Most of the NRI’s who are new to mutual funds have this confusion if they can invest in mutual funds in India or not?

In this article, I will share with you all the rules, restrictions and some of the important points that NRI investors should know before investing in Mutual funds.

Can NRI invest in mutual funds in India?

The simple answer is YES. NRI’s can invest in mutual funds in India.

In the case of NRIs, no special approvals are to be taken from SEBI or RBI, however the documentation can be little more and in case of US and Canadian NRI’s, there are some limitations in terms of which AMC’s they can invest in.

So let’s look at the basics first.

NRE or NRO accounts should be used

An NRI can invest in mutual funds only from an NRE or NRO bank account. The Non-Resident External Rupee (NRE) account is a rupee account from which money can be sent back to the country of your residence and the Non-Resident Ordinary Rupee (NRO) account is a non-repatriable rupee account.

Here is a detailed 30 min video explaining NRE/NRO accounts along with various other basics for NRI’s

Which means that if you are living in particular country and you want to invest in Indian mutual funds, but later in future, you want to redeem back the money and use it back in your country, then its better to invest by NRE account as its repatriable, otherwise NRO account can be used.

Procedure for Investing

For an NRI the procedure of applying in a mutual fund is similar to the one followed by residents.

Step #1 – KYC (Know your client)

This is one-time documentation required to invest in mutual funds and its a requirement set by SEBI. For doing your KYC, the following documents are required.

- Copy of Passport is compulsory

- Copy of Overseas Address Proof (in English)

- Copy of Indian PAN card

- Two passport size photos

- The fully Filled KYC form

You can complete your KYC either by taking support from a mutual fund distributor or directly submitting the filled KYC form at CAMS or KARVY Offices in your city by personally visiting them.

Important Points:

- Incase of POI, the POI card is also required in documentation

- In case your overseas address is not in English, you need to get it translated by a translator in your city and get their stamp

- In case you do not want to travel to India just for making investments, you can always give POA (Power of attorney) to someone trusted who can do the process for you. In our case, a lot of NRI readers of jagoinvestor, courier us their documents and we help them in doing their KYC and starting their investments.

Once your KYC form along with required documents is submitted to the registrars(CAMS, Karvy, Sundaram, etc.) It will take 4 to 5 days in registration. Once it is registered you can start investing into mutual funds. You will get the alert about the registration via mail or SMS. However, if you want you can check the status of your KYC by entering your PAN in either of the links below:

https://kra.ndml.in/

https://camskra.com/

https://www.karvykra.com

https://www.cvlkra.com/

https://www.nsekra.com/

You can also refer to these links for downloading the KYC application form.

FATCA

There is something called FATCA, which is also added in KYC documentation these days and it’s done for all investors. However, its mainly required for US and Canada investors. One has to provide information like country of tax residence, tax identification number from that country, country of birth, country of citizenship, etc.

Once the FATCA is submitted, NRI can start investing in mutual funds.

NRI’s from the US and Canada

Now, since the last few years – most fund houses in India don’t allow NRIs from the US and Canada to invest with them due to cumbersome compliance requirements under FATCA or Foreign Account Tax Compliance Act. When FATCA came into place, fund houses stopped taking investments from the USA and Canada because of the complexity associated with the compliance. However now, following fund houses accept NRI investments from US and Canada

- Birla Sun Life Mutual Fund

- SBI Mutual Fund

- UTI Mutual Fund

- ICICI Prudential Mutual Fund

- DHFL Pramerica Mutual Fund

- L&T Mutual Fund

- PPFAS Mutual Fund

- Sundaram Mutual Fund

Some of these fund houses have certain conditions on which they allow investors based in the USA and Canada to put money in their schemes. For example, ICICI Prudential AMC, Birla Sun Life Mutual Fund and SBI Mutual Fund allow investments only through the offline transaction with an additional declaration signed by the client. Similarly, L&T Mutual Fund doesn’t allow US and Canada based clients to invest in close-ended funds.

So, if you are the US or Canada NRI then look after the procedure and norms of Mutual funds in regards to NRIs of US/Canada before investing. We help a lot of our US and Canada clients to invest in mutual funds by making sure that their portfolio is designed well out of these limited sets of AMC which allows investments.

What if I was investing in mutual funds and moved to the USA, now I am an US NRI??

In this case, if the AMC you were investing with, continues to accept US NRIs then you just need to update the documents and have your FATCA verified, else you can just keep your investments as it is.

How do redemptions work for NRI?

When an NRI investor redeems the money from the mutual funds, the amount is credited back to your bank account after deduction of the applicable taxes in the form of TDS. Below are the taxation rules

NRI Taxation rules

NRI investors often fear that they will have to pay double tax when they invest in India. Well, this will not be the case, if India has signed the Double Taxation Avoidance Treaty (DTAA) with the respective country. For instance, India has signed this treaty with the US. Hence, you can claim tax relief in the US, if you have already paid taxes in India.

So if you have already paid X amount in India as tax, and If your taxation in the current country is Y, then you just need to pay Y-X tax in your country, provided the double taxation avoidance treaty is signed (in most cases its there for sure). Some documentation will be required for this benefit.

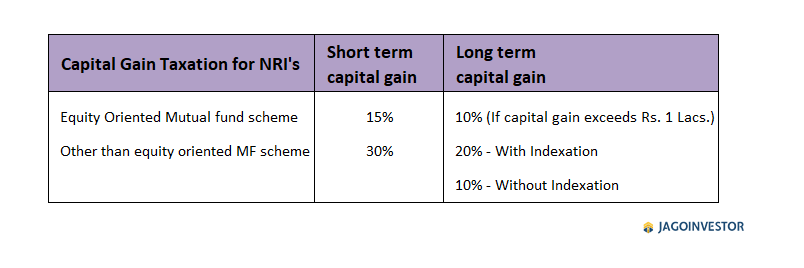

Equity and Debt taxation

The gains from equity mutual funds (funds where the composition of equity and equity-related instruments in the portfolio is 65% and above) are taxable based on the holding period. Short term capital gains (holding period 12 months or less than 12 months) attract tax at the rate of 15%. However, Long Term Capital Gains (holding period more than 12 months), in excess of Rs 1 Lakh, are taxable at the rate of 10%.

In case of debt funds (Hybrid funds with less than 65% equity exposure, Gold funds etc all are Non-Equity funds) Short Term Capital Gains (holding period less than 3 years) are taxable at the rate of 30%. Holding the fund for more than three years will result in a 20% tax on the gains with indexation benefit. LTCG on non-listed funds will be taxed at 10% without indexation.

Below given table shows the rate of TDS for NRI redemption on the basis of different holding periods and the type of funds.

If you are an NRI and you wish to start investing in Mutual funds, you can contact our team here.

If you are looking for Financial Planning, then visit our NRI Financial Planning page here

We have more than 100+ NRI clients across the globe who are doing their wealth creation using our help. We will help you in all the process and investing process.

We hope this article cleared the confusion about rules, regulations and taxation part of NRI investing.