ICICI Pru Life Time Classic Policy – Review, Features and Benefits

ICICI Pru LifeTime Classic Policy is a unit-linked insurance plan. In this policy, the investment risk in the investment portfolio is borne by the Policyholder. This plan offers the insured a life insurance cover to protect their family in case of your unfortunate demise along with multiple choices on how to invest to help you achieve your financial goals.

The plan also offers 4 portfolio strategies that can be selected according to your personal investment needs.

Features of this Policy –

- You can choose from 4 portfolio strategies according to your investment style to achieve your specific financial goals.

- Invest in your choice of funds – various choice of equity, balance, and debts funds, you can switch between them anytime.

- On the death of the policyholder, the nominee gets life cover and prevailing fund value as a lump sum payout.

- Tax benefits on premiums paid up to Rs 46,800 under Section 80C of Income Tax Act, 1961.

- Loyalty Additions and Wealth Boosters get added to your investment, just pay premium regularly, and stay invested.

- You can move your money between various fund options to get potentially better returns. 4 times free switches in a policy year.

- You can increase your investment in the plan anytime by using the online top-up facility.

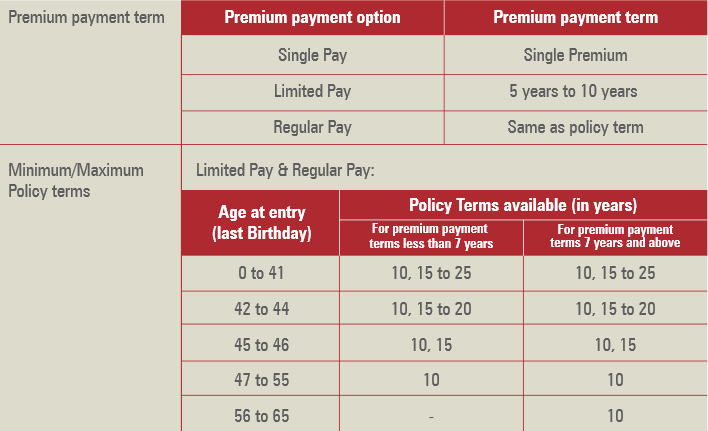

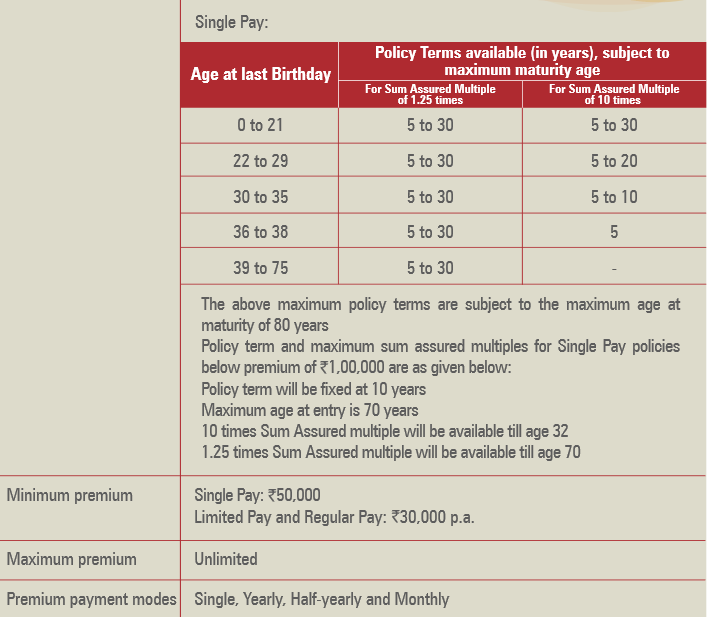

- You can pay the premium monthly, half-yearly, yearly, or make a one-time payment.

- There is no loan facility in the policy.

4 Portfolio Strategies –

a) Target Asset Allocation Strategy –

This strategy enables you to choose an asset allocation that is best suited to your risk appetite and maintains it throughout the policy term. You can allocate your premiums between any two funds available with this policy, in the proportion of your choice.

Your portfolio will be rebalanced every quarter to ensure that this asset allocation is maintained. The re-balancing of units shall be done on the last day of each policy quarter. You can avail of this option at inception or at any time later during the policy term.

b) Trigger Portfolio Strategy 2 –

For an investor, maintaining a pre-defined asset allocation is a dynamic process and is a function of constantly changing markets. The Trigger Portfolio Strategy 2 enables you to take advantage of substantial equity market swings and invest on the principle of “buy low, sell high”.

