CIBIL has recently come up with Cibil Transunion Score 2.0 which it calls an improved version of the CIBIL Credit Score. This new Credit Score will help in a better identification of new borrowers (having credit history of less than 6 months) and help classify them into risky and not-risky categories.

More about CIBIL Score 2.0

The biggest change here is that the CIBIL Score 2.0 is for new borrowers who have a short credit history, i.e. 6 months. So now there will be two classes of borrowers

1. Less than 6 months of credit history

Any borrower having less than 6 months of credit history earlier used to get a score of 0. But with CIBIL 2.0 , they will get a score in between 1 to 5, where 1 represents high risk of default and 5 denotes least risk of default. This score between 1-5 will depend on parameters like 90 days overdue in any given month (for last 24 months), credit seeking activity (number of loan enquiries you make), type of credit (secured or unsecured) and the demographic (age , location etc.)

This move is going to help a lot of people who are very new to credit and have recently taken credit cards or have taken some kind of loan and need another loan. There have been instances that due to their short credit tenure, they didn’t have any credit score and a lot of bank rejected their applications for loan just because they didnt have one.

2. More than 6 months of credit history

For those who have more than 6 months of credit of any kind, for them the credit score will be in range of 300 to 900 score, just like earlier. However, it seems like this scoring method will consider only higher scores like 800+ as the better score. As per this firstpost article, it says that an old score of 751-800 will now be equivalent to something like 662-697 in the new score version .

For borrowers with more than six months of credit history, the old scoring criteria 300-900 remains, but for the lower score you get. For instance, the old score of 751-800 will be equal to 662-697 in the present one.

The newer version is initially made available only for CIBIL’s 862 member banks and financial institutions, after which it will be available for the customers as well, he said, without giving an exact timeline for the completion of the process.

Cibil Score 2.0 is a better Score

This new CIBIL score is said to be a better indicator of someone repayment capability. It has been designed keeping in mind the Indian market and the way consumer behavior is changing from last some years.

“CIBIL TransUnion Score 2.0 predicts risk more powerfully as this scoring model has been customized for the changing Indian market and consumer behavior. This scoring model will enable banks to better identify good customers, thereby enabling them to provide credit to more consumers and increase credit penetration and financial inclusion in the country.”

– said Mr. Arun Thukral, Managing Director, CIBIL

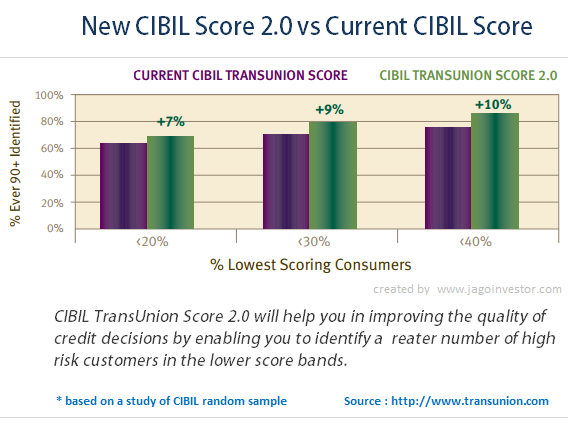

The new CIBIL score is tested by the company old random data and it seems to identify the risky customers in a more better way. Here is a snapshot of results I found out on transunion website. You don’t really need to understand this graph, just get that this identifies risky customers in an improved manner.

Now, The credit institutions that have adopted the new scoring model will decide on customer’s loan application based on this new score. So it would be interesting to watch out the credit score banks ask for giving loans .

What do you think about this new cibil score 2.0 and the changes which has taken place ?

We are happy to share that we have got a great response to our newly launched Jagoinvestor Wealth Club some days back . There are already 140 members and we are giving the discounted pricing to only 300 people . We are excited to share that we are moving towards our vision of creating a great dedicated closed community. Join the club if you feel you need to be present there.