We always wonder about an investment vehicle that can provide protection to the family as well as earn good returns. We basically want to have such an insurance plan which helps us realize our dreams without any worry. Aditya Birla Sun Life insurance has come with a policy that will maximize your wealth and as well as give protection to your and your family. “ABSLI Wealth Max Plan” is a single premium unit-linked insurance policy.

Features of this Policy –

- Pay once and reap the benefits of financial growth

- No Policy Loan is allowed against this policy

- The Flexibility to add top-ups whenever you have additional savings

- The flexibility of partial withdrawals to meet any emergency fund requirements

- Tax benefits under Section 80C and Section 10(10D) of the Income Tax Act, 1961(1)

Investment Options under this Policy –

Under ABSLI Wealth Max Plan, one can decide how to invest your basic and top-up premiums in one of the two investment options –

- Systematic Transfer Option or

- Self-Managed Option

The policyholder has an option to change investment options at any time after one year while the policy is in effect.

a) Systematic Transfer Option –

The Systematic Transfer Option safeguards your wealth against the market volatilities. Under the Systematic Transfer Option, your premium (net of premium allocation charge) shall be first allocated to the Liquid Plus fund option and thereafter monthly 1/12th of the allocated amount shall be transferred to a segregated fund of your choice.

You may choose any one segregated fund out of Income Advantage, Enhancer, Creator, Maximiser, Multiplier, Super 20, Value & Momentum, and MNC Capped Niy Index and Asset Allocation for your premiums to be transferred to.

The transfers to your chosen segregated fund will take place monthly on 1st, 8th, 15th or 22nd of the month as selected by you. Any top-up premiums paid are invested directly in the target fund.

For example – If person A aged 35 years, opts for Systematic Transfer Option with transfers on 15th of eve month to Super 20:Premium/s net of premium allocation charges will be allocated in Liquid Plus Fund and thereafter on 15th of eve month, 1/12th of initially allocated amount shall be automatically transferred to Super 20 Fund.

b) Self- Managed Option –

The Self Managed Option gives you access to our well-established suite of 16 segregated funds, complete control in how to invest your premium and full freedom to switch from one segregated fund to another.

Our 16 segregated funds range from 100% debt to 100% equity to suit your particular needs and risk appetite –

- Liquid Plus,

- Income Advantage,

- Assure,

- Protector,

- Builder,

- Enhancer,

- Creator,

- Magnifier,

- Maximiser,

- Multiplier,

- Super 20,

- Pure Equity,

- Value & Momentum,

- Capped Nifty Index,

- Asset Allocation and

- MNC

If one wishes to diversify their risk, you can choose to allocate your premiums in varying proportions amongst the 16 segregated funds. To meet your everchanging investment needs, you have full flexibility to switch money from one segregated fund to another at any time provided the switched amount is for at least Rs 5,000.

You can change from one investment option to another investment option anytime after the first policy year. You can switch to Self-Managed Option or Systematic Transfer Option during the policy term. Switching to Systematic Transfer Option is allowed only at the policy anniversary.

A detailed description of Segregated Fund’s –

1) Liquid Plus –

- Objective – To provide superior risk-adjusted returns with low volatility at a high level of safety and liquidity through investments in high-quality short term fixed income instruments – up to one-year maturity.

- Strategy – Fund will invest in high quality short-term fixed income instruments – up to one-year maturity. The endeavor will be to optimize returns while providing liquidity and safety with a very low-risk profile.

2) Income Advantage –

- Objective – To provide capital preservation and regular income, at a high level of safety over a medium-term horizon by investing in high-quality debt instruments.

- Strategy – To actively manage the fund by building a portfolio of fixed income instruments with medium-term duration. The fund will invest in government securities, high rated corporate bonds, high-quality money market instruments, and other fixed-income securities. The quality of the assets purchased would aim to minimize the credit risk and liquidity risk of the portfolio. The fund will maintain a reasonable level of liquidity.

3) Assure –

- Objective – To provide capital conservation, at a high level of safety and liquidity through judicious investments in high-quality short-term debt.

