Today I want to share some quick facts regarding Sovereign Gold Bonds which was announced in budget session and recently mentioned by our Prime minister.

RBI is going to issue something called Sovereign Gold Bonds for investors who want to benefit from the movement from Gold prices. It’s an alternative way to invest in gold apart from buying physical gold or through gold ETF or gold Mutual fund.

These bonds issue is part of the market borrowing program of govt of India, where it tries to borrow money from the public for the long term. So to understand it in brief, govt wants to borrow money from those who want to invest in gold and they would return back the money after X number of years which will be linked to the price of gold apart from a small interest.

10 FACTS about Sovereign Gold Bond Scheme you should know

Now let’s understand quickly what Sovereign Gold Bond Scheme is all about and some high-level important points every investor would want to know.

1. Issued by RBI and hence it’s safe and secure

These bonds are issued by Reserve bank of India and hence it carries a sovereign guarantee by Govt of India.

So in a way its 100% safe and secure and there are no chances of fraud or any issues happening in the future.

However, you need to know that the bond value is linked with the gold prices and hence the value of the bond can increase and decrease in the future depending on the gold price movement.

However, whatever is the maturity value will be paid to you and the guarantee is only for that. There is no assurity for any minimum value payment or any promise of return. One can hold the bonds in a single name or joint name as per preference.

2. First Batch of bonds available from Nov 5-20

As per a report, out of Rs 15,000 crore of bonds, the first batch of Rs 1,000 crore bonds are available from Nov 5 and the last date for application is Nov 20. The bonds are available for only residents Indian and NRI’s cant buys it. The bonds will be available at selected banks and post offices designated under the scheme.

I was not able to find exact locations, but I think all the major PSU banks in every city and some big post offices will be the contact point if one wants to purchase these bonds.

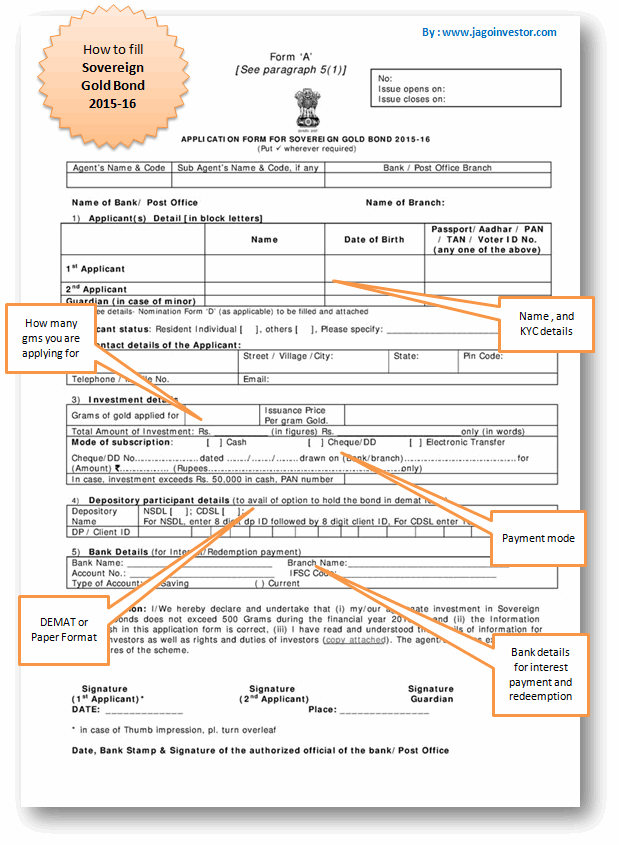

Below you can see a sample form and how it has to be filled. You can also download the form from his link

3. Amount of investment and Tenure

The minimum one has to buy 2 gms worth of gold bonds and the maximum can be 500 gms. So every normal middle-class person who wants some exposure in gold can buy it. The initial issue price is fixed at Rs 2,684 per gram. Which means a minimum initial investment would be Rs 5,400-5,500 at least.

Note that price fixed is a simple average of the closing price of the 999 purity gold, published by India Bullion and Jewellers Association Ltd (IBJA).

The bonds will be issued with an 8 yr tenure, however, an exit option will be available after 5th year onwards. The bonds can also be traded on stock exchanges if you have it in Demat form. However, I think it’s not going to work for most of the investors because that will get too complicated.

