Most of the people in India try to save income tax by investing the money in their spouse, children and parents name. We are going to explore this topic more deeper and help you understand the exact rules applicable and how you can save more tax legally, by gifting money to your family members.

Majority of people, just transfer the money to their family member account and invest that money, thinking that they will not be paying tax on that amount and it’s a smart way of gifting the money and avoid paying the tax. But that’s not correct. I have already written in detail about what is gift tax and certain exemptions when one don’t have to pay any tax on gifts received.

What most of the people do in real life is that, they just transfer the money to their family member bank account and invest that money in their name, assuming that by default it will help them in saving tax, because they have gifted away that money and because their family member has income below exemption limit, they also don’t have to pay any tax. However, it’s not that simple.

Now, let’s understand the tax implications of various people involved when a gift is given and what is the right way to save tax by gifting money.

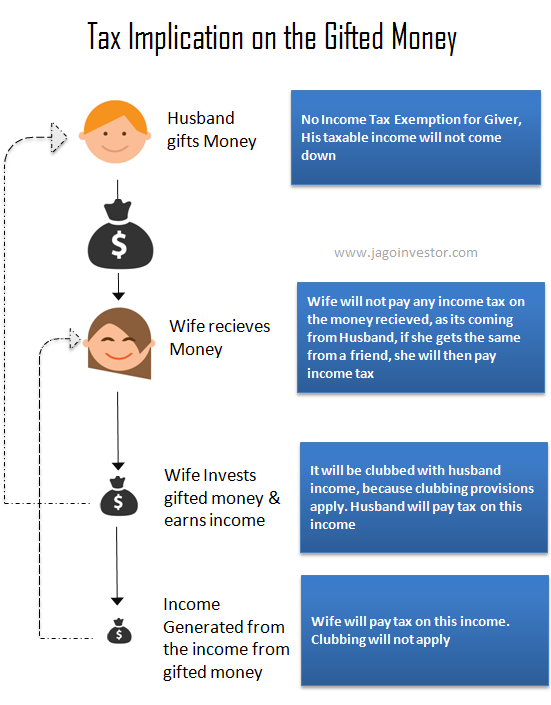

Let’s take an example – where husband earns Rs 10 lacs per annum, gifts Rs. 1 lakh out of that to his wife, who is a homemaker. Wife, then invests this Rs 1 lac in a Bank FD at the rate of say 10% interest per annum and earns Rs 10,000 as income.

This transaction has three parts and the tax implications as follows

- Tax Implication on GIVER (husband) for the amount gifted

- Tax Implication on receiver (Wife) for the amount received

- Tax Implication on the income earned, when the gifted money is invested.

Tax Implication on GIVER (husband) for the amount gifted

Let’s first talk about the tax implication for the person giving the gift.

The person, who gives the gift can never claim any income tax deduction or exemption from his/her income. Most of the people confuse the entire gifting implication and assume that the money which they have gifted to somebody will be reduced from their total taxable income and they have to pay tax only on the balance income. But that is not correct.

In the above example, the husband earns Rs 10 lacs per annum and should ideally pay tax on that full amount after deducting any income tax exemption they get from various sections like 80C and others.

How most of the people think?

Now husband can argue that the Rs. 1 lac which was gifted to his wife should be reduced from his total taxable income and he should be paying taxes only on Rs. 9 lacs. But this is simply not allowed!

Because – if this is allowed, then everyone will gift all their salary or business income to wife or parents and no one will pay tax at all, because they don’t have any income now as the entire income is gifted. That does not make any logical sense.

So in the above example, husband has to pay tax on his income of Rs 10 lacs subject to all the benefits as available to him under various sections of the IT act and let’s say that his total tax after all tax deductions (80C) comes to Rs. 75000/- and his post-tax income is Rs. 9.25 lacs. He can gift whatever he wants out of this post-tax income.

Tax Implication on Reciever (Wife) for the amount received

Now let’s take the tax implication for wife, who got the money in our example. Will she pay income tax on this gift received or not?