- Strategy – To generate better return with a low level of risk through investment into fixed interest securities having short-term maturity profiles.

4) Protector –

- Objective – To generate consistent returns through active management of a fixed income portfolio and focus on creating a long-term equity portfolio, which will enhance the yield of the composite portfolio with minimum risk appetite.

- Strategy – To invest in fixed income securities with marginal exposure to equity up to 10% at a low level of risk. This segregated fund is suitable for those who want to preserve their capital and earn a steady return on investment through higher exposure to debt securities.

5) Builder –

- Objective – To build capital and generate better returns at a moderate level of risk, over a medium or long-term period through a balance of investment in equity and debt.

- Strategy – To generate better returns with a moderate level of risk through active management of a fixed income portfolio and focus on creating a long-term equity portfolio, which will enhance the yield of the composite portfolio with a low level of risk appetite.

6) Enhancer –

- Objective – To grow capital through enhanced returns over a medium to long-term period through investments in equity and debt instruments, thereby providing a good balance between risk and return. It is suitable for individuals seeking, higher returns with a balanced equity-debt exposure.

- Strategy – To earn capital appreciation by maintaining a diversified equity portfolio and seek to earn regular returns on the fixed income portfolio by active management resulting in wealth creation for policyholders.

7) Creator –

- Objective – To achieve the optimum balance between growth and stability to provide long-term capital appreciation with a balanced level of risk by investing in fixed income securities and high-quality equity security. This fund option is for those who are willing to take the average to a high level of risk to earn attractive returns over a long period of time.

- Strategy – To invest in fixed income securities & maintaining a diversified equity portfolio along with active fund management of the policyholder’s wealth in the long run.

8) Magnifier –

- Objective – To maximize wealth by managing a diversified portfolio.

- Strategy – To invest in high-quality equity security to provide long-term capital appreciation with a high level of risk. This fund option is suitable for those who want to have wealth maximization over a long-term period with equity market dynamics.

9) Maximiser –

- Objective – To provide long term capital appreciation by actively managing a well-diversified equity portfolio of fundamentally strong blue-chip companies. Further, the fund seeks to provide a cushion against the sudden volatility in the equities through some investments in short-term money market instruments.

- Strategy – To build and actively manage a well-diversified equity portfolio of value and growth driven stocks by following a research-focused investment approach. While appreciating the high risk associated with equities, the fund would attempt to maximize the risk-return pay off for the long-term advantage of the policyholders. The fund will also explore the option of having exposure to quality mid-cap stocks.

The non-equity portion of the fund will be invested in good rated (P1/A1 & above) money market instruments and fixed deposits. The fund will also maintain a reasonable level of liquidity.

10) Multiplier –

- Objective – To provide long-term wealth maximization by actively managing a well-diversified equity portfolio, predominantly comprising of companies whose market capitalization is close to `1000 crores and above.

- Strategy – To build and actively manage a well-diversified equity portfolio of value & growth driven stocks by following a research-driven investment approach. The investments would be predominantly made in mid-cap stocks, with an option to invest 30% in large-cap stocks as well. While appreciating the high risk associated with equities, the fund would attempt to maximize the risk-return pay-off for the long-term advantage of the policyholders. The fund will also maintain a reasonable level of liquidity.

11) Super 20 –

- Objective – To generate long-term capital appreciation for policyholders by making investments in fundamentally strong and liquid large-cap companies.

- Strategy – To build and actively manage an equity portfolio of 20 fundamentally strong large-cap stocks in terms of market capitalization by following an in-depth research-focused investment approach. The fund will attempt to adequately diversify across sectors. The fund will invest in companies having financial strength, robust, efficient & visionary management, enjoying competitive advantage along with good growth prospects & adequate market liquidity.

The fund will adopt a disciplined yet flexible long-term approach towards investing with a focus on generating long-term capital appreciation. The non-equity portion of the fund will be invested in highly-rated money market instruments and fixed deposits. The fund will also maintain a reasonable level of liquidity.

