This was the last budget of BJP govt before the next elections and it was expected that they would announce some very good changes in budget which will be for middle class. From last many years, the tax slab rates have not seen any major changes (except few small changes) . The 80C limit and housing loan interest deducted limits were revised few years back, but still the common man expected some really good news.

While the budget was very good for farmers and rural sectors in general and also for senior citizens, it was extremely disappointing for middle class who are mainly into jobs.

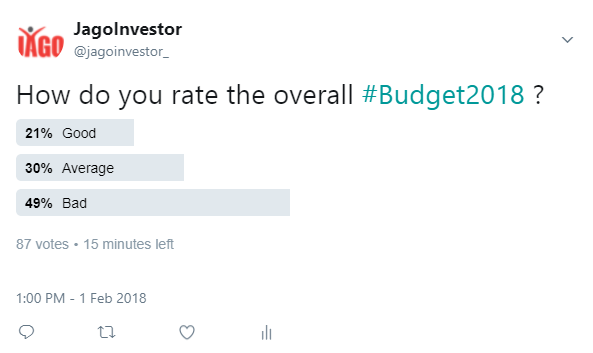

On twitter, I asked about people opinion on the budget and as expected, most of the people were not happy about it.

12 Things related to the middle class in 2018 BUDGET :

| 1. No change in Tax Slabs | 2. Standard Deduction of Rs 40,000 |

| 3. Long Term Capital gain Tax on Equity Gains at 10% | 4. Dividend Distribution tax of 10% on Equity |

| 5. Increase in Health and Education Cess to 3% to 4% | 6. No tax on interest from Deposits up to Rs 50,000 for senior citizens |

| 7. No TDS for deposits for Senior Citizens up Rs 50,000 | 8. Health Insurance deduction increased from 30,000 to 50,000 for senior citizens |

| 9. Increase in limits for critical illness treatments | 10. Corporate tax @25% for companies with turnover of less than 250 crores |

| 11. EPF contribution of new women workers capped at 8% | 12. Health Insurance Scheme for 5 lacs sum assured for majority |

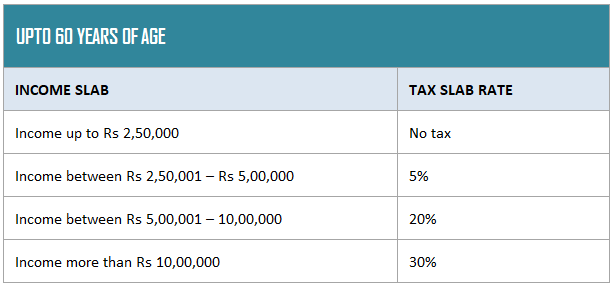

1. No change in Tax Slabs

One of the biggest disappointments for everyone in this budget was that the tax slabs were not changed at all. In media we keep hearing on how the minimum limit for taxation should be raised from 2.5 lacs to 5 lacs, but it was not even raised to 3 lacs.

Below are the slabs.

So you will still pay the taxes as per old slab rates only.

2. Standard Deduction of Rs 40,000

There is a standard deduction of Rs 40,000 allowed in this budget, which means that you can now reduce your taxable salary by Rs 40,000 directly along with other deductions and benefits. But this only looks great on paper, because the transport allowance of Rs 19,200 and medical reimbursement of Rs 15,000 are now removed as benefits.

So earlier anyways one was able to claim around Rs 34,200 ,so the added advantage is only for Rs 5,800 more.

You will only save a little headache of providing the medical bills which you used to do for claiming Rs 15,000 (a lot of people used to provide fake bills). So now the process will be simple

3. Long Term Capital gain Tax on Equity Gains at 10%

The biggest news in this budget was the reintroduction of 10% tax on long term capital gains on equity without Indexation benefits. Let me touch base on this a bit as this is very important to understand, however I will make another details article soon on this.

Till now, if you held equity stocks or equity mutual funds for more than 1 yr, then all the profits you made were tax free when you sold them. However now you will have to pay 10% tax on the profits on profits above Rs 1 lac.

However this will only apply on the profits made after 31st Jan 2018 and if you sell your holdings after 31st Mar 2018. All the gains you have made till 31st Jan 2018, are protected and now they will be considered as your cost price.

So if you had bought a stock or equity mutual funds for Rs 1 lacs in May 2017, and its value on 31st Jan 2018 was 1.2 lacs, then you do not pay any tax on this profit of Rs 20,000 . Now your cost price will become 1.2 lacs .

Now if you sell it in let’s say Dec 2018 for Rs 1.5 lacs , then your capital gains will be 1.5 lacs – 1.2 lacs = Rs 30,000 (not 50k).

| Particulars | Before Budget | After Budget |

| Buy Date : 1st June 2016 | Rs 5,00,000 | Rs 5,00,000 |

| Sell Date : 1st July 2019 | Rs 10,00,000 | Rs 10,00,000 |

| Price on 31st Jan 2018 | Rs 7,00,000 | Rs 7,00,000 |

| Purchase Price Considered | Rs 5,00,000 | Rs 7,00,000 |

| Capital Gains | Rs 5,00,000 | Rs 3,00,000 |

| Capital Gains Exempted | Rs 5,00,000 (100%) | Rs 1,00,000 (as per new rule) |

| Capital Gains which will be taxes | Rs 0 | Rs 2,00,000 |

| Tax Rate | NIL | 10% |

| Tax Payable | NIL | Rs 20,000 |

Note that the capital tax gains will come into picture only when you sell your holdings and the tax will be applicable only on the profits above Rs 1 lac.

