We always want the best for our family whether it’s security, stability, or a better lifestyle. But no matter how well planned we are, economic instability can bring turbulent times and hamper your plans.

In hard times like these, a guaranteed income proves to be a life savior. “Aditya Birla Sun Life Insurance Secure Plus Plan” offers a back-up income opportunity that guarantees more than just income, it offers peace of mind. In a time of crisis, neither we nor our family will have to sacrifice their needs and aspirations.

Features of this Policy –

i) Flexibility to choose the amount you wish to pay every year

ii) Flexibility to choose the Income Benefits –

- Option A – if you want to receive Income Benefit equal to 100% to 600% of Annualized Premium for 6 years

- Option B – if you want to receive Income Benefit equal to 200% of Annualized Premium for 12 years

iii) Inbuilt Accidental Death Benefit

iv) Enhance your insurance with appropriate rider options

v) Tax benefits under section 80C, 80D and section 10(10D) of the Income Tax Act, 1961

Benefits of this Policy –

a) Income Benefit Option –

ABSLI Secure Plus Plan offers you the flexibility to choose between two Income Benefit Options to suit your requirements.

After the completion of the policy term, the insured will start receiving Income Benefit payouts at the end of each year during the Payment Period which are fully guaranteed. These payouts are the pre-defined percentage of the Annualized premium paid by the insured. Depending on your perceived need for an increasing or a level payout, the insured can choose one of the following options at inception to receive the Income Benefit payouts during the payment period.

- Income Benefit Option A – Income benefit equal to 100%, 200%, 300%, 400%, 500% & 600% of annualized premium will be paid at the end of every year during the Payment Period for 6 years.

- Income Benefit Option B – Income Benefit equal to 200% of annualized premium will be paid at the end of every year during the Payment Period for 12 years.

b) Maturity Benefit –

On maturity date, the insured can choose to receive the commuted value of the Income Benefit as a lump sum. Once the maturity benefit is paid, the policy shall be terminated. No Income Benefit shall be payable thereafter.

The commuted value currently shall be calculated using a discounting rate of 9.00% per annum. This discounting rate is not guaranteed and is subject to change in future with prior IRDAI approval

c) Death Benefit –

In case of the unfortunate demise of the life insured during the policy term, the sum assured on death will be paid to the nominee. However, if the life insured is different from the policyholder, the policyholder will receive the death benefits. The policy shall be terminated once the Death Benefit is paid.

Sum Assured on death will be higher of the following –

- 10 times of the Annualized premium; or

- 105% of the Total Premiums Paid as on the date of death; or

- Sum Assured as the absolute amount to be paid on death

Where, Total Premiums paid means total of all the premiums received, excluding any extra premium, any rider premium, and taxes.

In case of the unfortunate demise of the life insured during the Payment Period, the nominee would continue receiving the Income Benefit as per the benefit option chosen till the end of the Payment Period.

In case the policy is issued on a minor life, if the death of the Life Insured takes place before the Life Insured attains the age of 18 years or when the first installment of Income Benefit becomes payable, then 2% of the annualized premium shall be payable as a one-time additional benefit.

d) Inbuilt accident Benefit –

In the event life insured dies due to an accident during the policy term after attaining the age of 18 years; the shall pay an additional Sum Assured to the nominee as an Accidental Death Benefit, subject to a maximum limit of Rs. 1 crore.

e) Rider Benefit –

For added protection, the insured can enhance their insurance coverage during the policy term by adding the following riders for a nominal extra cost. Different rider options are as follows –

- ABSLI Critical Illness Rider

- ABSLI Surgical Care Rider

- ABSLI Hospital Care Rider

- ABSLI Waiver of Premium Rider

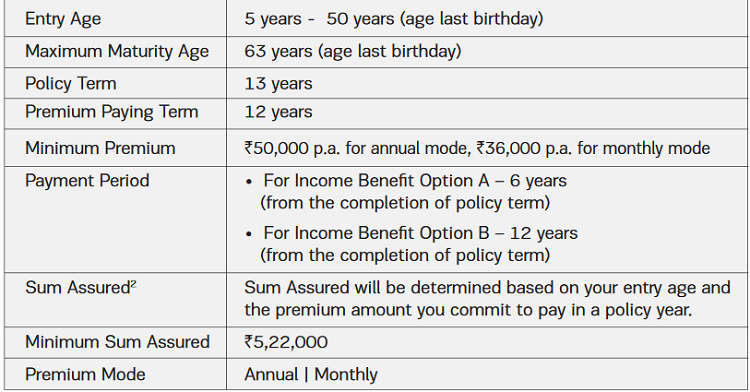

Eligibility Criteria of the Policy –

Can I surrender the policy?

Yes, the policyholder can surrender the policy and will also receive the surrender value after all due premiums for at least two full policy years are paid.

