HDFC Life Click 2 Protect 3D Plus is a term insurance plan that offers comprehensive security at an affordable price. One can buy this plan online through the website of HDFC. 3D stands for the three uncertainties that each one of us faces at some given point in life. One cannot get rid of these 3 uncertainties of life. This 3D is Death, Disability and Disease.

Features of this policy –

- Provide financial protection to you and your family at an affordable cost.

- One can choose to customize the term plan with a choice of 9 plan options.

- All future premiums are waived on Accidental Total Permanent Disability (available under all options) and on diagnosis of Critical Illness (available under 3D Life & 3D Life Long Protection options).

- One can protect their whole life with Life Long Protection & 3D Life Long Protection options.

- The policyholder has the flexibility to choose the policy with premium payment terms.

- Life Stage Protection feature offers to increase insurance cover on certain key milestones without medicals.

- There are special premium rates for female policyholders as well as attractive premium rates for non-tobacco users.

- Offers a 30 day free look period.

- Tax Benefits on the premiums and the pay-outs under Section 80C and 10(10D) of Income Tax Act.

Benefits of the policy –

- Terminal Illness Benefit – In this case, the payment of Death Benefit will be accelerated and the policy will terminate. This benefit is available under all 9 plan options.

- Critical Illness Benefit – In this case, all future premiums payable under the plan will be waived, if the policyholder is diagnosed with any of the covered critical illnesses. This benefit is available under only 3D Life & 3D Life Long Protection options.

- Benefit on Accidental & Total Permanent Disability (ATPD) – In this option, all future premiums payable under the plan will be waived on ATPD. This benefit is available under all plan options.

- Accidental Death Benefit – In this case, an Extra Life Sum Assured is paid along with the death benefit upon the death of policyholder due to accident. This benefit is available under only Extra Life & Extra Life income options.

- Maturity Benefit – In this case, all the premiums paid to date are returned back to the policyholder upon survival till the end of the policy term. This benefit is available under only the Return of Premium option.

- Death Benefit – Death Benefit is the sum of – a) Sum Assured on Death and (b) Additional Benefits

Sum Assured on Death is defined as:

i) For Single Pay Policies –

Highest of –

- 125% of Single Premium

- “Guaranteed Sum Assured on Maturity”

- Absolute amount assured” to be paid on death

ii) For Regular Pay & Limited Pay Policies –

Highest of –

- 10 times of the Annualized Premium

- 105% of Total Premiums Paid

- “Guaranteed Sum Assured on Maturity”

- “Absolute amount assured” to be paid on death

- Life Stage Protection – Under this feature, the policyholder has an option to increase the basic Sum Assured without underwriting on any of the below-specified events in the life of the policyholder –

- 1st Marriage – 50% of Sum Assured subject to a maximum of Rs. 50 lakhs

- Birth of 1st child – 25% of Sum Assured subject to a maximum of Rs. 25 lakhs

- Birth of 2nd child – 25% of Sum Assured subject to a maximum of Rs. 25 lakhs. This option is available for all plan options and is subject to BAUP.

- Top Up option – In the Top-up Option, the policyholder may opt for a systematic increase of the policy cover from 1st policy anniversary onwards. The Top-up option is available for all the plan options under Click 2 Protect 3D Plus. And the policy has opted at policy inception and is subject to BAUP.

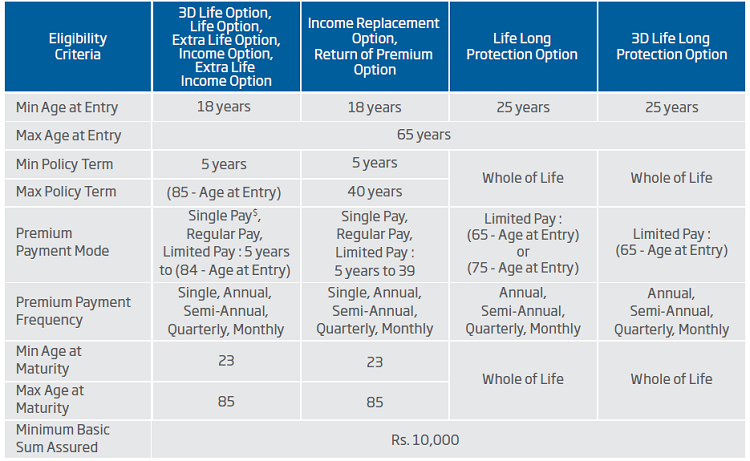

Eligibility conditions of the policy –

Like other policies of HDFC, this policy also has some eligibility conditions. Let’s have a look at these conditions –

9 Options available under this plan –

The 9 options are as follows –

Depending on the 2 types of pay-outs, Lump-sum and Lump-sum + Monthly pay-outs, the 9 optional plans are divided as mentioned below:

LUMP-SUM PAYOUTS –

The Nominee will get the entire amount at one go as Death Benefit in case of lump-sum pay-outs.