Under this strategy, your investments will initially be distributed between two funds Multi-Cap Growth Fund, an equity-oriented fund, and Income Fund – a debt-oriented fund in a 75%: 25% proportion. The fund allocation may subsequently get altered due to market movements.

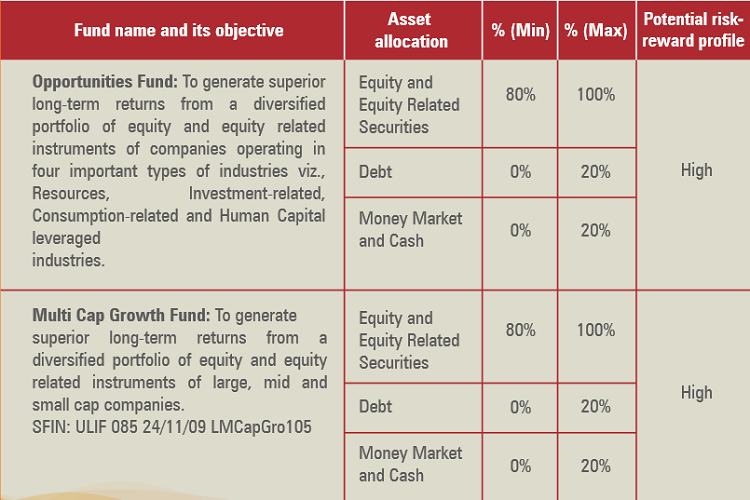

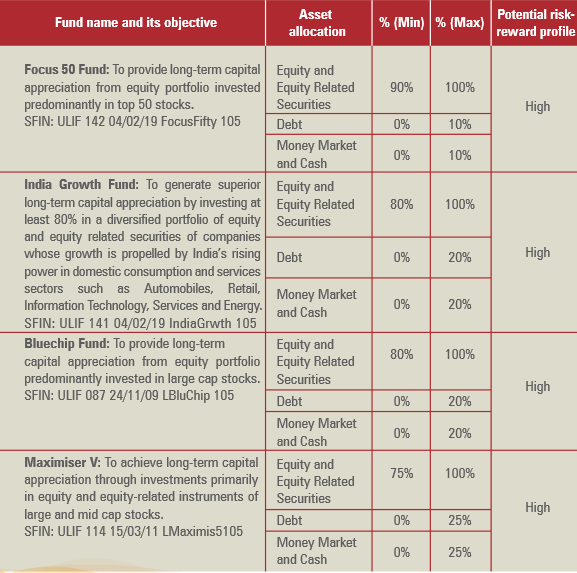

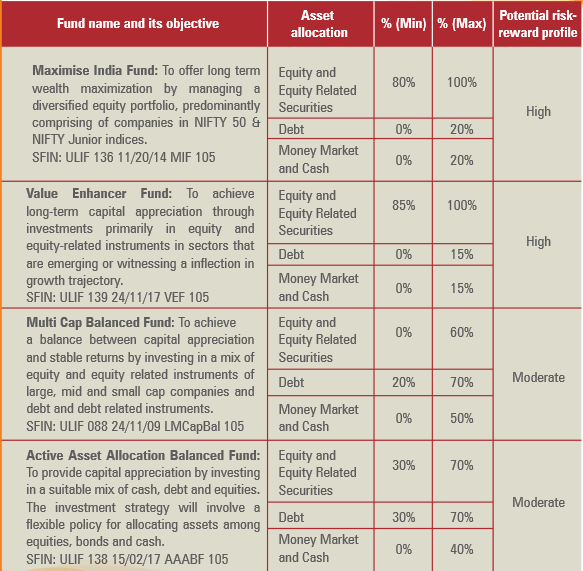

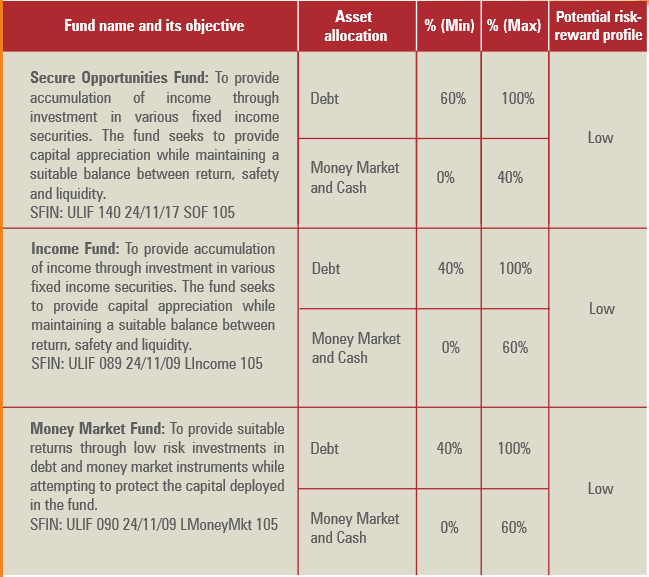

c) Fixed Portfolio Strategy –

This strategy enables you to manage your investments actively. Under this strategy, you can choose to invest your money in any of the following fund options in proportions of your choice. You can switch money amongst these funds using the switch option. The details of the funds are given in the table below:

d) Lifecycle based Portfolio Strategy 2 –

Your financial needs are not static and keep changing with your life stage. It is, therefore, necessary that your policy adapts to your changing needs. This need is fulfilled by the LifeCycle based Portfolio Strategy 2.

Benefits of this Policy –

a) Death Benefit –

In the unfortunate event of the death of the Life Assured during the term of the policy the following will be payable to the Nominee, or in the absence of a Nominee the Legal heir.

i) In the case of Single Pay policies, Death Benefit = A or B or C whichever is highest, Where,

- A = Sum Assured including Top-up Sum Assured, if any

- B = Fund Value including Top-up Fund Value, if any

- C = Minimum Death Benefit

ii) In the case of Limited Pay and Regular Pay policies, For age at entry less than 50 years, Death Benefit = (A+B) or C whichever is higherWhere,

- A = Sum Assured including Top-up Sum Assured, if any

- B = Fund Value including Top-up Fund Value, if any

- C = Minimum Death Benefit

iii) For the age at entry greater than or equal to 50 years, Death Benefit = A or B or C whichever is highest, Where,

- A = Sum Assured including Top-up Sum Assured, if any

- B = Fund Value including Top-up Fund Value, if any

- C = Minimum Death Benefit

Minimum Death Benefit will be 105% of the total premiums including Top-up premiums if any received up to the date of death.

b) Maturity Benefit –