12) Pure Equity –

- Objective – To provide long-term wealth creation by actively managing the portfolio through investment in selective businesses. Fund will not invest in businesses that provide goods or services in gambling, lotte /contests, animal produce, liquor, tobacco, entertainment like films or hotels, banks, and financial institutions.

- Strategy – To build and actively manage a well-diversified equity portfolio of value & growth driven fundamentally strong companies by following a research-focused investment approach. Equity investments in companies will be made in strict compliance with the objective of the fund. The fund will not invest in banks and financial institutions and companies whose interest income exceeds 3% of total revenues.

Investment in leveraged-firms is restrained on the provision that heavily indebted companies ought to serve a considerable amount of their revenue in interest payments.

13) Value & Momentum –

- Objective – To provide long-term wealth maximization by managing a well-diversified equity portfolio predominantly comprising of deep value stocks with strong price and earnings momentum.

- Strategy – To build & manage a well-diversified equity portfolio of value and momentum-driven stocks by following a prudent mix of qualitative & quantitative investment factors. This strategy has outperformed the broader market indices over the long-term. The fund would seek to identify companies, which have attractive business fundamentals, competent management and prospects of robust future growth and are yet available at a discount to their intrinsic value and display good momentum. The fund will also maintain a reasonable level of liquidity.

14) Capped Nifty Index –

- Objective – To provide capital appreciation by investing in a portfolio of equity shares that form part of a Capped NIFTY Index.

- Strategy – To invest in all the equity shares that form part of the Capped Nifty in the same proportion as the Capped Nifty. The Capped Niy Index will have all 50 companies that form part of the Nifty index and will be rebalanced on a quarterly basis. The index composition will change with eve change in the price of Niy constituents. Rebalancing to meet the capping requirements will be done on a quarterly basis.

15) Asset Allocation –

- Objective – To provide capital appreciation by investing in a suitable mix of cash, debt, and equities. The investment strategy will involve a flexible policy for allocating assets among equities, bonds, and cash.

- Strategy – To appropriately allocate money between equity, debt and money market instruments, to take advantage of the movement of asset prices resulting from changing financial and economic conditions.

16) MNC –

- Objective – To provide capital appreciation by investing in equity and equity-related instruments of multi-national companies.

- Strategy – The fund will predominantly invest in companies where FII / FDI and MNC parent combined holding is more than 50%. This theme has outperformed the broader market indices over the long-term. The companies chosen are likely to have above-average growth, enjoy distinct competitive advantages, and have superior financial strengths. The fund will also invest in high-quality money market instruments and maintain adequate liquidity.

Benefits of this Policy –

a) Death Benefit –

In the unfortunate event the life insured dies while the policy is in effect, the company will pay to the nominee the higher of –

- Basic Fund Value as on date of intimation of death; or

- Basic Sum Assured

In addition, the company will also pay the higher of the following –

- Top-up Fund Value as on date of intimation of death; or

- Top-up Sum Assured

At all times, if the policy has not been discontinued, the Death benefit shall never be less than 105% of basic premiums plus top-up premiums paid up to the date of death.

b) Maturity Benefit –

the insured will receive the Basic Fund Value plus the Top-Up Fund Value as of that date at the end of the Policy Term.

c) Surrender Benefit –

At any time while your policy is in effect the insured can request to surrender this policy for its Surrender Benefit. The Surrender Benefit –

- During the first 5 policy years shall be as explained in the Policy Discontinuance provisions

- After 5 policy years shall be the Policy Fund Value as of that date

d) Guaranteed Benefits –

This will be added to your policy in the form of additional units.

- From the 6th to 10th policy anniversary – Guaranteed Addition is 0.25% of the average Policy Fund Value in the last 12 months.

- From the 11th policy anniversary and every year thereafter – Guaranteed Addition is 0.60% of the average Policy Fund Value in the last 12 months.

e) Rider Benefit –

ABSLI Accidental Death Benefit Rider Plus – In the unfortunate event of the death of the life insured due to an accident within 180 days of the occurrence of the accident, the company will pay 100% of the rider sum assured to the nominee.

