As human beings, we feel that our topmost priority in life is to take care of our near and dear ones. These responsibilities have many forms – providing the best education to your children, ensuring that your parents are financially independent, or securing the lifestyle of you and your spouse post your retirement. In order to fulfill these responsibilities, you need a solution that will enable you to save towards these goals.

ICICI Pru Smart Life – is a savings and protection oriented Unit Linked Life Individual Product. This plan offers multiple choices on how to invest so that you can accumulate funds towards your desired goals while providing you with a life insurance cover to protect those goals even in your absence.

In this policy, the investment risk in investment portfolio is borne by the Policyholder. Unit linked Insurance products do not offer any liquidity during the first five years of the contract. The Policyholder will not be able to surrender/withdraw the monies invested in unit-linked insurance products completely or partially till the end of the fifth year.

Features of this policy –

i) Comprehensive protection to secure your goal –

In the unfortunate event of the death of the Life Assured,

- Lump-sum payment of Sum Assured – to take care of any immediate liabilities on the family.

- Waiver of all future premiums payable under the policy is available, provided all due premiums have been paid. Units will continue to be allocated as if the premiums are being paid – to ensure that your savings for your desired goal continue uninterrupted.

ii) Choice of portfolio strategies –

Select a portfolio strategy of your choice from,

- Fixed Portfolio Strategy – Option to allocate your savings in the funds of your choice from a diverse suite of funds.

- LifeCycle based Portfolio Strategy 2 – A unique and personalized strategy to create an ideal balance between equity and debt, based on your age.

iii) The flexibility of premium payment –

Pay premium just once, for a limited period or for the entire policy term.

iv) Liquidity –

Fund any intermediate financial need through Partial Withdrawals, any time after the completion of five policy years.

v) Loyalty Benefits –

Get rewarded with Loyalty Additions and Wealth Boosters on staying invested with us over the long term.

vi) Choice of Protection Levels –

One can choose from various protection levels available as per their needs.

vii) Increase and Decrease of premium –

An increase or decrease in premium is not allowed in this policy.

viii) Loan –

The Company will not provide loans under this policy.

ix) Tax Benefit –

The tax benefit on premium paid is allowed in this policy.

Benefits of this Policy –

a) Death Benefit –

i) On the death of the Life Assured, while money is not in the Discontinued Policy Fund (DP Fund), the Death Benefit payable will comprise of two parts –

- Lump-Sum Benefit – A benefit paid out at the time of claim to take care of any immediate liabilities of the family.

- Smart Benefit – A deferred benefit that ensures that your savings for your desired goal continue uninterrupted.

The Lump Sum benefit is higher of the two amounts –

- Sum Assured

- Minimum Death Benefit

Minimum Death Benefit = 105% of the total premiums including Top-up premiums if any received up to the date of death. For the purpose of this product, Sum Assured is deemed to include the Top-up Sum Assured, if any.

ii) On the death of the Life Assured, while money is in the DP Fund, the Death Benefit will be the DP Fund Value. Thereafter this policy shall terminate and all rights, benefits, and interests under this policy shall be extinguished.

b) Smart Benefit –

Secure your goal with Smart Benefit. Under this benefit, following the date of death of the life assured, provided all due premiums have been paid, units equivalent to the installment premium will be allocated by the Company on the subsequent premium due dates. This benefit is not applicable to the One Pay option. On the death of the Life Assured, the following conditions apply –

- The Fund Value including Top-up Fund Value, if any, will remain invested in the respective funds and portfolio strategies as on date of death of the Life Assured.

- Only the Fund Management Charge and Policy Administration Charge will be levied. Units will be allocated as if Premium Allocation Charges are being deducted. Life Insurance Cover will not apply and mortality charges will not be deducted.

- The policy cannot be surrendered. No policy alterations will be allowed. The Nominee will not be eligible for making partial withdrawals, paying top-up premiums, performing switches, renewing Automatic Transfer Strategy (ATS), redirecting premium, effecting a change in portfolio strategy, opting for settlement option, increasing or decreasing premium payment term, increasing or decreasing Sum Assured, increasing or decreasing policy term.

