Aditya Birla Sun Life Insurance Vision Life Income Plan – Review, Features and Benefits

In today’s world, we try to plan for all of life’s important stages and milestones keeping in mind our growing responsibilities. And, to supplement these efforts, we sometimes wish for an extra source of regular income.

The “Aditya Birla Sun Life Insurance Vision Life Income Plan”, is a traditional participating whole life plan that helps you to not only plan your financial goals but also realize your dreams by providing you with a steady income and whole life cover.

With survival benefits payable every year from the end of the premium paying term till maturity and a life insurance benefit, this plan offers a perfect blend of income and financial protection for you and your family.

Features of this Policy –

- Regular Income – 5% of the Sum Assured guaranteed plus bonus every year after premium paying term

- Whole Life Cover – Comprehensive financial protection for your family with whole life covers till age 100

- Enhanced protection – Access to suitable Rider options for added protection, at a nominal extra cost

- Tax Benefits on the premium paid as per sec 80 C | 10 (10) D and 80 D

Benefits of this Policy –

a) Death Benefit –

In the unfortunate event of the death of the life insured during the premium paying term, the company shall pay to the nominee the following –

- Sum Assured on Death; plus

- Accrued bonuses as on date of death; plus

- Terminal bonus (if any)

In the event the life insured dies after the premium paying term, the company shall pay to the nominee the following –

- Sum Assured on Death; plus

- Bonus from the last policy year; plus

- Terminal bonus (if any)

The Sum Assured on Death is the maximum of the following –

- 10 times the Annualized Premium

- Sum Assured chosen;

- 105% of Total Premiums paid up to the date of death

The annualized premium shall be the premium amount payable in a year chosen by the policyholder, excluding the taxes, rider premiums, underwriting extra premiums, and loadings for modal premiums, if any.

Total Premiums Paid means a total of all the premiums received, excluding any extra premium, any rider premium, and taxes.

In the case where the death of the Life Insured takes place prior to the risk commencement date, only the total premiums paid to date (excluding GST, if any ) shall be payable as the Death Benefit.

In case of death of the life insured, if the life insured is different from the policyholder, the policyholder will receive the death benefit. The policy shall be terminated once the death or maturity benefit is paid and no other benefit shall be payable thereafter.

b) Survival Benefit –

In the event Life Insured survives to the end of premium paying term, the company shall pay to you accrued bonuses to date. Your Policy Schedule shows the Income Benefit applicable to your policy.

Starting from Policy Anniversary subsequent to the end of the premium paying term and on every Policy Anniversary thereafter till maturity you shall receive –

- Income Benefit of 5.0% of Sum Assured; plus

- Bonus from the last Policy Year

c) Maturity Benefit –

On the policy maturity date, the company shall pay the insured –

- Higher of, Sum Assured or 105% of total premiums paid to date excluding premiums paid towards underwriting extra and any attached riders; plus

- Terminal bonus (if any)

d) Surrender Benefit –

The policy will acquire a surrender value after all due Installment Premium for at least two Policy Years have been paid in full. After the policy has acquired a surrender value, the insured can request to surrender the policy for its Surrender Benefit.

The Guaranteed Surrender Value is the percentage of Total Premiums paid and surrender value of accrued bonuses less any survival benefit already paid. Your surrender benefit is the higher of the following –

- Guaranteed Surrender Value; or

- Special Surrender Value

e) Rider Benefit –

If the insured wants some added protection, then this policy can be enhanced by the following riders for a nominal extra cost –

- ABSLI Accidental Death and Disability Rider

- ABSLI Critical Illness Rider

- ABSLI Surgical Care Rider

- ABSLI Hospital Care Rider

- ABSLI Waiver of Premium Rider

- ABSLI Accidental Death Benefit Rider Plus

f) Bonuses –

The company will declare simple reversionary bonuses regularly at the end of each financial year and those will be accrued in the policy on its policy anniversary, surrender, or on death. Bonuses once attached to the policy are payable along with the interim bonuses, as applicable to death, surrender, or survival.

In case of surrender, the surrender value of the attached bonuses will be payable. The regular bonus rate declared by the company may vary from year to year and will depend on the actual experience regarding various factors and the prevailing economic conditions. Future bonuses are however not guaranteed and will depend upon the future profits of the participating business.

Terminal bonus – The company may also pay a terminal bonus at the company’s discretion on death, or maturity, based on the actual experience and the prevailing economic conditions.

