Bajaj Allianz LongLife Goals – Review, Features and Benefits

Bajaj Allianz Life LongLife Goal, is a non-participating, life, individual whole of life Unit Linked regular premium payment Endowment Plan, which helps one acquire a healthy retirement corpus in market-linked investment instruments over a long-term by investing their money.

Features of this Policy –

- The policyholder can receive income till the age of 99 yrs in the form of periodic installments.

- The policyholder can enjoy the life cover till the age of 99 yrs.

- The policyholder has the option to choose between 2 plan variants such as LongLife Goal without Waiver of Premium & LongLife Goal with Waiver of Premium.

- The top-Up premium option is not available under this policy.

- Periodical Return of Life Cover charges.

- The policyholder will get a choice to choose between 8 funds.

- Loyalty Additions every year from 5thPolicy Year till 25 Policy Year.

- Choice of 4 investment portfolio strategies such as Investor Selectable Portfolio Strategies, Wheel of Life Portfolio Strategies II, Trigger Based Portfolio Strategy, Auto Transfer Portfolio Strategy.

- The policyholder also has an option to reduce the premium.

- Tax benefits on premium paid up to Rs.1.5 Lakhs.

Benefits of this Policy –

a) Maturity Benefit –

The policyholder will receive the maturity benefit as the Fund Value as on the Maturity Date, provided the Policy is in force.

b) Death Benefit –

If all due Premiums are paid, then, in case of unfortunate death of the Life Assured during the Policy Term, the Death Benefit payable will be higher of the following –

- Prevailing Sum Assured

- Fund Value

The Death Benefit is subject to the Guaranteed Death Benefit of 105% of the Total Premiums paid, till the date of death.

Total Premiums paid shall be the sum of all Regular Premiums paid till date.

c) Partial Withdrawal –

The policyholder has the option to make partial withdrawals, any time after the fifth Policy Year, subject to the following conditions –

- The Fund Value should not fall below 105% of the prevailing Annualized Premium ( Premium Payment Term), after a partial withdrawal.

- The minimum amount of partial withdrawal at any time is Rs 5,000.

- A partial withdrawal shall not be allowed if it will result in termination of the Policy.

- In the case of minor Life Assured, partial withdrawal is allowed after attaining Age 18 years.

- Under Investor Selectable Portfolio Strategy, the policyholder will have the option to choose the fund they want to do partial withdrawals from. In the Wheel of Life Portfolio Strategy, Trigger Based Portfolio Strategy or Auto Transfer Portfolio Strategy withdrawal of units from each fund will be done in the same proportion as the value of the Units held in that Fund as on date of withdrawal. The policyholder will not have any choice to opt for the fund from which the partial withdrawal of units is to be done.

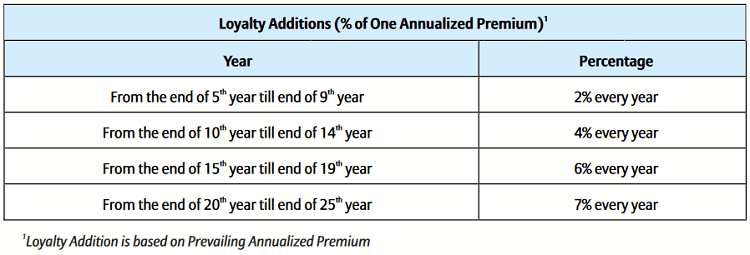

d) Loyalty Additions –

The Company shall allocate Loyalty Additions to the Fund Value as a percentage of one Annualized Premium at the end of each Policy Year starting from the end of 5Policy Year, provided all due Regular Premiums have been paid up to date. The Loyalty Additions payable are as below –

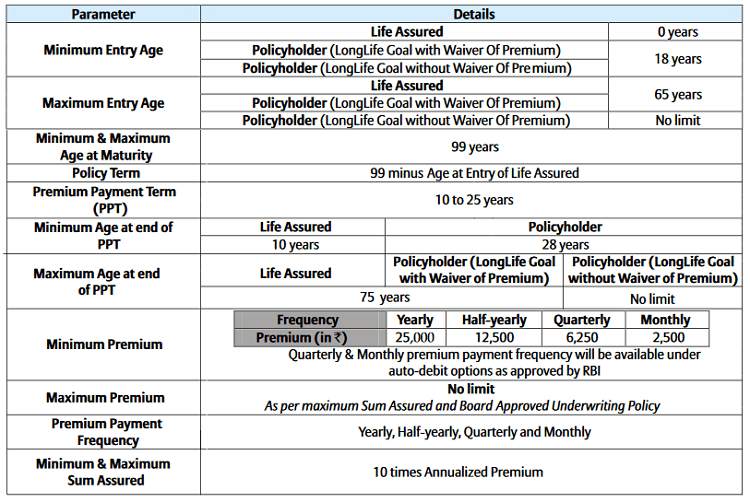

Eligibility Criteria of the Policy –

Is there any surrender benefit in the policy?

