Today I am going to talk about something which is one of the extremely important tool for risk management and also something which is encouraged if you want stable returns from your investments. We are going to talk about the investments in Equity and Debt.

How Re-balancing the portfolio will help in –

- Risk Management

- Stability

- Maximize returns

Understand the pros and cons of Equity and Debt

EQUITY

Pros : High returns, Low risk in Long term, High Liquidity

Cons : Risky, not suitable for short term investment

DEBT

Pros : Stable and assured returns, Good investment for short term goals

Cons : Low returns

Equity + Debt :

When we combine Equity and Debt, returns are better than Debt but less than Equity, but at the same time risk is also minimized compared to Equity and Debt, and when we apply technique of Portfolio Rebalancing, both risk and returns are well managed.

What is Portfolio Rebalancing?

The first step to understand is that each person must divide his investments into Equity and Debt in some ratio, it can be 40:60, 50:50, 60: 40, 75:25 or any ratio, The ratio depends on a persons risk taking capability and return expectation.

For an example let take the ratio to 60:40, portfolio rebalancing is nothing but rebalancing your portfolio in same ratio, in case they got changed after some months or years, as you wish. Preferably the good time is every 6 months or 1 yr, but not 15 days or 1 month.

Why Do we do it?

You have to understand that each person should concentrate on both returns and risk.

Case 1 : Equity:Debt goes up.

Action : Decrease the Equity part and shift it to Debt so that Equity:Debt is same as earlier.

Reason : As our Equity has gone up, we could loose a lot of it if some thing bad happens, we shift the excess part to Debt so that it is safe and grows at least.

Case 2: Equity:Debt Goes Down.

Action : Decrease the Debt part and shift it to Equity, so that Equity:Debt is same as earlier.

Reason : As out Equity part has decreased, we make sure that it is increased so that we don’t loose out on any opportunity.

Limitations Lets also talk about the limitations of this strategy, once your equity exposure has gone up, if you rebalance and bring down your Equity Exposure, you will loose out on the profits if Equity provides great returns after that, or if your Equity exposure as gone down and you bring up your exposure from Equity and if Equity does bad, then you will loose more.

Understanding the Game of Equity and Debt

But, we already said in the start that our primary concern is managing risk and profit is secondary. Let us understand that markets are unexpected and they can go in any direction, so better be safe than sorry. Many people are confused that if there equity has done very well then shall they book profits and get out with money and wait for markets to come down so that they can reinvest.

Portfolio rebalancing is the same thing but a little different name and methodology, so once you get good profit in something which was risky you transfer some part to non-risk Debt.

When we say Equity we mean shares or mutual funds which are related to Stock markets, which tend to go up and down, if it goes up, there are high chances that it will come down and when it comes down, its highly probable that it will move up again.

Lets us now see the most interesting part : Examples

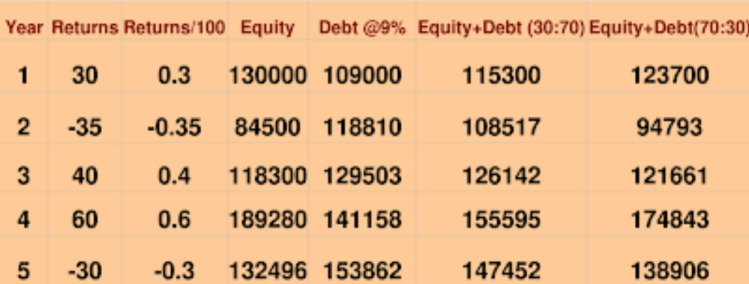

Ajay has Rs 1,00,000 to invest and he want to invest it for 5 yrs and the 5 yrs returns are 30%, -35%, 40%, 60% and -30% .

Lets look at his money and its growth in 3 different mode

– Only Equity

– Only Debt

– Equity + Debt in some ratio (without Portfolio Rebalancing)

(click on this image to see in large resolution)

We can see here that Debt performed better than Equity, because of the uncertain movement in returns, also the Equity+Debt performed better than Equity but not Debt.

