering the effect of inflation is known as the real return. Real return can be calculated using the following formula

Here r is the rate of return (8%) and i is the inflation rate (10%)

1.08 / 1.10 is 0.9818

0.9818 – 1 is -0.01818

-0.01818 * 100 is -1.8181

So the effective or real return earned on this investment is -1.8181%

So even on the face of it, it seems that your investment has made a return of 8% (nominal return). After considering the inflation rate (10%), the real return is a negative 1.81. Which means actually on maturity you did not make any money, infact your money has lost value due to inflation. Surprised and hence the name of the article – ‘Inflation – The Silent Monster’ – inflation silently erodes the value of your money if you don’t invest wisely. So consider the effect of inflation while measuring your returns on maturity. Use following calculator to find your real investments real return .

Children Education Cost Inflation

Whenever the Weekly or Monthly Inflation Number is declared by the Government, the number represents average inflation which takes into account the rise in the average cost of living. This is a much broader number. If we break down this broad number into different components then we realise that different components have varied impact on individuals. All people are impacted by common things like food inflation and fuel inflation. People who have small children have to prepare themselves for Children Education Cost Inflation and Children Marriage Cost Inflation. So how do Children Education Cost Inflation and Children Marriage Cost affect and why do parents have to plan for this? Let us try to understand this with the help of a case study.

5 Easy Steps to do your Child’s Education Planning

Sample Case Study

- Let us take the example of Ajay. He wants to make his 1 year daughter, Priyanka a MBA when she grows up. Priyanka will take admission for the MBA course when she turns 21 years old. So Ajay has 20 years in hand to plan for Priyanka’s education.

- The MBA course as on today costs Rs 4,00,000. If we assume that education costs (inflation) will rise by 8% every year, then the same MBA course will cost a whopping Rs 18,64,382 after 20 years.

- To accumulate this Rs 18,64,382 in 20 years, Ajay will have to make a monthly investment of Rs 2046 per month if his investments earn a return of 12%. So even though the amount of Rs 18.64 Lakhs seems huge on its face, with regular investments, and the magic of compounding over a period of 20 years, this mammoth target can be achieved with investments of as low as Rs 2046 per month. But the secret to success is to start early and make regular and disciplined investments.

- If the returns earned by our investments are 15% then the investment amount further falls to Rs 1421 per month. Historically equities have given annual returns in the range of 15% over a long period of time.

- If the target of Rs 18.64 Lakhs has to be achieved without taking much risk through a Public Provident Fund (PPF) account which guarantees a return of 8%, then this target can be achieved with a monthly investment of Rs 3276 per month.

9 effective financial education tips for your Children

Importance of Starting Early

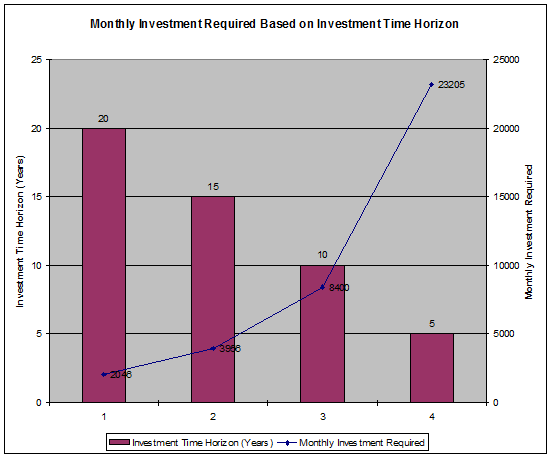

It is very important for the parent to start investing for the child’s future as early as possible. Starting early allows his money the much required time to grow and reap the benefits of compounding. Let us consider the above example of Ajay planning to accumulate money for Priyanka’s MBA course.

- His goal is to accumulate Rs 18,64,382 in 20 years. To accumulate this Rs 18,64,382 in 20 years, Ajay will have to make a monthly investment of Rs 2046 per month if his investments earn a return of 12%.

- If Ajay delays the investment plan and starts investment when the daughter is 6 years old, then in this case he will have 15 years to achieve his goal. In this case the monthly investments that he will have to make will rise to Rs 3956 per month to achieve his same target of Rs 18.64 Lakhs if his investments earn a return of 12%.

- If Ajay delays the investment plan and starts investment when the daughter is 11 years old, then in this case he will have 10 years to achieve his goal. In this case the monthly investments that he will have to make will rise to Rs 8400 per month to achieve his same target of Rs 18.64 Lakhs if his investments earn a return of 12%.

- If Ajay delays the investment plan and starts investment when the daughter is 16 years old, then in this case he will have 5 years to achieve his goal. In this case the monthly investments that he will have to make will rise to a whopping Rs 23205 per month to achieve his same target of Rs 18.64 Lakhs if his investments earn a return of 12%.

Use this Goal Planner Calculator to Plan your future goals .

The below table shows the monthly investment that will be required by Ajay to achieve his goal of Rs 18.64 Lakhs based on his investment time horizon. It is assumed that the investments will earn 12% in all the scenarios.

| Investment Time Horizon (Years) | Return (%) | Monthly Investment Required |

| 20 | 12 | Rs 2,046 |

| 15 | 12 | Rs 3,956 |

| 10 | 12 | Rs 8,400 |

| 5 | 12 | Rs 23,205 |

The sooner the parent starts planning for the child’s education and marriage the better. These are long term goals and need proper planning. This is the best gift that parents can give to their children. As a parent the sooner you sow the seeds of early investments, the bigger will be the fruit the tree will bear which will take care of your child’s all future needs, primarily education and marriage expenses.

Children’s Marriage Planning

Like education it is the same story for children’s marriage expenses (inflation). If you as a parent feel that today your daughter’s marriage will cost you Rs 7,00,000 then the same marriage will cost Rs 11.27 Lacs 5 years down the line if expenses increase (inflation) at the rate of 10%.

Sample Case Study

Let us consider the following case study to understand this thing better in simpler terms.

- Sharon has an 8 year old daughter Mini. Sharon needs to accumulate funds for her daughter’s marriage. The marriage is planned 16 years from now.

- According to Sharon, as on today, Mini’s marriage will cost Rs 4,00,000. If inflation (rise in costs) of 5% is assumed the same marriage will cost Rs 8,73,150 after 16 years.

- If Sharon wants to make a one time investment which will give her Rs 8,73,150 on maturity after 16 years, she will have to make a lumpsum investment of Rs 1,42,429 (assuming the investment earns a return of 12% p.a.).

But many of us don’t have lumpsum amount to invest and we prefer to make monthly investments. To accumulate this Rs 8,73,150 over a period of 16 years Sharon will have to invest Rs 1,615 per month if her investments will earn a return of 12% p.a.

Watch this video which shows you the effects of Inflation in Zimbabwe and how the paper money has lost all its value.

Conclusion

Last but not the least to end the article here is something for you all to ponder over your money in the bank savings account is earning an annual return of 3.5% and the annual average inflation rate (increase in cost of living) is 5-6%. So if you calculate the real return how much is negative return that you are making or how much is the value that your money is losing???? Think about it

This is a Guest post by Gopal Gidwani , He writes on his blog www.bachatkhata.com