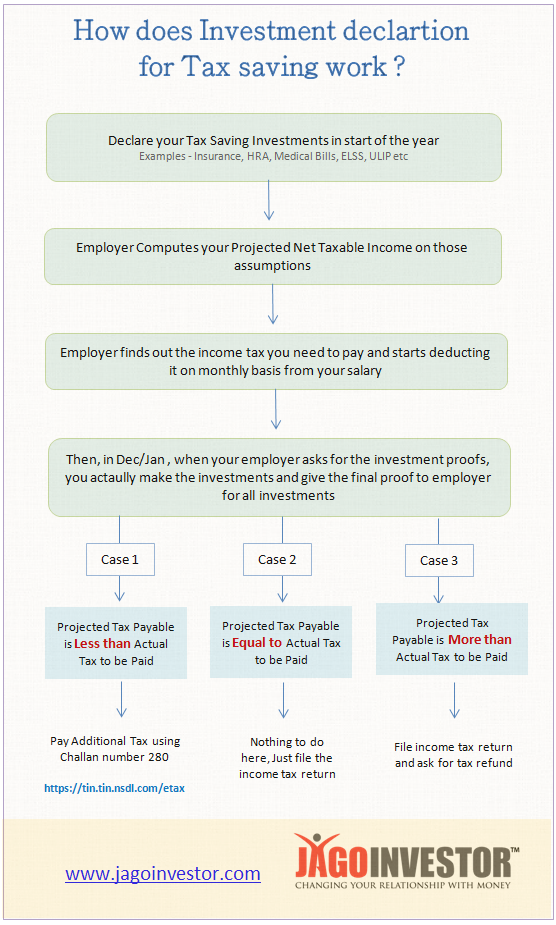

Every year, when the new financial year starts, employers ask their employees to declare their investments and give an idea about where will they invest to save the tax. There is a page on the companies’ websites, where each employee has to declare their investments. Come of the examples of the target options are life insurance premiums, ELSS investments, Rent, Ulips and home loan-related numbers.

Why do employers ask for this investment declaration?

The employer asks for this information because they want to approximate how much will be your final taxable income (after deducting the tax saved through 80C investments, HRA, Home loan and medical bills. So that they can cut a constant amount of TDS each month.

A lot of employees get a bit tensed thinking, what exactly they should mention while declaring the investments. They feel that at the end of the year, they will have to invest exactly in the same order in which they declared. However, this is not correct. All you need to do is invest the same amount declared at the start of the year into any tax-saving investments option.

For example – If you had declared that you will invest Rs 50,000 in LIC policy and Rs 30,000 in Tax saving mutual funds (ELSS). The total is Rs 80,000. Now your employer will deduct Rs 80,000 from your projected income for the year and arrive at net taxable income and find out how much is the tax you need to pay at the end of the year (projected). Now he will just divide it by 12, and find out the monthly number and start cutting that much tax each month from your salary.

Now when the month of Dec/Jan arrives, your employer asks you for investments proof. Now when you actually give it to them, they recalculate things and see if things are matching with what you declared at the start of the year or not.

There can be 3 scenarios here.

Case 1 – Amount Actually Invested Less than Amount declared in the start

In-case you were not able to invest up to the amount you declared, or you were not able to submit the documents to your employer on time, it means your employer will assume that you will not be able to do so, and that means that they have over estimated your tax saving and the tax paid by employer is lesser (because you owe more tax, due to less tax-saving investments) . In which case, the employer will recalculate your tax liability and now will adjust it with the next 1-2 month salary (Feb/Mar). Which means you get less salary in the last 1-2 months.

But, If you are able to finally invest for tax saving, then at the time of tax filing you need to declare it and ask for a tax refund from the IT department. It’s always a good idea if you can avoid this situation because then it takes a lot of time to get back your refund.

If for some reason, your employer does not cut the tax from your last month’s salary, then you directly owe the tax to govt. This can also happen if you have any other income source, which is not accounted for by the employer, in that case, you need to pay the tax to govt directly. You can do it online using Challan 280 on the IT department website. Then at the end of the year, you can file the returns.

Case 2 – Amount Actually Invested = Amount declared in the start

If you invest the same amount as declared at the start of the financial year, it means that your taxable income would be almost same as computed by your employer and the amount of tax you paid was equal to what you owe to the income tax department. In this case, there is nothing much you need to do. just file the ITR at the end of the year and everything should be pretty smooth unless you have income from other sources.

Case 3 – Amount Actually Invested More than Amount declared

It might happen that you declared only Rs 50,000 investments, but finally invested Rs 1,00,000 into tax-saving instruments, which means you saved more tax. However, your employer has been deducting the tax assuming your declaration for Rs 50,000 only, which means the employer was paying more tax to govt on your behalf. Now, this means you are entitled to get a tax refund and you can ask for it when you file the returns. Generally, it’s a good idea to declare the maximum possible investments in the start, let your employer assume you will do maximum tax saving (so that less tax is paid), and then make sure you actually invest the promised amount. In the worst case, if you fail to do so, better pay the tax at the end of the year or get less salary (be prepared for it)

This article from Bemoneyaware talks about this topic in much detail. Did you get clarity about investment proofs for your employer? Do you have any questions?