On maturity of the policy, you will receive the Fund Value including the Top-up Fund Value, if any. You will have an option to receive the Maturity Benefit as a lump sum or as a structured payout using the Settlement Option.

- With this facility, you can opt to get payments on a yearly, half-yearly, quarterly or monthly (through ECS) basis, over a period of one to five years, post maturity.

- The first payout of the settlement option will be made on the date of maturity.

- At any time during the settlement period, you have the option to withdraw the entire Fund Value.

- During the settlement period, the investment risk in the investment portfolio is borne by you.

- Only the Fund Management Charge, switch charge, and mortality charge, if any, would be levied during the settlement period.

- No Loyalty Additions or Wealth Boosters will be added during this period.

- You may avail facility of switches as per the terms and conditions of the policy. Partial withdrawals and CIPS are not allowed during the settlement period.

- Rider cover shall cease on the original date of maturity.

- In the event of the death of the Life Assured during the settlement period, Death Benefit payable to the nominee as lump sum will be – Death Benefit during the settlement period = A or B whichever is highest Where, A = Fund Value including Top-up Fund Value, if any B = 105% of total premiums paid On payment of Death Benefit, the policy will terminate and all rights, benefits and interests under the policy will be extinguished.

- On payment of the last installment of the settlement option, the policy will terminate and all rights, benefits, and interests under the policy will be extinguished.

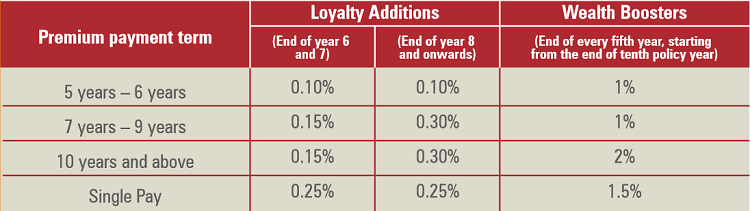

c) Loyal Additions and Wealth Boosters –

The Company will allocate extra units as below provided all due premiums have been paid:

- For single pay policies with a policy term of 5 years, a loyalty addition of 0.25% of the average of daily Fund Values, including Top-up Fund Value, if any, in that same policy year, will be payable at the end of the fifth policy year.

- Each Loyalty Addition will be a percentage of the average of daily Fund Values including Top-up Fund Value, if any, in that same policy year as mentioned in the table above.