A) Life Option :

In life option, if the policyholder dies during the policy term or the policyholder is diagnosed with any of the mentioned Terminal Illness, then the nominee receives the death benefit. The entire sum assured is paid at one go by HDFC Life Insurance. In the future, if the policyholder suffers a total permanent disability due to an accident, then all future premiums will be waived off.

B) Extra Life Option :

In Extra Life Option, along with immediate pay-out (Sum Assured on death or diagnosis of Terminal illness) and waiver of premium (in case of total permanent disability due to an accident an additional accidental death rider is attached. If the policyholder becomes a victim of accidental death, then the nominee will receive an additional benefit over and above the base policy coverage.

C) 3D Life Option :

The term 3D stands for Death, Disease, and Disability. This term plan covers all three D – Death, Disease, and Disability. In case of death or diagnosis of any Terminal Illness (covered), the lump-sum benefit is paid. And in case of total permanent disability due to an accident or diagnosis of any of the 34 mentioned Critical Illness, there is a waiver of future premiums.

D) Life-Long Protection Option :

As the name suggests, a lifelong protection option means protecting the policyholder’s life until the policyholder is alive. However, the policyholder pays premiums only till the age of 65 years. In case, the policyholder passes away or is diagnosed with any of the mentioned Terminal Illness, the entire sum assured paid is in lump-sum. In case the life assured suffers a total and permanent accidental disability, all future premiums are waived off.

E) 3D Life Long Protection Option :

In addition to the benefits under Life Long Protection Option, the policyholder will receive an additional benefit of waiver of future premiums upon diagnosis of Critical Illness. The policyholder pays the premium only till the age of 65 yrs.

F) Return of Premium Option :

Under this plan option, your total premiums 22 will be returned if the policyholder survives until the end of the Policy Term. On death/ diagnosis of Terminal Illness during the Policy Term, a Lump-sum benefit will be paid to the nominee and all future premiums are waived off in case of total permanent accidental disability.

LUMP-SUM + MONTHLY PAYOUTS –

G) Income Option :

In Income Option, the policyholder can choose the term for the monthly income to be received by the nominee (to ensure the financial stability of the family). The policyholder can also either level or increase the monthly income depending on the requirement. Along with this, a lump-sum benefit on death or diagnosis of Terminal Illness is paid and all future premiums are waived off in case of total permanent accidental disability.

H) Extra Life Income Option :

This plan comes with an in-built accidental death benefit rider. An addition to the income option, an extra benefit of an additional Sum assured will be paid out on accidental death partly as Lump-sum and partly as income.

I) Income Replacement Option :

Income Replacement Option ensures that the nominee keeps receiving the income stream even in the policyholder’s absence. In case of death or diagnosis of Terminal Illness, the nominee will receive 12 times the applicable monthly income as lump-sum as well as a level/increasing income for residual policy term. Apart from this, all future premiums will be waived off in case of total permanent accidental disability.

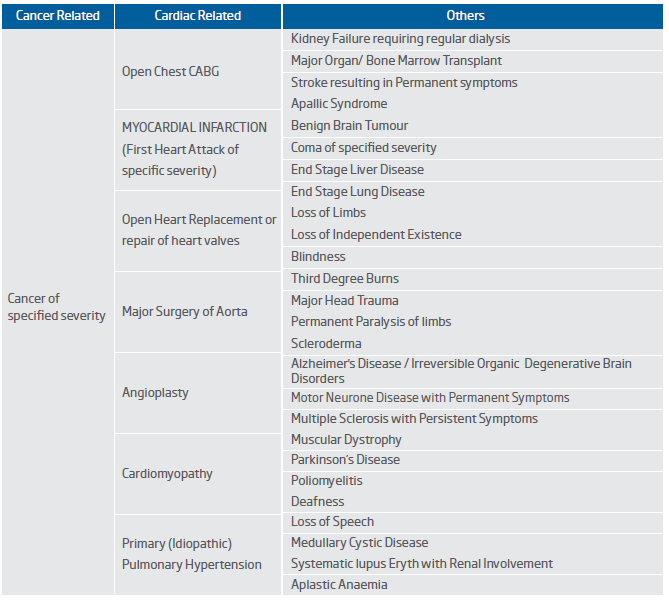

List of Critical Illness covered under this policy –

Here is the list of critical illnesses of this policy. Let’s have a look at what all is covered under the policy. For a detailed description of the critical illnesses, one can refer to the policy documents –

If I don’t pay premiums then what?

