Aditya Birla Sun Life Insurance Life Shield Plan – Review, Features and Benefits

Protection needs differ from one family to another. There is no one in all policy which will be the same for everyone. Be it joint life protection with your spouse, increasing or decreasing term assurance option, waiver of premium benefit in case of total permanent disability or critical illness on the return of premium option, you need a policy that delivers future security for your family in the way you prefer.

Aditya Birla Sun Life Insurance has come up with Term Plan named ” Aditya Birla Sun Life Insurance (ABSLI) Life Shield Plan” which offers you the flexibility to make a combination from amongst 8 different plan options as per your family’s needs so they need not compromise on their lifestyle, even in your absence.

Features of this Policy –

- Multiple options to suit your different protection needs

- There is no loan facility in this policy

- This policy offers tax benefits under Section 80C and Section 10(10D) of the Income Tax Act, 1961.

- Option to enhance coverage at key milestones of your life

- Option to cover your spouse under the same policy

- Return of premium under option 7 & 8

- Inbuilt Terminal Illness Benefit

- Multiple options to receive Death Benefit

- Additional Rider Benefit

Plan Option of the Policy –

- The premium will vary depending on the plan option chosen by you. The plan option once selected cannot be changed during the policy term.

- In case of rider benefits, if opted for, shall be payable as per rider sum assured chosen at inception.

- # excluding loadings for modal premiums, applicable taxes, any applicable rider premiums, and underwriting extras, if any.

- ^ Refer product brochure of Critical Illness and Total Permanent Disability definition and exclusions in details

| Option 1 |

Level Term Assurance – Sum Assured chosen by you will remain constant for the entire policy term. |

| Option 2 |

Level Term Assurance with Waiver of Premium (WOP) Benefits – In addition to benefit applicable for Option 1, in case you are diagnosed with Critical Illness^ or Total and Permanent Disability^ whichever is earlier, all future premiums if any, will be waived off and policy will continue till the end of the policy term. |

| Option 3 |

Increasing Term Assurance – You can choose to enhance your sum assured at inception by 5% / 10% per annum. (simple) as per your needs. Every year, your sum assured will increase by 5% / 10% p.a. (simple) of the original sum assured without any increase in your premium amount. |

| Option 4 |

Increasing Term Assurance with Waiver of Premium (WOP) Benefits – In addition to benefits applicable for Option 3, in case you are diagnosed with Critical Illness^ or Total Permanent Disability^ whichever is earlier, all future premiums if any, will be waived off and policy will continue till the end of the policy term. |

| Option 5 |

Decreasing Term Assurance – An option designed to take care of your protection needs owing to any loan or mortgage taken by you. Refer to the product brochure for details on death benefit under this option. |

| Option 6 |

Decreasing Term Assurance with Waiver of Premium (WOP) Benefits – In addition to benefits applicable for Option 5, in case you are diagnosed with Critical Illness^ or Total Permanent Disability^ whichever is earlier, all future premiums if any, will be waived off and policy will continue till the end of the policy term. |

| Option 7 |

Return of Premium – Sum Assured chosen by you will remain constant for the entire policy term. If the life insured survives till maturity date, we shall return all the premiums paid #. |

| Option 8 |

Return of Premium with Waiver of Premium (WOP) Benefit – In addition to benefits applicable for Option 7, in case you are diagnosed with Critical Illness^ or Total Permanent Disability^ whichever is earlier, all future premiums if any, will be waived off and policy will continue till the end of the policy term. |

Benefits of the Policy –

a) Death Benefit –

In case of the unfortunate demise of the life insured during the Policy Term, Death Benefit will be paid to the nominee. Death Benefit is the Sum Assured on deathless any previously paid Terminal Illness Benefit. The policy shall be terminated once the Death Benefit is paid.

Sum Assured on death for regular | limited pay will be highest of –

- 10 times of the Annualised premium for all ages; or

- 105% of all the Total Premiums paid as on the date of death; or

- Absolute amount assured to be paid on death

Sum Assured on death for single pay will be the highest of –

- 125% of the single premium for all ages; or

- Absolute amount assured to be paid on death

The annualized premium shall be the premium amount payable in a year chosen by the policyholder, excluding the taxes, rider premiums, underwriting extra premiums and loadings for modal premiums, if any.