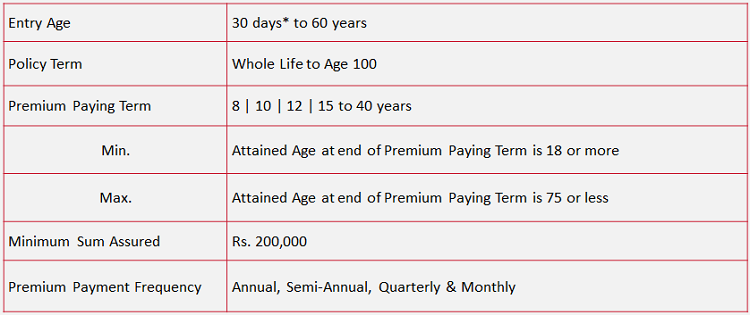

Eligibility Conditions of the Policy –

Can I cancel the policy if I didn’t like its terms and conditions?

The policyholder has the right to return their policy to the company within 15 days (30 days in case the policy issued under Distance Marketing) from the date of receipt of the policy. This period is known as the Free Look Period.

The company will refund the premium paid once they receive a written notice of cancellation (along with reasons thereof) together with the original policy documents.

The company will further deduct the proportionate risk premium for the period of cover and expenses incurred by the company on medical examination and stamp duty charges while issuing the policy.

Can I take Loan against this policy?

The insured is eligible to take a loan against their policy at any time after their policy acquires a surrender value. The minimum policy loan is Rs. 5,000 and the maximum is 85% of the then Surrender Benefit less any outstanding policy loan balance as of date.

Your outstanding policy loan balance on any date shall equal all policy loans made to date, including accrued and unpaid interest thereon, less any policy loan repayments you have made to date. The interest charged by the company on any outstanding policy loan balance accrues on a daily basis.

The insured is free to repay all or part of your outstanding policy loan balance at any time. If your policy is in reduced paid-up status and your outstanding policy loan balance equals or exceeds the Surrender Benefit then on that date, all benefits under your policy will cease immediately and policy will terminate.

Any benefit payable under this policy will first be reduced by any outstanding policy loan balance at that time and only the residual value will be paid to you or your Nominee as the case may be.

Is there any revival period in the policy?

To revive the policy, the insured must pay all unpaid Installment Premium due to date plus interest thereon and repay any outstanding policy loan balance plus interest thereon.

The insured can revive the policy for its full coverage within five years from the due date of the first unpaid premium by paying all outstanding premiums together with interest as declared by the company from time to time and by providing evidence of insurability satisfactory to us. Upon revival, your benefits shall be restored to their full value.

Is there any premium discontinuance in the policy?

If the insured is unable to pay the Installment Premium by the due date, they will be given a grace period of 30 days during which time all benefits under the policy will continue.

a) Until two (2) full years Installment Premium are paid –

If the company does not receive the entire Installment Premium by the end of the grace period, this policy will be deemed lapsed and all benefits will cease immediately. The lapse date is the date the first unpaid Installment Premium was due. The insured will be given a period of five years from the lapse date to revive your policy.

b) Once two (2) full years Installment Premium have been paid –

If the company does not receive the entire Installment Premium by the end of the grace period, this policy will be deemed paid-up, and benefits will continue as per the Policy Paid-Up provision. The paid-up date is the date the unpaid Installment Premium was due. The insured will be given a period of five years from the paid-up date to revive the policy for its full benefit.

When can my policy terminate?

Your policy will terminate at the earliest of the following –

- The date of settlement of the Death Benefit; or

- The date of payment of the surrender value, if any; or

- The policy maturity date; or

- The date on which the Revival Period ends after your policy has lapsed as per Premium Discontinuance provision; or

- The date when outstanding loan value exceeds the surrender benefit for reduced paid-up policy.

Exclusion under the policy –

- Suicide Exclusion –

In case of death of Life Insured due to suicide within 12 months from the date of commencement of risk under the policy or from the date of Revival of the policy, as applicable, the amount described in the Death Benefit provision will not be payable.

In such circumstances, the company shall refund the premiums paid since Date of Inception of the policy till the date of death(excluding applicable taxes)or the company shall pay the Surrender Value available as on the date of death, whichever is higher to the Nominee or beneficiary of the Policyholder, provided the policy is in force or active.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.

hi, I have paid 1,25000 till yet. I want to cancel my policy as it is not worthful it seems. So let me know wht will be lose and profit?

You need to check this with Birla!

I HAVE PAID Rs 246988 IN 5 INSTALLMENTS STARTING FROM DECEMBER 2016.

IF I SURRENDER MY POLICY TODAY , WHAT WOULD BE THE DEDUCTIONS AND THE FINAL AMOUNT WHICH WOULD BE PAYABLE

Check out the policy document once.. I guess you shall get less than you have paid, the exact numbers can come only from company side!

Manish