- Loyalty Additions and Wealth Boosters, as described below will continue to be allocated to the Fund Value.

c) Maturity Benefit –

On maturity of the policy, you will receive the Fund Value including the Top-up Fund Value, if any. This is paid irrespective of the survival of the life assured till the maturity date.

You will have an option to receive the Maturity Benefit as a lump sum or as a structured payout using the Settlement Option. This option is available only where the Life Assured and the Policyholder are the same and the Life Assured survives till the end of the policy term.

The following conditions are applicable to choosing settlement option –

- With this facility, you can opt to get payments on a yearly, half-yearly, quarterly or monthly (through ECS) basis, over a period of one to five years, post maturity.

- At any time during the settlement period, you have the option to withdraw the entire Fund Value. •During the settlement period, the investment risk in the investment portfolio is borne by you.

- Only the Fund Management Charge, switch charge, and mortality charge if any would be levied during the settlement period.

- No Loyalty Additions or Wealth Boosters will be added during this period.

- Rider cover shall cease on the date of maturity.

- You may avail the facility of switches as per the terms and conditions of the policy. Partial withdrawal and CIPS will not be allowed during the settlement period.

- In the event of the death of the Life Assured during the settlement period, Death Benefit payable to the nominee as a lump sum will be –

Death Benefit during the settlement period = A or B whichever is highest

Where,

- A = Fund Value including Top-up Fund Value, if any

- B = 105% of total premiums paid

On payment of Death Benefit, the policy will terminate and all rights, benefits, and interests under the policy will be extinguished.

- On payment of the last installment of the settlement option, the policy will terminate and all rights, benefits, and interests under the policy will be extinguished.

d) Loyalty Additions and Wealth Boosters –

The company will allocate extra units as below –

Loyalty Additions, Additional Loyalty Additions, and Wealth Boosters will be equal to the above percentage of the average of the Fund Values on the last business day of the last eight policy quarters. These units will be allocated among the funds in the same proportion as the value of total units held in each fund at the time of allocation.

Allocation of Loyalty Additions units, Additional Loyalty Additions units, and Wealth Boosters units is guaranteed and shall not be revoked by the Company under any circumstances. The above additions will not be added if your monies are in the DP Fund.

e) Rider Benefit –

The charge for this rider will be deducted by the cancellation of units on a monthly basis.