Total Premiums paid means total of all the premiums received, excluding any extra premium, any rider premium, and taxes.

b) Maturity Benefit –

In the event the life insured survives to the end of the Policy Term, no benefit is payable on maturity except when the Return of Premium Plan Option 7 | 8 is chosen and then the sum of all the premiums (excluding GST, premiums paid towards underwriting extras and/or riders as may be applicable) shall be paid on the policy maturity date and the policy will be terminated thereafter.

c) Terminal Illness Benefit –

In case the life insured is diagnosed with a Terminal Illness, 50% of the applicable Sum Assured on death, subject to a maximum of Rs. 2.5 crore, will be paid immediately and all future due premiums are waived off. On subsequent death of the life insured during the Policy Term, the Sum Assured on death shall be reduced by the amount of Terminal Illness Benefit already paid. Future due premiums are not liable to be paid on their premium due dates.

Terminal Illness Benefit shall only be payable on the first diagnosis of any Terminal Illness of the life insured during the Policy Term.

d) Waiver of premium and on Total and Permanent Disability (TPD) –

In case of the life insured suffering from Total and Permanent Disability during the Policy Term described later in detail, all future premiums, if any, will be waived off. Death Benefit under the policy will remain unaffected.

e) Waiver of Premium on Critical Illness (CI) –

In case of the life insured suffering from any of the specified Critical Illness during the Policy Term described later in detail, all future premiums if any will be waived off. Death Benefit under the policy will remain unaffected.

The premium waiver on TPD or CI is applicable only if you have chosen Plan Option 2, 4, 6 or 8. Premium waiver benefit is applicable to the first occurrence of either TPD or Critical Illness whichever is earlier. This benefit is applicable only once during the entire Policy Term.

f) Joint Protection Life –

Under this option, two lives, i.e., you (primary life insured) and your spouse (secondary life insured) are covered under the same policy. The Sum Assured applicable for your spouse shall be equal to 50% of your applicable Sum Assured. This option shall only be available where the Sum Assured of primary life insured is greater than or equal to Rs. 50,00,000.

You can opt for Joint Life Protection for only if Plan Option 1, 2, 3 or 4 is chosen. You can opt for this option at the inception of the policy and the same shall not be changed subsequently. No rider can be chosen under this option.

In case of death of the primary life insured prior to the secondary life insured, Sum Assured on death for primary life insured will be paid to the spouse (secondary life insured) and the life cover for secondary life insured will continue with the future premiums, if any, waived off. Then on the death of secondary life insured, before the policy maturity date, Sum Assured in respect of secondary life insured will be paid to the nominee and policy will be terminated.

In case of death of secondary life insured prior to primary life insured, Sum Assured in respect of secondary life insured will be paid to the primary life insured. Future premiums, if any, will be reduced from the next policy anniversary to the premium that would have been charged at inception for only primary life insured at policy inception. Then on the death of the primary life insured, before the policy maturity date, the Sum Assured on death in respect of primary life insured will be paid to the nominee and the policy will be terminated.

If the case of death of both the lives simultaneously the Sum Assured on death in respect of the primary life insured as well as Sum Assured in respect of secondary life insured will be paid to the nominee and the policy will be terminated.

Once the Joint Life Protection is chosen, you cannot discontinue the coverage of the particular life, unless it is due to the events as mentioned above.

The Terminal Illness Benefit as explained in the Death Benefits section shall be applicable in respect of both, i.e., the primary life insured and the secondary life insured.

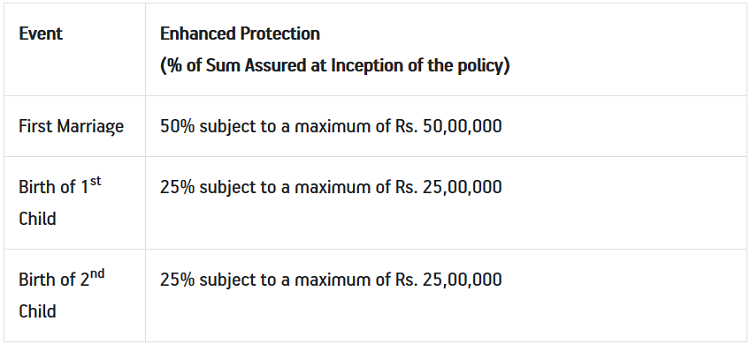

g) Enhanced Life stage Protection –

Your protection need varies at different life stages owing to the occurrence of joyous events such as marriage and birth of children. You may opt to increase your life cover on the occurrence of each of the events without undergoing any fresh medical examination.

This feature is available only for policy under Plan Option 1 and Option 2, standard life at the inception of the policy, regular pay policy and the attained age of life insured is less than or equal to 50 years while exercising this option.

This option is not available if Joint Life Protection is chosen. Future premiums shall be considered at the premium rate as applicable to the age at the inception of the policy. Future premiums shall be increased in the proportion of the increase in the Sum Assured to the Sum Assured at the inception of the policy and will be reflected from the subsequent policy anniversary.