- Wealth Boosters will be a percentage of the average Fund Values including Top-up Fund Value, if any, on the last business day of the last eight policy quarters.

- Loyalty Additions and Wealth Boosters will be allocated among the funds in the same proportion as the value of total units held in each fund at the time of allocation.

- The allocation of Loyalty Additions and Wealth Boosters is guaranteed and shall not be revoked by the Company under any circumstances.

- If the premium payment is discontinued anytime after 5 years, the number of years for which premiums have been paid will be considered as the premium paying term for the purpose of deciding the Loyalty Additions & Wealth Boosters to be paid for the rest of the policy term as per the table above.

d) Rider Benefit –

Additional protection through ICICI Pru Unit Linked Accidental Death Rider. The insured will be paid in addition to the death benefit if death is due to an accident.

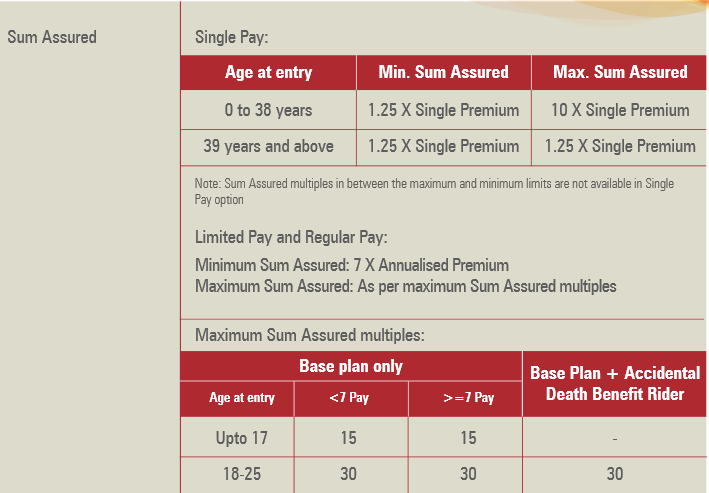

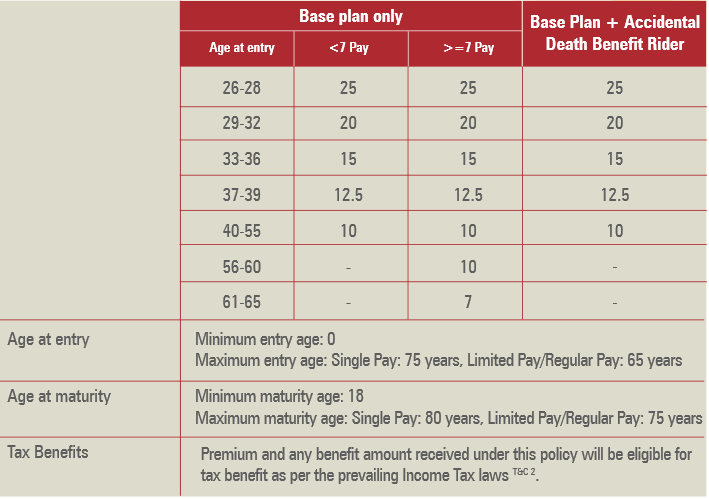

Eligibility Criteria of the Policy –

Can I make switches between funds?

If you choose the Fixed Portfolio Strategy, you can switch units from one fund to another depending on your financial priorities and investment outlook as many times as you want. Four switches are free in a policy year. Switches in excess of 4 free switches in a policy year will be charged at Rs 100 per switch. Unutilized free switches can not be carried forward in the next policy year. The minimum switch amount is Rs 2,000.

What is the Top-up facility in the policy?

The insured can invest any surplus money as Top-up premium, over and above the base premium(s), into the policy. The following conditions apply to Top-ups –

- The minimum Top-up premium is Rs 2,000.

- Your Sum Assured will increase by Top-up Sum Assured when you avail of a Top-up. Limits on Top-up Sum Assured multiples are the same as those applicable for the Single Pay premium payment option and are based on the age of the life assured at the time of paying the Top-up premium.

- Top-up premiums can be paid any time except during the last five years of the policy term, subject to underwriting, as long as all due premiums have been paid.

- A lock-in period of five years would apply for each Top-up premium for the purpose of partial withdrawals only.

- At any point during the term of the policy, the total Top-up premiums paid cannot exceed the sum of base premium(s) paid till that time.

- The maximum number of top-ups allowed during the policy term is 99.