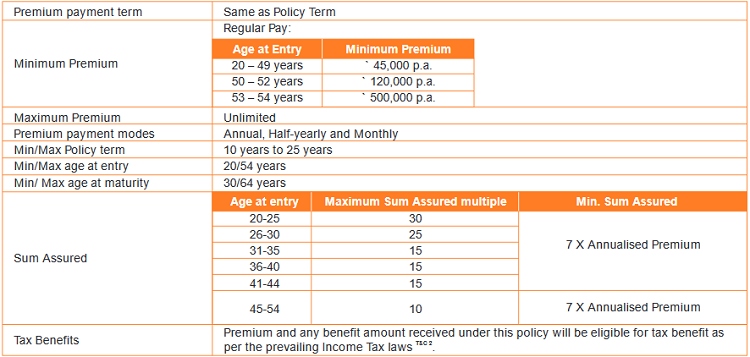

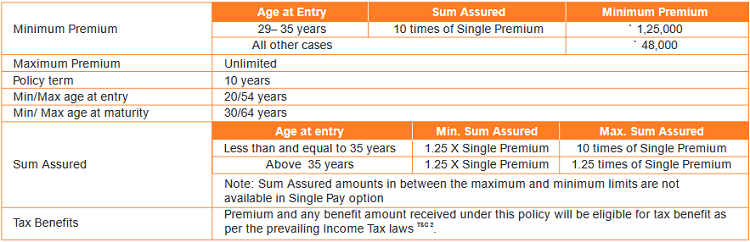

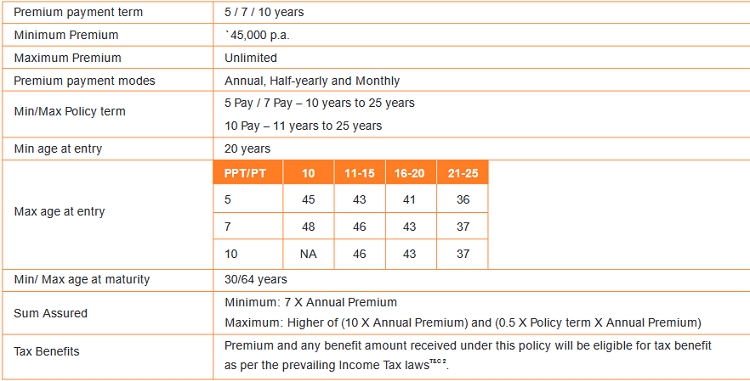

Eligibility Conditions of the Policy –

a) For Regular Pay –

b) One Pay –

c) Limited Pay –

Is switching between funds allowed?

You have the option to switch between the available funds as and when you choose to, depending on your financial priorities and investment outlook. Switching will be allowed provided the money is, not in the DP Fund. This feature is only available if you have all your funds in the Fixed Portfolio Strategy at the time of switching and minimum value of a switch is Rs 2000. This feature is not available if your money is invested in the LifeCycle based Portfolio Strategy 2.

Is Top Up allowed in this policy?

You can invest any surplus money as Top-up premium, over and above the base premium(s), into the policy. The following conditions apply on Top-ups –

- The minimum Top-up premium is Rs 2,000

- Your Sum Assured will increase by Top-up Sum Assured when you avail of a Top-up. Limits on Top-up Sum Assured multiples are the same as those applicable for the One Pay premium payment option and are based on the age of the life assured at the time of paying the Top-up premium.

- Top-up premiums can be paid any time except during the last five years of the policy term, subject to underwriting, as long as all due premiums have been paid, provided the monies are not in the DP Fund.

- A lock-in period of five years would apply for each Top-up premium for the purpose of partial withdrawals only.

- At any point during the term of the policy, the total Top-up premiums paid cannot exceed the sum of base premium(s) paid till that time.

- The maximum number of top-ups allowed during the policy term is 99.

What is Change in portfolio strategy (CIPS)?

You can change your portfolio strategy once every policy year, provided the money is not in the DP Fund. This facility is provided free of cost. Any unutilized CIPS cannot be carried forward to the next policy year.

What is premium redirection?

This feature is applicable only if you have opted for the Fixed Portfolio Strategy and provided the money is not in the DP Fund. If you have selected Fixed Portfolio Strategy, at policy inception you specify the funds and the proportion in which the premiums are to be invested in the funds. At the time of payment of subsequent premiums, the split may be changed without any charge. This will not count as a switch. This benefit is not applicable to the One Pay option.

Are Partial withdrawals allowed in this policy?

Partial Withdrawals are allowed after the completion of five policy years provided the money is not in the DP Fund. You can make an unlimited number of partial withdrawals as long as the total amount of partial withdrawals in a year does not exceed 20% of the Fund Value in a policy year. The partial withdrawals are free of cost.

The following conditions apply to partial withdrawals, they are as follows –

- Partial withdrawals are allowed only after the first five policy years.

- Only for the purpose of partial withdrawals, the lock-in period for Top-up premiums will be five years from the date of payment.

- Partial withdrawals will be made first from the Top-up Fund Value, as long as it supports the partial withdrawal, and then from the Fund Value built up from the base premium(s).

- Partial withdrawal will not be allowed if it results in the termination of the policy.

Is it allowed to decrease the sum assured in the policy?

You can choose to decrease your Sum Assured at any policy anniversary during the policy term provided all due premiums till date have been paid, monies are not in the DP Fund.

- The decrease in Sum Assured will not change the premium payable under the policy.

- The decrease in Sum Assured is allowed up to the minimum allowed under the given policy.