Also, you will be able to trade the bonds on markets only if the volumes are very good, otherwise it will be locked away and you will be able to get back the money only after the 5/8 yrs of time. You can read detailed FAQ’s on this scheme here

Also note that these bonds can be provided as collateral incase, you need any loans.

4. You will get interest of 2.75%

You will get interest of 2.75% interest on the initial value of investment (not the market price) every 6 months. I have not gone in details, but I think the way it will work is that if you invest Rs 1,00,000 in these bonds, then every 6 months you will get 50% of 2.75% of Rs 1 lac as interest, which would be Rs 1,375

5. Taxation on returns and maturity

Note that the interest you earn every 6 months will be taxable in your hands. Also at the time of maturity, the long-term capital gains will be applicable, which means that after applying indexation, you will have to pay 20% tax on the returns. Note that because KYC is done properly, you cant escape this.

6. KYC requirement

You will be able to buy these gold bonds only after the KYC is done for you. In simple terms, at the time of application, you will have to provide your identity and provide your PAN or Aadhar card etc and the payment can be done electronically, with cheque/DD or even CASH.

However, you will not be able to hide your identity. This will surely discourage those investors who want to convert their unaccounted money (CASH) into white money.

7. Investment in Paper or Demat Form

You can purchase the bonds in paper format or Demat holding as per your preference. Means if you want the bond in paper format, you will get a receipt and a bond that you can keep in your locker or at home and at the time of maturity you can give it back. Or you can hold it in Demat form and not worry about keeping the bond safely.

Who should not invest in these gold bonds?

I think that 5-8 yrs tenure is a long tenure and you can earn much better returns in this long term. Equity mutual funds would deliver better returns compared to this scheme. Hence if you are a young person below age 40, and are looking at wealth creation as your main goal, then you can give a miss to this scheme.

The return on the scheme (2.75%) is not to be considered and the gold returns historically have been around inflation only.

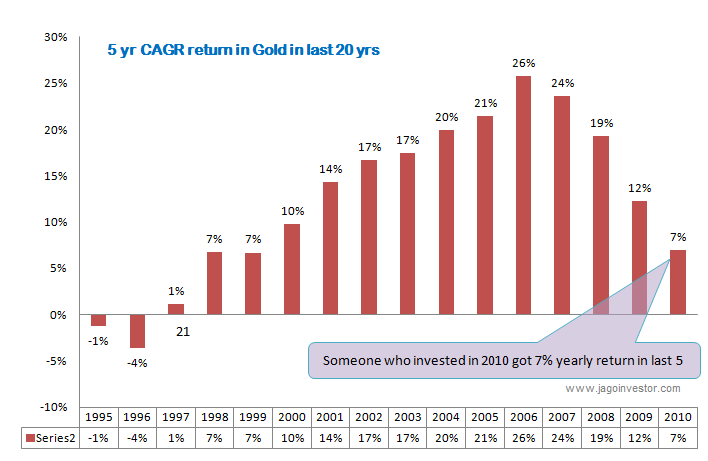

If you look at the below chart, you can see 5 yrs CAGR return of the gold investment. Note that for the tenure of 2000-2010 the returns have been very very good, but then if you look at someone who invested in the year 2010, they have just got a 7% CAGR return, which is very much in tune with long term gold returns.

So if we look at the optimal use of your investment to generate a decent return, I personally dont consider this as a great investment product. You can skip this.

Who can think of buying these bonds?

Now if we look at the other side, There are many investors who are very attached to gold and really want to invest in that. No logic will move them and no conversation of CAGR will make sense to them. So for those investors who were anyways going to buy physical gold or Gold ETF, can look at this scheme as a good alternative.

Anyways your investment value will move as per gold prices and on top of it, you will get 2.75% interest which you do not get in case of physical gold or gold ETF/funds. The best part of this scheme is that you don’t have to worry about the quality of the gold or where to store it as its all in paper format and no one is going to steal it from you.

The money will only come back to your bank account only which you have provided at the time of investment.

However, note that the investment in these bonds is going to be mainly illiquid in the very short term. If you buy physical gold, you get that liquidity in your hand and if you need money urgently you can sell off the gold. You will not get it here.

So overall, you are the right person to pick if this scheme is for you or not.

Please share what are your views on this scheme. Do you think it’s going to be a hit among investors?