Is it possible to make any Change in the Portfolio Strategy?

You can change your portfolio strategy up to four times in a policy year. This facility is provided free of cost. Any unutilized CIPS cannot be carried forward to the next policy year.

What is Premium Redirection in the policy?

This feature is applicable only if the insured has opted for the Fixed Portfolio Strategy and provided the money is not in the DP Fund. If the insured has selected Fixed Portfolio Strategy, at policy inception, by specifying the funds and the proportion in which the premiums are to be invested in the funds.

At the time of payment of subsequent premiums, the split may be changed without any charge. This will not count as a switch. This benefit is not applicable to the Single Pay option.

Is there any partial withdrawal benefit in this policy?

Irrespective of the portfolio strategy selected by the insured, partial withdrawals are allowed after the completion of five policy years and on payment of all premiums for the first five policy years. The insured can make an unlimited number of partial withdrawals as long as the total amount of partial withdrawals in a year does not exceed 20% of the Fund Value in a policy year.

The partial withdrawals are free of cost. The following conditions apply on partial withdrawals, they are as follows –

- Partial withdrawals are allowed only after the first five policy years and on payment of all premiums for the first five policy years.

- Partial withdrawals are allowed only if the Life Assured is at least 18 years of age.

- For the purpose of partial withdrawals, the lock-in period for the Top-up premiums will be five years or any such limit prescribed by IRDAI from time to time.

- Partial withdrawals will be made first from the Top-up Fund Value, as long as it supports the partial withdrawal, and then from the Fund Value built up from the base premium(s).

- Partial withdrawal will not be allowed if it results in termination of the policy

- The minimum value of each partial withdrawal is Rs 2,000.

Can I increase or decrease the sum assured?

The insured can choose to increase or decrease their Sum Assured at any policy anniversary during the policy term provided all due premiums have been paid.

- An increase or decrease in Sum Assured will not change the premium payable under the policy.

- An increase in Sum Assured is allowed, subject to underwriting, before the policy anniversary on which the life assured is aged 60 years completed birthday.

- The decrease in Sum Assured is allowed up to the minimum allowed under the given policy.

- Such increases or decreases would be allowed in multiples of Rs 1,000, subject to maximum Sum Assured multiple limits. Any medical cost for this purpose would be borne by you and will be levied by the redemption of units.

Can I increase the premium payment term?

Provided all due premiums have been paid, the insured can choose to increase the Premium Payment Term by notifying the Company.

- An increase in the Premium Payment Term must always be in multiples of one year.

- Decreasing the Premium Payment Term is not allowed.

This benefit is not applicable to the Single Pay option.

Can I increase or decrease Policy Term?

The insured can choose to increase or decrease their policy term by notifying the Company.

- An increase or decrease in terms is allowed subject to the Policy terms allowed under the given policy

- An increase in policy term is allowed, subject to underwriting.

When can I surrender the policy?

During the first five policy years, on receipt of intimation that the insured wishes to surrender the policy, the Fund Value including Top-up Fund Value, if any, after deduction of applicable Discontinuance Charge, shall be transferred to the Discontinued Policy Fund (DP Fund).

The insured or your nominee, as the case may be, will be entitled to receive the Discontinued Policy Fund Value, on the earlier of death or the expiry of the lock-in period. Currently, the lock-in period is five years from policy inception. On surrender after completion of the fifth policy year, you will be entitled to the Fund Value including Top-up Fund Value, if any.

How is money treated in the policy while the money is in the DP Fund?

While money is in the DP Fund –

- Risk Cover and Minimum Death Benefit will not apply

- A Fund Management Charge of 0.50% p.a. of the DP Fund will be made. No other charges will apply.

- From the date monies enter the DP Fund till the date they leave the DP Fund, a minimum guaranteed interest rate declared by IRDAI from time to time will apply. The current minimum guaranteed interest rate applicable to the DP Fund is 4% p.a.

When can I revive my lapsed policy?

The revival period is three years from the date of the first unpaid premium. Revival will be based on the prevailing Board approved underwriting guidelines.

In case of revival of the policy, the company shall collect from you the following –

- All due and unpaid premiums without charging any interest or fee,

- Levy policy administration charges and premium allocation charges as applicable during the discontinuance period. No other charges shall be levied,

On payment of overdue premiums before the end of the revival period, the policy will be revived. On revival, the policy will continue with benefits and charges, as per the terms and conditions of the policy. The insured shall have an option to revive the policy without or with the rider if any.