Also, the company will refund the premiums collected after the date of Accident till the date of death, with interest as declared by the company from time to time, along with death benefit payable.

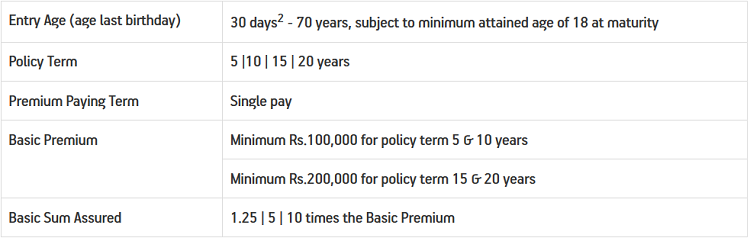

Eligibility Criteria of the policy –

Are there any Policy Charges in the Policy?

a) Premium Allocation Charge –

- A premium allocation charge of 3% is levied on the basic premium when received.

- A premium allocation charge of 2% is levied on any top-up premium when paid.

b) Fund Management Charge –

The daily unit price of the segregated fund is adjusted to reflect the fund management charge –

- 1.00% p.a. for Liquid Plus, Income Advantage, Assure, Protector and Builder

- 1.25% p.a. for Enhancer, Creator, Capped Niy Index, and Asset Allocation

- 1.35% p.a. for MNC, Magnifier, Maximiser, Multiplier, Super 20, Pure Equity and Value & Momentum.

The company may change the fund management charge under any segregated fund at any time in the future subject to a maximum of 1.35% p.a. in the future subject to IRDAI approval.

c) Policy Administration Charge –

The policy administration charge is Rs 20 per month for the first five policy years. It shall increase to Rs 25 per month in the sixth year and inflate at 5% p.a. thereafterer, subject to a maximum of Rs 6,000 p.a. This charge is deducted at the start of eve month by canceling units proportionately from each segregated fund you have at that time.

d) Mortality Charge –

Mortality Charge is deducted at the start of every month for providing you with the risk cover. It is charged by canceling units proportionately from each segregated fund you have at that time. The charge per 1000 of Sum at Risk will depend on the gender and attained the age of the life insured.

e) Miscellaneous Charges –

The company currently charges Rs 50 per request for a change in investment option, fund switch, partial withdrawal or any additional servicing request. The company, however, reserve the right to charge up to Rs 500 per request in the future. Any increase in the miscellaneous charges will be subject to IRDAI approval.

Is there any partial withdrawal allowed in the policy?

Yes, the insured is allowed to make unlimited partial withdrawals any time after –

- Five complete policy years or

- Life insured attaining the age of 18 whichever is later.

The partial withdrawals shall first be adjusted from Top-up Fund Value (except any top-up premiums paid in the previous five years immediately preceding the date of withdrawal); if any. Once the Top-up Fund Value is exhausted, partial withdrawals would be adjusted from Basic Fund Value.

The top-up sum assured will remain unchanged after any withdrawal from the top-up fund value. The minimum amount of partial withdrawal is Rs 5,000. There is no maximum limit, but you are required to maintain a minimum Policy Fund Value of 50% of the basic premium paid plus 100% of any top-up premiums paid in the previous five years immediately preceding the date of withdrawal.

Is it possible to return the policy if I didn’t like its terms and conditions?

Yes, the policy can be returned within 15 days (30 days in case the policy issued on Distance Marketing) from the date of receipt of the policy, in case you are not satisfied with the terms & conditions of your policy. This 15-day period is called the Free Look Period.

The company will pay the policy fund value + non allocated premiums + charges levied by cancellation of units once we receive your written notice of cancellation (along with reasons thereof) together with the original policy documents.

Exclusion under the Policy –

Suicide Exclusion –

If the policyholder dies due to suicide within 12 months from the date of commencement of the policy, the nominee or the beneficiary of the policyholder shall be entitled to the Policy fund value, as available on the date of intimation of death.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.