The policyholder has the option to surrender their Policy at any time.

- On surrender during the lock-in period of first five years of your policy, the Fund Value, less the applicable Discontinuance/Surrender charge, as on the Date of Surrender, will be transferred to the Discontinued Life Policy Fund (maintained by the Company), and risk cover under the Policy shall cease immediately.

- On surrender during the lock-in period, the option to revive the Policy will not be available to such a Discontinued Life Policy. The Discontinuance Value as at the end of the lock-in period will be available as Surrender Benefit.

- On surrender after the lock-in period of the first five years of your policy, the surrender value available will be Fund Value, as on the date of surrender, and will be payable immediately.

- Under LongLife Goal with Waiver of Premium, if Waiver of Premium has already been triggered under the Policy, then, the present value of future Waiver of Premium installments, discounted at 4% p.a. (from the date of surrender), shall be paid.

- The Policy shall thereafter terminate upon payment of the full Surrender Benefit by the Company.

Is there any option where I can reduce the premium of the policy?

- The policyholder will have the option to reduce the prevailing premium under the policy after the first five (5) policy years.

- The reduction can be up to a maximum of 50% of the Premium at the inception of the Policy.

- Once reduced, the same cannot be increased, even to extent of the Premium at the inception of the Policy.

- On receipt of the reduced premium, the prevailing sum assured under the policy will be correspondingly reduced.

When can my policy terminate?

a) If the policyholder has opted for the settlement option then –

- All risk cover under the Policy will terminate immediately, and the Policy will terminate on payment of the last instalment.

b) The Policy shall automatically and immediately terminate on the earlier occurrence of any of the following events –

- On foreclosure of the Policy

- On the date of receipt of intimation of death of the Life Assured, unless Settlement option has opted for.

- On payment of Discontinuance Value or Surrender Benefit.

- The Maturity Date, unless the Policyholder has opted for the Settlement Option.

- The expiry of the Settlement period, if opted.

- On cancellation of Policy during Free look period.

Is there any grace period in the policy?

This policy has a grace period of 30 days for yearly, half-yearly & quarterly Premium payment frequency and 15 days for monthly Premium payment frequency from the due date of Regular Premium payment, without any late fee, during which time the Policy is considered to be in-force with the risk cover without any interruption as per the Policy terms and conditions.

Can I cancel the policy if I didn’t like its terms and conditions?

If the policyholder doesn’t like the terms and conditions of the policy, then they can cancel and return the policy with its original document within 15 days and 30 days (in case the policy is purchased through distance marketing) from purchasing the policy. This period is known as the Free-Look Period.

On receiving the policy, the Company shall send the policyholder a refund comprising of the Premium Allocation Charge plus charges levied by cancellation of Units plus Fund Value, at the date of cancellation of units less the proportionate risk premium for the period the Life Assured was on the cover, expenses incurred on medical examination and stamp duty charges.

Exclusion Under the Policy –

a) Suicide Exclusion –

In case of death due to suicide within 12 months from the date of commencement of the Policy or from the date of the latest revival of the Policy, the nominee or beneficiary of the Policyholder shall be entitled to fund value, as available on the date of intimation of death. Any charges other than FMC or guarantee charge recovered subsequent to the date of death shall be added to the fund value as at the date of intimation of death.

b) Accidental Permanent Total Disability Exclusion –

The accidental disability benefit will not be payable in the following situations –

- Disability as a result of the insured person committing any breach of law with criminal intent;

- Disability of insured person as a result of war, invasion, civil war, rebellion or riot;

- Disability as a consequence of the insured person being under the influence of alcohol or drugs other than drugs prescribed by and taken in accordance with the directions of a registered medical practitioner;

- Disability as a result of the insured person taking part in any naval, military or air force operation;

- Disability as a result of the insured person participating in or training for any dangerous or hazardous sport or competition or riding or driving in any form of race or competition;

- Disability of insured person as a result of aviation, gliding or any form of aerial flight other than as a fare-paying passenger on a civilian airline plying on regular routes and according to a scheduled timetable;

- Disability of insured person as a result of attempted self-injury whilst sane or insane

- Disability of insured person as a result of poison, gas or fume (voluntary or involuntarily, accidentally or otherwise taken, administered, absorbed, or inhaled.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.