The money will be invested in the segregated fund(s) chosen by the insured at the NAV as on the date of such revival.

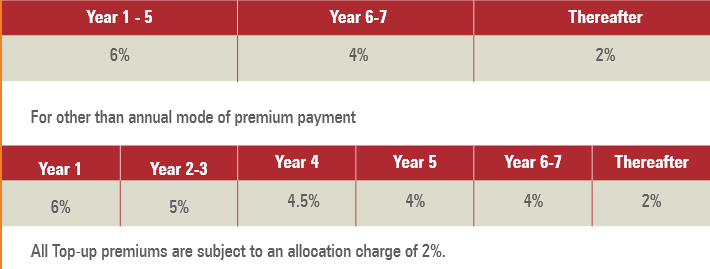

Charged under the policy –

i) Premium Allocation Charge

Premium Allocation Charge depends on the premium payment option and the premium payment mode chosen. It is deducted from the premium amount at the time of premium payment and units are allocated in the chosen funds thereafter. This charge is expressed as a percentage of the premium.

- Single Pay: 3%

- Limited Pay and Regular Pay – For the annual mode of premium payment

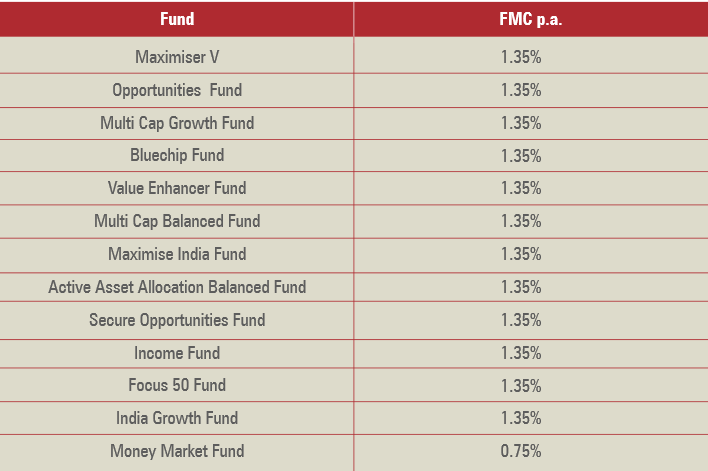

ii) Fund Management Charge (FMC)

The following fund management charges will be applicable and will be adjusted from the NAV on a daily basis. This charge will be a percentage of the Fund Value.

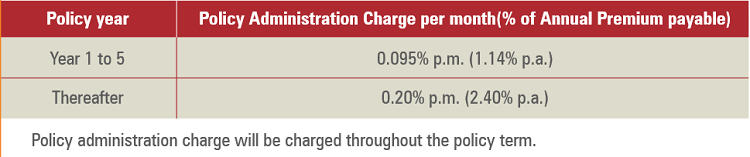

iii) Policy Administration Charge –

Policy Administration Charge will be levied every month by the redemption of units, subject to a maximum of Rs 500 per month (Rs 6,000 p.a.). The policy administration charge will be as set out below –

- Single Pay – Rs 60 per month. (Rs 720 p.a.) for the first five policy years.

- Other than Single Pay –

Can I cancel the policy if I didn’t like its terms and conditions?

If the insured is not satisfied with the terms and conditions of this policy, then the policy can be returned to the company with reasons for cancellation within 15 days from the date of receipt of the policy document and 30 days from the date of receipt of the policy document, if your policy is purchased through Distance Marketing Distance.This period is known as the Free Look Period.

On cancellation of the policy during the free-look period, the insured shall be entitled to an amount which shall be equal to non-allocated premium plus charges levied by cancellation of units plus Fund Value at the date of cancellation less stamp duty expenses under the policy and expenses borne by the company on medical examination.

Is there any grace period in the policy?

The grace period for payment of premium is 15 days for monthly mode of premium payment and 30 days for other modes of premium payment.

Exclusion under the policy –

- Suicide Exclusion –

If the Life Assured, whether sane or insane, commits suicide within 12 months from the date of commencement of the policy or from the date of policy revival, only the Fund Value, including Top-up Fund Value, if any, as available on the date of intimation of death, would be payable to the Claimant.

Any charges other than Fund Management Charges and guarantee charges, if any, recovered subsequent to the date of death shall be added back to the fund value as available on the date of intimation of death. If the Life Assured, whether sane or insane, commits suicide within 12 months from the effective date of the increase in Sum Assured, then the amount of increase shall not be considered in the calculation of the death benefit.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.