Capital gains on equity was already there before 2004, At that time it was 20% on profits with indexation or 10% without indexation. Now they are reintroduced.

Note that if you sell your holdings before 31st March 2018, the old rules still apply. This new rules are only going to be in picture if you sell after 1st April, 2018.

What should you do?

Nothing!

Dont get too emotional about the tax part. I know people hate paying tax in any form, and especially when it comes as a surprise. But the truth is that the capital gains tax was there before 2004. Its not reintroduced. You should feel happy that for 13 yrs, there was no taxes on equity gains and those of you who have made great returns in past decade enjoyed it tax free.

Also, the capital gains tax on equity is one of the lowest in India at 10% . Most of the other countries tax it at anywhere from 15-35% . So we are not in bad shape.

Equities are still one of the best asset classes, and now lets focus on your wealth creation over long term. The fundamentals are still strong and the equity is set to give great returns over long term. Even with this 10% tax, equities are the best thing to invest in (for long term)

4. Dividend Distribution tax of 10% on Equity

Before of the LTCG on equity , now the dividends from equity mutual funds and stocks will also be taxed at 10%. However this will at source. Which means that it will get deducted by the company itself and you will get the dividend post deduction of 10% . You will not be paying any tax at your end, so there is no headache of all that calculation and CA work

For example, if the company announces Rs 10 dividend per share/unit and you are suppose to get Rs 10,000 dividend , then you will get Rs 9,000 and Rs 1,000 will be paid to govt directly by the company.

This applies to both dividend and dividend reinvestment option in mutual funds.

The dividend distribution tax and treatment for debt mutual funds is still the same. No changes in that.

5. Increase in Health and Education Cess to 3% to 4%

The cess was increased from 3% to 4% in this budget.

Cess is something which you pay extra on the income tax. So if you are in 20% income tax bracket, then you will pay 4% more on 20% , which will make your income tax rate as 20.8% .

If your income tax amount comes to Rs 20,000 per year, then your cess will be 4% of Rs 20,000 = Rs 800.

With 1% increase in cess, you will pay Rs 200 more now (if your income tax is 20,000). This will increase your tax burden by a very marginal amount.

6. No tax on interest from Deposits up to Rs 50,000 for senior citizens

This budget has given a lot of benefits for senior citizens.

One big benefit is that now there won’t be any tax on interest on all the deposits and bank interest up to Rs 50,000 for senior citizens. This will include interest of saving bank account, fixed deposits and recurring deposits.

7. No TDS for deposits for Senior Citizens up Rs 50,000

Now there won’t be any TDS deductions for interest from deposits (fixed deposits and recurring deposits) upto Rs 50,000. Till now the TDS was deducted as per provisions of section 194A , if the interest was above Rs 10,000 , but now it will be Rs 50,000 limit.

8. Health Insurance deduction increased from 30,000 to 50,000 for senior citizens

Under section 80D, there was an exemption of up to 30,000 per year for health insurance premiums for senior citizens, but now it has been increased up to Rs 50,000 . It’s a major relief because for senior citizens the health insurance premiums are very high and in most cases, it’s more than 40-50k anyways.

9. Increase in limits for critical illness treatments

There is an increase in the deduction limit for medical expenditure for certain illness up to Rs 1 lac for all senior citizens under section 80DDB . So in a particular year, if a senior citizen spends money on treatment of these illness, they can claim deduction on up to Rs 1 lac.

Here is the list of all illness covered under Sec 80DDB

- Dementia

- Dystonia Musculorum Deformans

- Motor Neuron Disease

- Ataxia

- Chorea

- Hemiballismus

- Aphasia

- Parkinsons Disease

- Malignant Cancers

- Full Blown Acquired Immuno-Deficiency Syndrome (AIDS)

- Chronic Renal failure

- Hematological disorders

- Hemophilia

- Thalassaemia

Increase in deduction limit for medical expenditure for certain critical illness from Rs. 60,000 (in case of senior citizens) and from Rs. 80,000 (in case of very senior citizens) to Rs. 1 lakh for all senior citizens, under section 80DDB.

10. Corporate tax @25% for companies with turnover of less than 250 crores

Those of you who are running any companies, the good news is that the tax rate will be 25% now instead of 30%, provided your turnover is less than Rs 250 crores yearly.

11. EPF contribution of new women workers capped at 8%

Now all the new women how will join the workforce for the first time, their EPF will be deducted @8% only instead of 12% for the first 3 yrs, also the govt will now provide 12% from their side also. It’s still not clear if the employer contribution will also be extra other than govt contribution.

12. Health Insurance Scheme for 5 lacs sum assured for majority

Another big news was that now govt is bringing a health insurance scheme for masses, where each family will be entitled for Rs 5 lac sum assured each year. But this will be mostly for weaker section of society and I don’t think any of our readers will be eligible for this.

There are no details about this scheme right now in budget and no allocations is made for this. I would rather wait for more details before commenting on this more. However if successfully implemented it would be wonderful for our country.

Let us know what do you think about the budget? What is one major disappointment and one great thing about the budget for you?