Aditya Birla Sun Life Insurance Wealth Assure Plus enables your wealth to grow over the long-term while protecting it against death, Critical Illness, or Total Permanent Disability. With the benefits of MNC fund in your portfolio, it helps in generating good returns. Also, you get up to 2.4 times in the form of guaranteed additions. Thus, this plan provides a secure financial future to achieve your life goals at different stages.

Features of this Policy –

- A plan that offers the dual benefit of life insurance protection and savings through a wide range of fund options.

- Option to increase protection through a waiver of premium in case of Critical Illness or Total Permanent Disability

- The flexibility to choose from 2 plan options to suit your aspirations

- Boost your savings through regular premiums

- The flexibility to choose between 4 investment options to suit your needs

- The flexibility to add top-ups whenever you have additional savings

- The flexibility of partial withdrawals to meet any emergency fund requirements

Plan Options of the Policy –

The Insured can choose between the 2 plan options at inception. The benefit to be paid to the nominee/policyholder in case of unfortunate death of the life insured during the policy term.

- Classic Option – Sum Assured plus Policy Fund Value.

- Assured Option – Sum Assured plus Policy Fund Value. Additionally, on the occurrence of any Critical Illness or Total Permanent Disability, the policy will continue till maturity and all the future installment premiums shall be paid by us on the premium due dates in the fund value.

Investment Options of the Policy –

i) Smart Investment Option –

- Portfolio structured as per your maturity date and risk profile.

- Basic Premium invested under two segregated funds – Maximiser (Equity) and Income Advantage (Debt)

- ABSLI will manage & administer the investments on your behalf

- Allocation turns conservative as the maturity date approaches to protect accumulation.

- The proportion invested in Maximiser will be according to the schedule given below – the remaining amount will be invested in Income Advantage.

ii) Systematic Transfer Investment Option –

- Available only if you have opted for Annual Mode.

- The basic premium shall be first allocated to the Liquid Plus fund option.

- Thereafter Monthly 1/12th or Weekly 1/48th of the allocated amount shall be transferred to up to 4 segregated fund(s) of your choice viz. Income Advantage, Enhancer, Creator, Maximiser, Multiplier, Super 20, Value & Momentum, and new MNC as per the investment proportion for the chosen funds.

- Transfers to your chosen segregated fund(s) will take place monthly on 1st, 8th, 15th or 22nd of the month

Switch between monthly and weekly transfers can be done on the policy anniversary.

iii) Self Managed Investment Option –

- Gives you access to our well-established suite of 16 segregated funds – Liquid Plus, Income Advantage, Assure, Protector, Builder, Enhancer, Creator, Magnifier, Maximiser, Multiplier, Super 20, Pure Equity, Value & Momentum, Capped Nifty Index, Asset Allocation, MNC.

- It gives you complete control over how to invest your premiums.

- Full freedom to switch from one segregated fund to another.

- Flexibility to redirect future premiums by changing your premium allocation percentages at any time.

iv) Return Optimizer Investment Option –

- Basic premiums (net of allocation charges) are invested in the Maximiser fund.

- It will be tracked every day for each policyholder for a pre-determined upside movement of 10% or more over the net invested amount (net of all charges).

- When the gain from the Maximiser fund reaches 10% or more of the net invested amount, the amount equal to the appreciation will be transferred to the Income Advantage fund at the prevailing unit price.

- Protect your gains from the future market volatility and create a more stable sequencing of investment returns.

Benefits of the Policy –

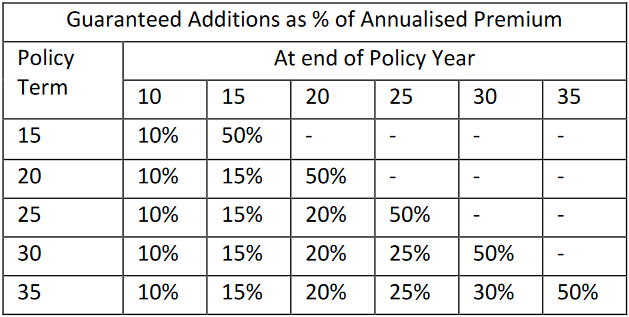

a) Guaranteed Benefits –

- For Premium Band 1, the company will add the following Guaranteed Additions to your Policy FundValue on 10th Policy Anniversary and thereafter every 5th Policy Anniversary as per the table below,while the policy is in force –

- For Premium Band 2, the Guaranteed Additions will be further enhanced by 10% of Basic Premium on the Policy Maturity Date. For paid-up policies, Guaranteed Additions will reduce in the same proportion as the basic premium paid to date to the basic premiums payable during the premium paying term and will be credited to the policy at a specified duration.