- Such decreases would be allowed in multiples of Rs 1,000, subject to limits.

- Once decreased, the Sum Assured cannot be increased.

Is it allowed to decrease in Policy Term?

- You can choose to decrease your policy term by notifying the Company.

- The decrease in terms is allowed subject to the Policy terms allowed under the given policy.

- If the Policy Term is amended, all future charges will reflect the updated Policy Term.

- Once decreased, the Policy Term cannot be increased.

Can I surrender the policy?

During the first five policy years, on receipt of intimation that you wish to surrender the policy, the Fund Value including Top-up Fund Value, if any, after deduction of applicable Discontinuance Charge, shall be transferred to the Discontinued Policy Fund (DP Fund). The proceeds of the discontinued policy shall be refunded only upon completion of the lock-in period.

If the policy is not revived, you or your nominee, as the case may be, will be entitled to receive an amount not less than the Fund Value including Top-up Fund Value, if any, which was transferred to the DP Fund, on the earlier of death and the expiry of the lock-in period.

Currently, the lock-in period is five years from the date of commencement of the policy. On surrender after completion of the fifth policy year, you will be entitled to the Fund Value including Top-up Fund Value, if any.

Is there any grace period in this policy?

The grace period for payment of premium is 15 days for monthly mode of premium payment and 30 days for other modes of premium payment.3

Can I revive my lapsed policy?

The treatment of withdrawal of surrender requests in the first five policy years is the same as a revival of a policy where the premium is discontinued. In case of surrender during the first 5 policy years or premium discontinuance during the first five policy years, you can revive the policy by paying overdue premiums within three years from the date of the first unpaid premium.

On revival, Discontinuance Charge previously deducted will be added to the DP Fund Value and Policy Administration Charge and Premium Allocation Charge, which were not collected while money is in the DP Fund, shall be levied. The money will be invested in the funds in the same proportion as on the Date of Discontinuance, at the NAV as on the date of such revival.

In case of premium discontinuance after 5 policy years, you can revive the policy within three years from the date of the first unpaid premium. On revival, applicable premium allocation charges will be levied and the policy will continue with the risk cover, benefits, and charges, as per the terms and conditions of the policy. You shall have an option to revive the policy without or with the rider if any

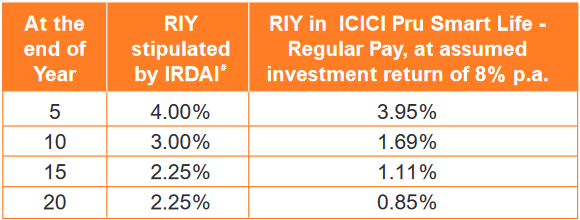

What is the benefit of staying invested for the long term?

- Lower Reduction in Yield –

The longer you stay invested in this policy the better can be the expected returns. The table below shows the Reduction in Yield (RIY) at 8% and 4% investment return for the example mentioned above. The lower the RIY, the better it is for you.

The RIY has been calculated after applying all the charges (except service tax, applicable cesses and mortality charges) and an annual premium of Rs 50,000 p.a.

Various Types of charges under the policy –

a) Premium Allocation Charge –

Premium Allocation Charge depends on the premium payment option and the premium payment mode chosen. It is deducted from the premium amount at the time of premium payment and units are allocated in the chosen funds thereafter. This charge is expressed as a percentage of the premium.

- One Pay – 3% A discount of 0.5% in the premium allocation charge is given to customers who buy directly from the Company’s website.

- Limited/Regular Pay –

A discount of 1% in the premium allocation charge in Year 1 is given to customers who buy directly from the Company’s website. All Top-up premiums are subject to an allocation charge of 2%.

b) Policy Administration Charge –

The policy administration charge will be levied every month by the redemption of units, subject to a maximum of Rs 500 per month (Rs 6,000 p.a.). The policy administration charge will be as set out below –

- One Pay – Rs 60 p.m. (Rs 720 p.a.) for the first five policy years

- Limited/Regular Pay – 0.21% p.m. (2.52% p.a.) of Annual Premium, for the entire policy term.

