The success of any business totally depends upon a good workforce in the company. Everyone requires some sort of insurance in life, especially when their family is totally financially dependent on them. The HDFC Life Group Term Insurance (GTI) plan meets this need and serves as an ideal way for companies to reinforce their bond with their employees.

The sort of needs an employer need to cater to its employees could be in the form of the following –

- Employee benefits

- Cover for housing or vehicle loans given by the employer to the employee.

- A Group Term Insurance cover for future service gratuity liability

Features of this policy –

- This policy provides life cover to groups of people.

- It is a master policy covering all members of the group.

- The term insurance plan can be renewed annually.

- The company can add and delete the member’s names anytime during the year.

- Sum assured will be payable to the nominee on the death of the covered member (death covered can be either natural or accidental).

- Employees can be additionally covered by riders e.g. accidental/ critical illness/disability.

- This policy offers flexibility to cover the spouse of the member.

- This policy comes with an easy claim settlement process enabling speedy & quick settlement.

- One can take additional protection by opting for HDFC Life Group Critical Illness + Rider that provides rider Sum Assured in case diagnosed with any of the 19 Critical Illnesses.

- No limit on maximum sum assured.

- The policy covers death due to any cause; accidental or natural, and hence it is more comprehensive than Group Personal Accident insurance.

Benefits of the policy –

A) Benefits to the employer –

- Life cover for all the group members under one policy.

- Easy and hassle-free financial help to the employee’s family, in case of an unfortunate incidence.

- Group Term Insurance are cost-effective policies for employers because they can buy a high cover at a low premium.

- This policy can serve as a strong retention tool.

- Premiums paid by the employer are tax deductible u/s 37 (1) of the Income Tax Act, 1961.

- Simple procedures for the addition and deletion of members into the policy.

B) Benefits to the employee –

- Adequate financial support to the family members against the accident, illness or untimely death of the policyholder.

- No medical test required until free cover limits.

- Employer gives cover for housing or vehicle loans to the employees.

- Premiums paid by the employer is not treated as perquisite in the hands of employees.

- Death benefit is exempted from tax under Section 10(10D) of Income Tax Act, 1961.

C) Death Benefit –

If the member of this policy passes away then sum assured will be payable to the nominee, provided the policy is active.

D) Maturity Benefit –

There is no maturity benefit payable under any circumstances.

E) Surrender Benefit –

If the policyholder surrenders the policy before completion of the term, then an amount equal to the premium for the unexpired term of the discontinuing members minus an appropriate deduction for expenses, commission and taxes and levies as applicable would be payable. In case of such surrenders, the individual members of the group will be given an option to continue the policy as an individual policy until the expiry of the term of the group policy

F) Optional Rider Benefits –

If a policyholder wants some additional rider benefits, then the policyholder will have to pay some additional cost other than the policy premium. Below table shows the type of rider benefit available to the policyholder –

| Accidental Death Benefit | Total Permanent Disability | Total Permanent and Partial Disability | HDFC Life Group Critical Illness Plus Rider |

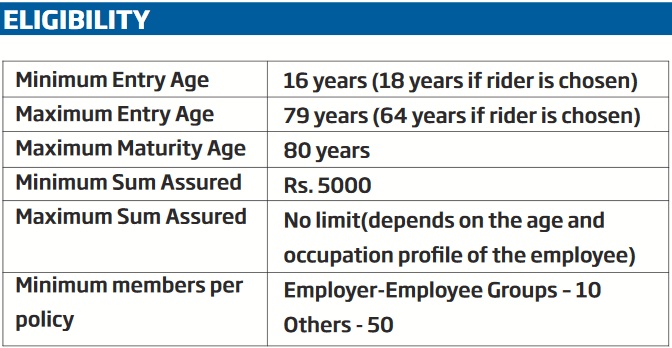

Eligibility of the policy –

Like other policies of HDFC, this policy also has some eligibility conditions. Let’s have a look at them –

Tax Benefits –

- Premium paid by the company will be considered a tax-deductible expense for the company under Section 37 (1) of the Income Tax Act, 1961. Premium paid by the company is not taxable as a perquisite in the hands of the employees.

- Tax benefits described in Section 80C and Section 80D (for Critical Illness Benefit payments by Cheque) are applicable to the premiums paid by the employee.

- Any proceeds from a claim on this plan, which accrue to the employee or his beneficiaries, are exempted from tax under Section 10(10D).

Exclusions in the policy –

- Exclusions On Basic Death Benefit – In case of employer – Employee Schemes – Sum Assured will be payable to the nominee in case of death due to suicide. In case of other schemes, if the member dies due to suicide within 12 months from the date of joining the scheme, the nominee shall be entitled to get 80% of the premiums paid.

Conclusion –

So, by now you know each and every important details of this policy. Do let me know if I have missed any important point in the comment section. Please feel free to ask any doubts regarding this policy.