b) Death Benefit –

Your Policy Schedule shows the Basic Sum Assured applicable to your policy. Your Sum Assured is the total of Basic Sum Assured and Top-up Sum Assured, if any. If the Life Insured dies while the policy is in force, the company shall pay to the Nominee the following –

- Basic Sum Assured; plus

- Basic Fund Value as on date of intimation of death

In addition, if any top-up premium is paid, the nominee shall also receive the following –

- Top-up Sum Assured; plus

- Top-up Fund Value as on date of intimation of death

If the policy has not been discontinued, the Death Benefit shall never be less than 105% of total basic premiums and top-up premiums paid up to the date of death. Provided that where the death of the Life Insured takes place prior to the Risk Commencement Date, only the Basic Premium paid shall be payable as the Death Benefit.

The policy will terminate once the Death Benefit is paid to the nominee. The Death Benefit shall always be determined as on the date we receive intimation of death of the Life Insured.

Further any charges other than Fund Management Charges (FMC) recovered subsequent to the date of death shall be added back to the Policy fund value as available on the date of intimation of death. Where this policy has been taken for the benefit of the life insured who is a minor, the policy shall automatically vest in the life insured on his attaining age 18.

c) Waiver of Premium on Critical Illness and Total Permanent Disability Benefit –

- Classic Option – Nil

- Assured Option –

If the policyholder has chosen the Assured Options per the policy schedule and the life insured is diagnosed with the first occurrence of any one or more of the specified Critical Illnesses or Total Permanent Disability during the policy term as defined below in detail, all future premiums, if any, shall be paid by the Company when due to be paid.

All the other benefits will remain unaffected till the Policy Maturity Date or date of death whichever is earlier as shown in the Policy Schedule. All policy charges shall be deducted as and when due, except Waiver of Premium (CI / TPD), charges.

Premium waiver benefit is applicable to the first occurrence of either Total Permanent Disability or specified Critical Illness, whichever is earlier. For a paid-up policy no future installment premiums shall be paid by the Company on the diagnosis of any one or more of the specified Critical Illnesses or Total Permanent Disability during the policy term.

d) Maturity Benefit –

On the Policy Maturity Date and provided your policy is in force, the company shall pay you the Maturity Benefit. The Maturity Benefit shall be the Basic Fund Value and the Top-up Fund Value as of that date.

e) Rider Benefit –

For added protection, ABSLI Wealth Assure Plus can be enhanced by the following riders for a nominal extra cost:

i) ABSLI Accidental Death Benefit Rider Plus –

In the unfortunate event of the death of the life insured due to an accident within 180 days of the occurrence of the accident, we will pay 100% of the rider sum assured to the nominee. Also, we will refund the premiums collected after the date of Accident till the date of death, with interest as declared by us from time to time, along with death benefit payable.

ii) ABSLI Waiver of Premium Rider –

In case of the following conditions –

- The policyholder becomes completely disabled due to an illness or accident.

- The policyholder is diagnosed with any of the specified critical illnesses.

- Death of the policyholder (only if other than the Life Insured)

The company will fund all the future due to premiums and all the other benefits will remain unaffected. This benefit is applicable only once during the entire premium paying term. The rider can be taken only if you have chosen Classic Option.

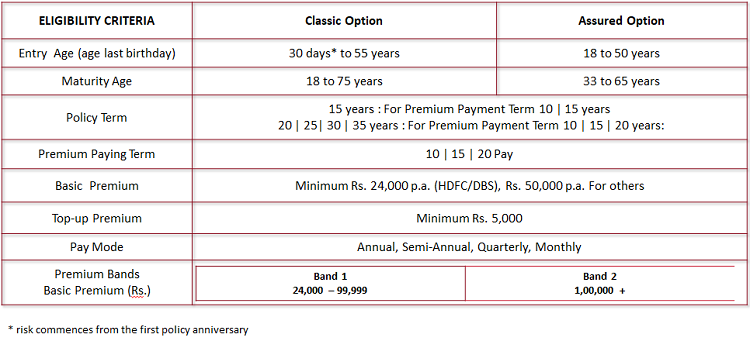

Eligibility Criteria of the Policy –

Is Partial Withdrawal allowed in the policy?

The insured is allowed to make unlimited partial withdrawals any time after the following –

- Five complete policy years or

- Life insured attains the age of 18, whichever is later.

The partial withdrawals shall first be adjusted from Top-up Fund Value (except any top-up premiums paid in the previous five years immediately preceding the date of withdrawal); if any. Once the Top-up Fund Value is exhausted, partial withdrawals would be adjusted from Basic Fund Value.