The answer is NO

Because this is a gift from her husband, who comes under the specified list of relatives who are exempt under the income tax act from gift tax liability. If she had got this 1 lacs from her friend or some random person, who is unrelated to her. In that case, this 1 lac would be considered her income for the year and taxed in her hands, but here she will not pay any tax on this 1 lac.

Below is the list of relations from whom if one gets any gift, they don’t need to pay any tax.

- Your spouse

- Your brother or sister

- Brother or sister of your spouse

- Brother or sister of either of your parents

- Any of your lineal ascendants or descendants

- Any lineal ascendant or descendant of your spouse

- Spouse of the persons referred in above points

So the point is that, if one gets a gift from close family members, like spouse, parents, siblings etc, the receiver does not pay any income tax on the money received.

Tax Implication on the income earned, when the gifted money is invested

Now the tricky part comes in.

What happens when the gifted money is invested in products like FD’s or shares? Let’s say that the wife invests this Rs. 1 lacs in a bank FD and earns an interest @10% annually, ie Rs 10,000.

Now who will pay the tax on this interest of Rs 10,000?

Husband or Wife?

I know most of the people will think that its wife, because once she gets the gift, now its her money and she is 100% owner of that money and any income generated from that should also be her own income and she should pay the income tax on that amount. So here in this case, if wife does not have any other income apart from this Rs 10,000 , then her total income for the year will be Rs 10,000 only and as its lower than the exemption limit, so she will not be paying any tax and won’t be required to file any income tax returns.

However in real life, this is not how it works.

In this case, IT department clearly knows that people will gift the money to their spouse who does not have any income, so that the whole income generated become’s tax-free. To combat this, there is something called as Income Clubbing provisions, which adds the income of one person in other income in certain cases, and that will apply in this case.

So in the above example, this interest income of Rs. 10,000 would not go tax-free and will be clubbed with husband’s income and he has to pay tax based as per the applicable tax slab.

So if, husband earned Rs 10 lacs a year, now this Rs 10,000 will be his additional income making his total yearly income as Rs 10.1 lacs.

But Income earned from the income earned is not clubbed

One interesting point to note is that any further income generated from the income is not clubbed further and that will be 100% income of the person who got the gift.

So in above example, when wife gets Rs 1 lacs as gift, and earns Rs 10,000 as the income, that Rs 10,000 will be clubbed with income of husband, but when this Rs 10,000 is further invested into FD again and earns Rs 1,000 income, this time – it will be wife’s income and not husband.

So now, how you can apply this rule in real life? Here is a tip !

Let’s say you have Rs 10 lacs with you. If you invest this money in your name, you will earn Rs 1 lac as income from it and pay tax on it, but next time again when you invest this 1 lac, you will earn Rs 10,000 and then again have to pay tax on it because it will be your own income.

What is the alternative way ?

What you can do here is that, you can invest Rs. 10 Lakhs in your wife’s name and earn an interest of Rs. 1 lac. This Rs. 1,00,000 will be clubbed in your income for the computation of income tax; which was going to happen anyways. however, when your wife further invests this 1

However, when your wife further invests this 1 lac in another FD and earns Rs. 10,000 (assuming 10% interest) as interest on it, this time it will be considered as her income and will not be clubbed with your income. Assuming husband in 30% tax bracket, it’s a saving of Rs 3,000. Might look small, but its one of the ways to save the tax by Rs 3,000 in a legal way.

The image below shows you the rules and how the tax implication will apply in various cases explained above

3 tricks to save more tax legally by investing in family members name?

Now you are clear about the tax implication on person giving the gift, on person who is taking the gift and on the income generated from the investment done by the gifted money.

Now let’s see some things, which an investor can do to legally save tax in a more smart manner by involving their family members and that too in a 100% legal manner.

Trick #1 – Invest the gifting money into tax-exempt or low-tax instruments

Clubbing provisions will not apply when the gifted money is invested in any investment option which are tax exempt by default. Or one can invest in lower tax options.