If a policyholder doesn’t pay premiums then Grace Period comes into the picture. The grace period is the time provided after the premium due date during which the policy is considered to be in-force with the risk cover. This policy has a grace period of 30 days for yearly, half-yearly and quarterly frequencies from the premium due date. The grace period for monthly frequency is 15 days from the premium due date.

If a valid claim arises under the policy during the grace period, but before the payment of due premium, then the company shall still take the claim. In such cases, the due and unpaid premium will be deducted from any benefit payable. In case if the policyholder does not pay premiums before the end of the grace period, then the policy will lapse. All risk cover will cease and no benefits will be payable in case of lapsed policies.

what is not covered under this policy?

A) Suicide Clause of the policy –

- If the policyholder commits suicide, within 12 months from the date of inception of the policy, then the nominee of the policy will be entitled to at least 80% of the premiums paid, provided the policy is in force.

- If the policyholder commits suicide, from the date of revival of the policy, then the nominee of the policy will be entitled to an amount which is higher of 80% of the premiums paid till the date of death or the surrender value as available on the date of death.

B) Additional Exclusions under Extra Life and Extra Life Income Options –

The company is not liable to pay an accidental death benefit in 2 cases if the death occurs after 180 days from the date of the accident and also if accidental death is caused directly or indirectly by any of the following –

- If death occurs after 180 days from the date of the accident.

- Intentionally self-inflicted injury or suicide, irrespective of mental condition.

- Alcohol or solvent abuse, or the taking of drugs except under the direction of a registered medical practitioner

- War, invasion, hostilities (whether war is declared or not), civil war, rebellion, revolution or taking part in a riot or civil commotion.

- Taking part in any flying activity, other than as a passenger in a commercially licensed aircraft.

- Taking part in any act of a criminal nature with criminal intent.

- Taking part or practicing for any hazardous hobby, pursuit or race unless previously agreed to by us in writing.

C) Additional Exclusions under 3D Life and 3D Life Long Protection options –

The company will not be liable to pay any benefit if the critical illness is caused directly or indirectly by the following:

- Any of the listed critical illness conditions where death occurs within 30 days of the diagnosis.

- Any sickness-related condition manifesting itself within 90 days of the commencement of the policy/date of acceptance of risk or reinstatement of cover.

- Intentionally self-inflicted injury or attempted suicide, irrespective of mental condition.

- Taking part in any act of a criminal nature with criminal intent.

- HIV or AIDS

- Failure to seek medical or follow medical advice (as recommended by a Medical Practitioner).

- Radioactive contamination due to nuclear accident.

- Alcohol or solvent abuse, or voluntarily taking or using any drug, medication or sedative unless it is an “over the counter” drug, medication or sedative taken according to package directions or as prescribed by a Medical Practitioner.

Is it possible to revive a lapsed policy?

Yes, a lapsed policy can be revived within 2 consecutive years of lapsation subject to the terms and conditions specified by the company from time to time. In case the policy is revived, the policyholder is entitled to receive all contractual benefits.

Can I get loans against this policy?

Loans against this policy are not allowed to any policyholder.

Can I cancel the policy if I didn’t like its terms and conditions?

Yes, the policyholder can cancel the policy if the policyholder doesn’t like its terms and conditions. The policy can be returned within 15 days from the date of receipt of the policy stating a reason to the company as to why the policyholder wants to cancel the policy. This period is called Free-Look Period.

Free-Look Period for policies purchased through online/ distance marketing will be 30 days. Distance Marketing refers to insurance policies sold over the telephone or the internet or any other method that does not involve face-to-face selling. Once the policy is canceled, the company is entitled to refund the premium, after deducting –

- The proportionate risk premium for the period on cover,

- The expenses incurred by the company on medical examination if any

- stamp duty

Distance Marketing refers to insurance policies sold over the telephone or the internet or any other method that does not involve face-to-face selling.

Can I surrender the policy?

Every policy is entitled to surrender value during the policy term, provided no claims have been made under the policy. Surrender Value gets acquired immediately on payment of a single premium. For Limited and Regular Payment policies, Surrender Value gets acquired upon payment of premiums for 2 years – in case of premium payment term is less than 10. For other cases, surrender value gets acquired on payment of premiums for 3 years

All surrender values are guaranteed. To know the Special Surrender Values one can refer to the policy documents.

Video Review of the policy –

Conclusion –

So, by now all of you know each and every detail of this policy. Now it’s up to you all to decide whether this policy will be best for you or not. If you have any doubt regarding this policy, they please let us know in the comment section.