The minimum amount of partial withdrawal is Rs. 5,000. The insured is required to maintain a minimum Basic Fund Value of one basic premium payable in a year plus any top-up premiums paid in the previous five years immediately preceding the date of withdrawal. The total amount of partial withdrawal during a policy year shall not exceed 25% of the total Policy fund value at the beginning of the policy year.

When can I surrender my policy?

In case of emergencies, the policy can be surrendered anytime during the policy term. If the policy is surrendered after completion of five policy years, the Policy Fund Value will be paid immediately. If it is surrendered before lock In period, the proceeds of the discontinued policy shall be payable at the end of the lock-in period.

Can I take a loan against this policy?

The insured is not allowed to take any loan against the policy under any circumstances.

Am I allowed to switch in between funds?

The insured can change from one investment option to another investment option anytime after the first policy year. They can switch to Self-Managed Investment Option, Smart Investment Option, or Systematic Transfer Investment Option during the policy term, however, switching to the Return Optimiser Investment Option is not allowed. Switching to Systematic Transfer Investment Option is allowed only at the policy anniversary.

What is Premium Redirection in the policy?

To meet your ever-changing investment needs, you have full flexibility to redirect future premiums by changing your premium allocation percentages at any time.

What is the Reduction of Premium Payment Term?

The insured shall have an option to reduce the premium payment term provided the policy is in force for full sum assured and provided that such reduction is subject to boundary conditions of the product. This option shall be available only after basic premiums have been paid in full for the first five policy years.

Can I cancel the policy if I didn’t like its terms and conditions?

The insured will have the right to return their policy to the company within 15 days (30 days in case the policy issued under the Distance Marketing) from the date of receipt of the policy, in case you are not satisfied with the terms & conditions of your policy. This period is known as the Free Look Period.

The will pay the Policy fund value plus non allocated premiums plus charges levied by cancellation of units once they receive a written notice of cancellation (along with reasons thereof) together with the original policy documents. The company may reduce the amount of the refund by the proportionate risk premium and the expenses incurred by us on medical examination of the proposer and stamp duty charges

Various Policy Charges –

a) Premium Allocation Charge –

A Premium Allocation Charge is levied on the basic and top-up premiums when received –

- 5% of the basic premium payable in the policy years 1-10

- Nil from the 11th policy year onwards Premium Allocation Charge of 2% is levied on any top-up premium when paid.

b) Fund Management Charge –

The daily unit price of the segregated fund is adjusted to reflect the fund management charge –

- 1.00% p.a. for Liquid Plus, Income Advantage, Assure, Protector and Builder

- 1.25% p.a. for Enhancer, Creator, Capped Niy Index & Asset Allocation

- 1.35% p.a. for MNC, Magnifier, Maximiser, Multiplier, Super 20, Pure Equity and Value & MomentumWe may change the fund management charge under any segregated fund at any time subject to a maximum of 1.35% p.a. in the future subject to IRDAI approval.

c) Policy Administration Charge –

The Policy Administration Charge is deducted at the start of eve policy month by canceling units proportionately from each Segregated Fund you have at that time. The charge is as shown below, subject to a maximum of Rs 6,000 per annum.

d) Waiver of Premium (CI/TPD) Charge –

For Assured Option, a waiver of premium (CI/TPD) charge is deducted at the start of eve month. It is charged by canceling units proportionately from each segregated fund you have at that time. The charge per 1000 of Sum at Risk under the policy will depend on the gender and attained the age of the life insured. The sum at Risk is the discounted value (determined using a discount rate of 6.25% p.a.) of future installment premiums.

e) Miscellaneous Charges –

The company currently charges Rs 50 per request for a change in investment option, premium re-direction, fund switch partial withdrawal, or any additional servicing request. The company reserves the right to charge up to Rs 500 per request in the future. Any increase in the miscellaneous charges will be subject to IRDAI approval.

f) Switching Charges –

This charge is deducted from your Basic Fund Value in case you request for switching between investment options or Segregated Fund Switch. The current charges are Rs. 50 per request and reserve the right to increase this charge at any time in the future, subject to a maximum of Rs. 500 per request and prior IRDAI approval.

g) Mortality Charges –

This is deducted from your policy on each monthly processing date by the redemption of units from the segregated fund/s. This charge is guaranteed to never increase. The charge depends on the gender of the Life Insured, premium band and varies by policy year based on the then attained age of the Life Insured.

When can I revive my policy?

You can revive your policy within the revival period of three years from the discontinuance date. To revive the policy, you must pay all due and unpaid basic premiums till date and provide us with evidence of insurability satisfactory to us with respect to the Life Insured.