For example – rather than a normal FD, if the money is invested in shares of a listed company and sold after 1 yr or an ELSS mutual fund, and sold after 3 yrs lock in period, then in that case the profits which attract on 10% tax as equity taxation after recent budget is only 10% without indexation, that too above Rs 1 lac limit

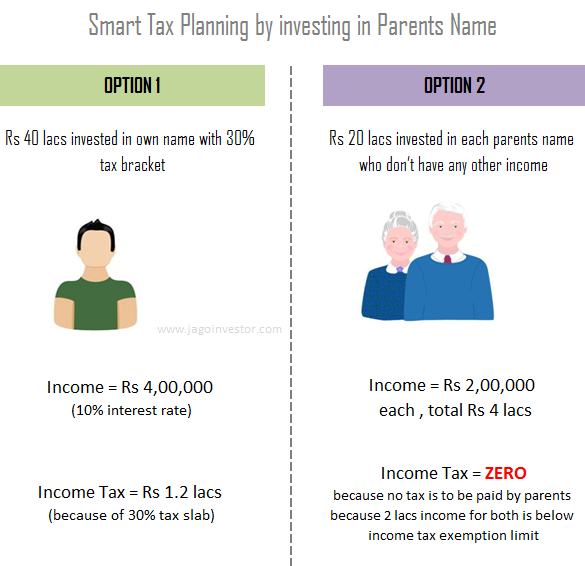

Trick #2 – Invest money in your parents name

You can save taxes by gifting money or by giving loans to your parents or in-laws because clubbing provisions does not apply in these cases. This is because any income generated on the gifted or loaned money to parents is purely parents income and will be taxed in their hands only.

Let’s see an example.

Assume that you have Rs 40 lacs in your hand which you want to invest and your father and mother are both senior citizen and have no income from any source. Now what you can do is, gift Rs 20 lacs to each parent and let it get invested in a bank FD at an interest rate of 10% (just an assumption)

Now both of them will get 2 lacs as the interest income individually and this is their only income in a year and will be below the exemption limit (Rs 3 lacs for senior citizens) . So there won’t be any income tax to be paid by them.

This way you have invested Rs 40 lacs in family name itself with ZERO income tax.

On the other hand if this 40 lacs was invested in FD on a main bread-winner name who is into 30% bracket, he would have paid 30% income tax on 4 lacs of interest, which is Rs 1.2 lacs. This whole 1.2 lacs is saved.

Even if parents are having additional source of income, it’s still beneficial to gift the money to them as it would lower the income tax outgo, because of the lower slab rates and applicable exemption limit.

You can apply the same logic and invest in property in parents name and let the income come to them and enjoy the tax-free income subject to exemption limits.

Trick #3 – Invest money on Major Children Name

In the same way, even the money gifted to major children (above 18 yrs) will not be clubbed in your hand. So in case you have children who are 18 years or older who are either studying or earning at a lower tax slab than you, then gifting your surplus money and investing in their name will neither attract gift tax nor clubbing of income will apply.

Income earned out of investments made by your major Children out of the gifts given by you will be taxed in their hands only.

This is really a great thing because if you are going to pay for some upcoming children education goal or marriage goal, then instead of investing the money in your name and funding the goal later, why not just gift the money to the child and invest it in their name itself. When the goal arrives, the money can then be used, but for years there will be no tax liability (or lower tax) and you will save a good amount of income tax.

You may even consider giving interest-free loans to your children as it is lawful and can help you save you more taxes. However when the children are minor then clubbing provision will attract except in cases where the income is earned by the child due to his or her skill or talent.

Plan your Income Tax with help of a CA

There are lots of ways one can save income tax by restructuring their investments in family members name. Generally people do not have much time to plan all this and for years they pay higher income tax and never optimize it. If you really want to work on this. I suggest hire a good CA for his consultancy services. This can be your family CA or some friend if you want or some external person whom you can trust.

Let me know what new ideas are coming to your mind right now after reading this article? What are your views on this? Please share it on comments section.

|

This article is guest post by Rishabh Parakh, a Chartered Accountant by Profession & Founder Director of Money Plant Consulting, which provides services related to income tax filing, scrutiny cases and various other CA related services with operations in Pune, Mumbai and expanding to other regions. |