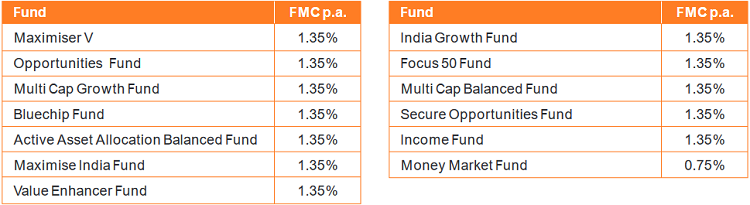

c) Fund Management Charge (FMC) –

The following fund management charges will be applicable and will be adjusted from the NAV on a daily basis. This charge will be a percentage of the Fund Value.

Can I cancel the policy if I didn’t like its terms and conditions?

Yes, the policyholder can cancel the policy if not satisfied with the terms and conditions of this policy. The policy can be returned to the company, with the Policy Document and reasons for cancellation within 15 days and 30 days (if the policy is purchased through distance marketing) from the date you receive your policy. This period is known as the Free Look Period.

On cancellation of the policy during the free-look period, you shall be entitled to an amount which shall be equal to non-allocated premium plus charges levied by cancellation of units plus Fund Value at the date of cancellation less stamp duty expenses paid under the policy and expenses borne by the Company on medical examination, if any. Thereafter this policy shall terminate and all rights, benefits, and interests under this policy shall be extinguished.

Which portfolio strategy suits me the best?

- Fixed Portfolio Strategy – With this option, you can invest your money in equity and debt funds of your choice. You can also move your money from one fund to another to suit your investment needs.

- Lifecycle-based Portfolio Strategy – With this option, your money is automatically allocated to equity and debt funds based on your age. As you grow older, your money is systematically transferred from equity to debt to secure it when the policy matures.

How much money will my family receive in my absence?

In case of the unfortunate demise of the person insured, the company pays in two ways, as follows –

i) Lump-Sum Benefit – A lump sum benefit is paid out by the company to take care of any immediate liabilities of the family.

The Lump Sum benefit is the higher of the two amounts –

- A fixed amount called the Sum Assured, including Top-up Sum Assured if any

- Minimum Life Cover that is equal to 105% of the total premiums including Top-up premiums, if any received up to the date of death.

ii) Smart Benefit – This benefit ensures that your savings continue to grow to fulfill your family’s goals. In case of an unfortunate event, the company pays the future premiums on your behalf and the policy continues uninterrupted.

How does Smart Benefit work?

The company pays the premium in the form of units on the due date. On maturity of the policy, the nominee receives a lump sum of the Fund Value including the Top-up Fund Value, if any.

Smart Benefit is valid for regular premium policies and applies only if all due premiums have been paid.

What is the value of Wealth Boosters that I will get?

Each Wealth Booster addition will be equal to 3.25% of the Fund Value average in the Regular and Limited Pay options and 1.5% in One Pay option. This will also include additional Fund Value from Top-ups if any. The additions are made once in 5 years starting from the end of the 10th policy year, which means for a policy term of 25 years, Wealth Boosters will be allocated four times.

Loyalty Additions and Wealth Boosters will be equal to the above percentage of the average Fund Values on the last business day of the last eight policy quarters.

Is Wealth Booster a guaranteed feature of the product?

Yes, the allocation of Wealth Booster units is guaranteed and is subject to regular payment of premiums.

How much money can I withdraw?

You can withdraw up to 20% of your Fund Value at any time from the sixth policy year.

Exclusion under the Policy –

- Suicide Clause

If the Life Assured, whether sane or insane, commits suicide within 12months from the date of commencement of the policy or from the date of policy revival, only the Fund Value, including Top-up Fund Value, if any, as available on the date of intimation of death, would be payable to the nominee.

Any charges other than Fund Management Charges and guarantee charges, if any, recovered subsequent to the date of death shall be added back to the fund value as available on the date of intimation of death.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.