The effective date of the revival is when these requirements are met and approved by the company. On the effective date of the revival, the company shall follow the approach as mentioned in the Policy Discontinuance Section.

Can I make a partial withdrawal in the policy?

Yes, you can make a partial withdrawal at any time after five complete policy years and provided Life Insured is alive and has attained age 18 or older. The partial withdrawals shall first be adjusted from the Top-up Fund Value (except any top-up premiums paid in the previous five years immediately preceding the date of withdrawal); if any.

Once the Top-up Fund Value is exhausted, partial withdrawals would be adjusted from Basic Fund Value. The top-up sum assured will remain unchanged after any withdrawal from the top-up fund value.

The partial withdrawal you can make is subject to a minimum of Rs. 5,000 and a maximum equal to any excess of the Policy Fund Value over one years’ Basic Premiums payable in a year plus top-up premiums paid during the five years immediately preceding the date of partial withdrawal. The total amount of partial withdrawal in a policy year shall not exceed 25% of the total PolicyFund Value at the beginning of the policy year.

What is Policy Paid-Up?

Under the paid-up status, the policy will continue until the end of the revival period with the following modifications –

- Basic Sum Assured and Guaranteed Additions shall be reduced in proportion to the installment premiums actually paid to the total installment premiums payable during the premium paying term.

- Mortality charges will be deducted for the reduced sum at risk and other policy charges will remain unchanged.

- Under Assured Option, the Waiver of premium benefit (CI & TPD) will be terminated and no future installment premiums, if any, shall be paid by the Company, in the event of the Life Insured being diagnosed with the first occurrence of any of the covered Critical Illnesses or Total Permanent Disability.

Also, no charge will be deducted for Critical Illness and TPD benefits. If the policy is not revived before the end of the revival period, the policy shall terminate as per the Policy Discontinuance Provision.

When can my policy terminate?

Your policy will be terminated at the earliest of the following –

- The date of settlement of the policy proceeds on complete withdrawal as per the Policy Discontinuance Provision; or

- The date when the Policy Fund Value becomes zero; or

- The date of settlement of the death benefit; or

- The date of payment of the surrender value, if any; or

- The date when the maturity benefit is paid

Exclusion under the Policy –

a) Suicide Exclusion

In case of death due to suicide within 12 months from the date of commencement of the policy or from the date of revival of the policy, as applicable, the nominee or the beneficiary of the policyholder shall be entitled to the Policy fund value, as available on the date of intimation of death.

Further any charges other than Fund Management Charges (FMC) recovered subsequent to the date of death shall be added back to the Policy fund value as available on the date of intimation of death.

b) Total Permanent Disability and Critical Illness Benefit Exclusion –

The Life Insured shall not be entitled to any benefits if Total Permanent disability or covered Critical Illness results either directly or indirectly from any of the following –

- Any Pre-Existing Disease. “Pre-Existing Disease” means any condition, ailment, injury, or disease –

i) That is/are diagnosed by a physician within 48 months prior to the effective date of the policy issued by the insurer or its latest revival date; OR

ii) For which medical advice or treatment was recommended by, or received from, a physician within 48 months prior to the effective date of the policy or its latest revival date, whichever is later; OR

iii) A condition for which any symptoms and or signs if presented and have resulted within three months of the issuance of the policy or its latest revival date in a diagnostic illness or medical condition.

This exclusion will not be applicable to conditions, ailments or injuries or related condition(s) which are underwritten and accepted by insurer inception.

- Any sickness-related condition manifesting itself within 90 days from the policy commencement date or its latest revival date, whichever is later;

- AIDS and/or HIV-related complications or any sexually transmitted diseases;

- Suicide or attempted suicide or self-inflicted injury, irrespective of mental condition;

- Participation in a criminal, unlawful or illegal activity;

- Taking or absorbing, accidentally or otherwise, any intoxicating liquor, drug, narcotic, medicine, sedative or poison, except as prescribed by a registered medical practitioner;

- Nuclear contamination, the radioactive, explosive, or hazardous nature of nuclear fuel materials or property contaminated by nuclear fuel materials or accidents arising from such nature.

c) Additional Total Permanent Disability Benefit Exclusion –

In addition to the common exclusions above, the Life Insured shall not be entitled to any benefits if Total & Permanent Disability results either directly or indirectly from –

- Engaging in or taking part in professional sport(s) or any hazardous pursuits, including but not limited to, diving or riding or any kind of race; underwater activities involving the use of breathing apparatus or not; martial arts; hunting; mountaineering; parachuting; bungee jumping.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.