The Guaranteed Surrender Value shall be a percentage of total premiums paid. The Guaranteed Surrender Value will vary depending on the year the policy is surrendered. Your policy will also be eligible for a Special Surrender Value. The policy shall be terminated once the Surrender Value is paid.

The surrender benefit is the higher of the following –

- Guaranteed Surrender Value, or

- Special Surrender Value

Can I get a loan against this policy?

Yes, loan against this policy is allowed once the policy acquires a Surrender Value. The minimum loan amount is Rs 5,000 and the maximum up to 85% of your Surrender Value.

The company shall charge an interest on the outstanding loan balance at a rate declared by the company which is 2% plus the base rate of the State Bank of India.

Any outstanding loan balance will be recovered by the company from policy proceeds due for payment and will be deducted before any benefit is paid under the policy. If the outstanding policy loan balance equals or exceeds the Surrender Value of your policy at any time, then the policy shall be terminated without value.

Can I return the policy if I didn’t like its terms and conditions?

Yes, you can return the policy to the company within 15 days (30 days in case of Distance Marketing) from the date of receipt of the policy. This 15 day period is known as the Free Look Period.

The company will refund the premium paid once they receive in writing notice of cancellation (along with reasons thereof) together with the original policy documents. Further to this, the company will deduct the proportionate risk premium for the period of cover and expenses incurred by the company on medical examination and stamp duty charges while issuing your policy.

Is there any grace period and revival terms in the policy?

If the insured is unable to pay the premium by the due date, then the insured will be given a grace period of 30 days and during this grace period, all coverage under your policy will continue.

If the insured does not pay the premium within the grace period, the following will be applicable –

- In case you have not paid premiums for two full years, then all benefits under your policy will cease immediately.

- In case you have paid premiums for at least two full years, then your policy will continue on a Reduced Paid-up basis.

If the policy has lapsed, then the insured can revive their policy for its full coverage within five years from the due date of the first unpaid premium by paying all outstanding premiums together with interest as declared by the company from time to time and by providing evidence of insurability satisfactory to the company. Upon revival, your benefits shall be restored to their full value.

What is reduced paid-up benefit in the policy?

In case of discontinuance of premiums after having paid premiums for at least two full years, policy will not lapse but continue on a Reduced Paid-Up basis.

Under Reduced Paid-Up, Sum Assured on Death, Accidental Death Benefit, Income Benefit, and additional benefit on death (applicable on minor lives) shall be reduced in proportion to the premiums actually paid to the total premiums payable during the policy term. Rider Benefit, if any will cease.

When can my policy terminate?

Your policy will terminate at the earliest of the following –

- The date of settlement of Death Benefit; or

- The date of payment of the surrender value; or

- The date of payment of the last Income Benefit during the Payment Period; or

- The date on which the revival period ends after the policy has lapsed if fewer than two full years installment premiums have been paid;

- The date of early termination of the policy by the Policyholder before the policy acquires any paid-up value; or

- The date on which the outstanding loan amount exceeds the surrender value.

Exclusions under the Policy –

a) Suicide Exclusion –

The company will pay the total premiums paid till date or surrender value available on the date of death, if higher in the event the life insured dies due to suicide, within 12 months from the date of commencement of risk under the policy or from the date of revival of the policy, as may be applicable provided the policy is in force.

b) Accidental Death Benefit Exclusion –

The Life Insured will not be entitled to the Accidental Death Benefit for any accidental death directly or indirectly due to or caused, occasioned, accelerated or aggravated by any of the following –

- Death as a result of any disease or infection other than directly linked with an accident.

- Attempted suicide or self-inflicted inju while sane or insane.

- Participation of the insured person in criminal, illegal activity, or unlawful act with criminal intent.

- Taking or absorbing any intoxicating liquor, drug, narcotic, medicine, sedative or poison, except as prescribed by a licensed doctor other than life insured.

- Nuclear Contamination; the radioactive, explosive, or hazardous nature of nuclear fuel materials or property contaminated by nuclear fuel materials or accidents arising from such nature.

- Entering, exiting, operating, servicing, or being transported by any aerial device or conveyance except when on a commercial passenger airline on a regularly scheduled passenger trip over its established passenger route.

- Engaging in or taking part in professional sport(s) or any hazardous pursuits, including but not limited to, diving or riding or any kind of race; underwater activities involving the use of breathing apparatus or not; martial arts; hunting; mountaineering; parachuting; bungee jumping.

- War, terrorism, invasion, the act of a foreign enemy, hostilities (whether war be declared or not), armed or unarmed truce, civil war, mutiny, martial law, rebellion, revolution, insurrection, milita power, riot or civil commotion, strikes. War means any war whether declared or not.

- Service in the armed forces in time of declared or undeclared war or while under orders for warlike operations or restoration of public order.

- Accident occurring while or because the Insured is under the influence of Alcohol or Solvent abuse or taking of drugs, narcotics or psychotropic substances unless taken in accordance with the lawful directions and prescription of a registered medical practitioner.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.