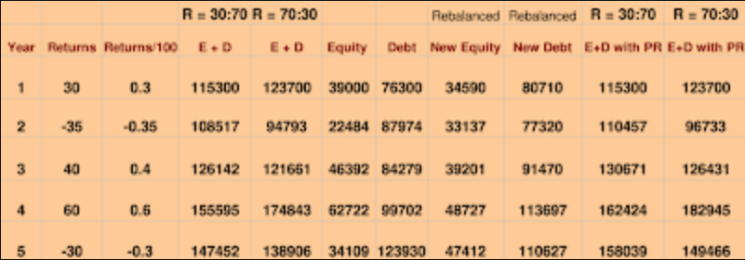

Let us now see the performance of Equity + Debt (with portfolio rebalance)

So now, every time our Equity and Debt ratio changes, we will rebalance it.

Ratio = 30:70

Investment = 1,00,000

Equity = 30,000

Debt = 70,000

At the end of 1st year (Equity return = 30% , and debt = 9%) :

Equity = 30,000 * (1.3) = 39,000

Debt = 70,000 * (1.09) = 76,300

Total Capital = 39,000 + 76,300 = 1,15,300

Now we will rebalance the portfolio

Equity = 30% of 115300 = 34590

Debt = 70% of 115300 = 80710

Now This is our new Equity and Debt investment

At the end of 2nd year (Equity return = -35% , and debt = 9%) :

Equity = 34590 * (1-.35) = 22484

Debt = 80710 * (1.09) = 87974

Total Capital = 22484 + 87974 = 110457

Now we will rebalance the portfolio

Equity = 30% of 110457 = 33137

Debt = 70% of 110457 = 77320

In this way we keep rebalancing the portfolio and lets see its performance for 5 yrs

(click on this image to see in large resolution)

Here, you can see that The column (E+D with PR) is the our main column which shows the performance with portfolio rebalancing. Here we have example for two ratio’s 30:70 and 70:30, we can clearly see that at the end of every year the final corpus for rebalanced portfolio was always greater than the non-balanced portfolio for both the ratio.

For ratio 30:70

Year 1 : 115300 vs 115300

Year 2 : 110457 vs 108517

Year 3 : 130671 vs 126142

Year 4 : 162424 vs 155595

Year 5 : 158039 vs 147452

For the 70:30 ratio also we can see that rebalanced portfolio outperformed the non-balanced portfolio.

Also you can see that for most of the years re-balanced portfolio outperformed “Only Equity” and “Only Debt” except 1st year and 4th year.

1st yr is very easy to understand why it happened and for 4th year, the returns were positive again after 3rd year and we made more profit in “Only Equity” portfolio because of high concentration on Equity side, but you can see that in 5th year, when there was a negative return of -35%, then the “Only Equity” fell heavily, but the rebalanced Portfolio fell very little because we have rebalanced it already and dropped our Equity Exposure to be safe.

Conclusion

So at last the question is what is the ultimate conclusion of all this talk.

Each person has his own Equity and Debt diversification, if the person is high risk taker his Equity component will be high else it will be less, every time your Equity and Debt component changes you have to see that it matches your risk profile, if it does not you bring it back to your level.

By bringing Equity exposure from high levels to your level, you are managing the risk you can take and by increasing the Equity exposure to your level back (in case it went down), you are making sure that you don’t miss out the chance.

Other reason is that Debt always increases, Every time your money goes up in Equity from your comfort level, you take that money which is earned by risk and shifting it to a safe place which will rise for sure though with less speed. Equity is linked with Stock Market and they tend to go up and down always and you don’t know when will it happen. So better manage that risk by Portfolio Rebalancing.

Please comment of this article to let me know how you feel about this article, Feel free to comment on anything which you feel is wrong .

Also, the example taken for this article was self made and does not represent any real life situation, but for sure its possible and similar scenarios have happened in our Stock Markets