The details of Enhanced Lifestage Protection are mentioned below –

You can choose to reduce the Sum Assured in the future to the extent of Sum Assured increased under the Enhanced Lifestage Protection option. The reduction in Sum Assured will be effective from the policy anniversary falling immediately after the date of notification and the premium will be decreased at the same time.

Any increase in Sum Assured due to your first marriage, the birth of a first child or second child under this option may be subsequently reduced subject to the written request. The premium shall be decreased by the same amount as the premium was increased while exercising the Enhanced Lifestage Protection option.

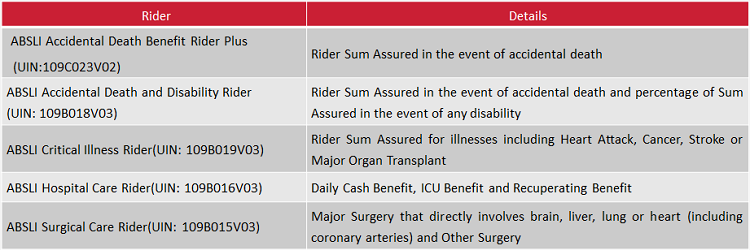

h) Customizable Benefit –

Insurance cover can be enhanced during the premium paying term by adding any one of the following riders –

Riders are not available for Joint Life Protection Option & Decreasing Term Assurance (Plan Option 5|6).

The policyholder can only opt for either ABSLI Accidental Death and Disability Rider or ABSLI Accidental Death Benefit Rider Plus, not both.

Eligibility Conditions of the Policy –

| Entry Age (age last birthday) |

18 to 65 years |

| Maximum Maturity Age |

80 years |

| Policy Term |

Minimum

• For Plan Option: 1 | 2 | 3 | 4 | 5 | 6 – 10 years Maximum • 50 years |

| Premium Paying Term | Single Pay | Limited Pay – 6, 8 Years | Regular Pay |

| Premium Mode | Annual | Semi-annual | Quarterly | Monthly |

| Sum Assured |

|

Is there any grace period in this policy?

Yes, a grace period of 30 days will be given if you are unable to pay your premium by the due date. During this grace period, all coverage under your policy will continue.

a) If Plan Option 1 or 2 or 3 or 4 or 5 or 6 is chosen then –

- Regular Pay – If you do not pay your premium within the grace period, your policy will lapse, and all benefits will cease immediately.

- Limited pay – If you have not paid premiums for four full policy years, at the end of grace period of 30 days, the policy will lapse and all benefits will cease immediately and If you have paid premiums for at least four full policy years and any subsequent premium is not paid, then on the expiry of the grace period, the policy will continue on the reduced paid-up basis.

b) If Plan Option 7 or 8 is chosen then –

- Limited pay – If you have not paid premiums for four full policy years, at the end of grace period of 30 days, the policy will lapse and all benefits will cease immediately and If you have paid premiums for at least four full policy years and any subsequent premium is not paid, then on the expiry of the grace period, the policy will continue on the reduced paid-up basis.

Is there any possibility where I can revive my policy?

Yes, there is a possibility where you can revive your policy for its full coverage within five years from the due date of the first unpaid premium by paying all outstanding premiums together with interest as declared by the company from time to time and by providing evidence of insurability satisfactory to us. The policy can be revived only during the revival period.

Is there any Paid-Up benefit in the policy?

a) If Plan Option 1 or 2 or3 or 4 or 5 or 6 is chosen –

- For Regular Pay – Not applicable

- For Limited Pay – If you choose to stop paying premiums after all due Installment Premiums for at least four policy years have been paid then this policy will continue on a paid-up basis.

b) If Plan Option 7 or 8 is chosen –

- If you choose to stop paying premiums after all due Installment Premiums for at least two full policy years have been paid then this policy will continue on a paid-up basis.

Is there any surrender value of our policy?

a) If Plan Option 1 or 2 or 3 or 4 or 5 or 6 is chosen –

- There is no surrender benefit payable for regular pay under this plan. However, for limited pay, your policy will acquire a surrender value are all due premiums for at least four full policy years are paid and for single pay immediately are policy issuance.

b) If Plan Option 7 or 8 is chosen –

- Your policy will acquire a surrender value are all due premiums for at least two years are paid for regular or limited pay and immediately are policy issuance for single pay.

Can I return the policy if I didn’t like the terms and conditions of the policy?

Yes, the policy can be returned to the company within 15 days (30 days in case the policy issued under the provisions of IRDAI Guidelines on Distance Marketing(2) of Insurance products) from the date of receipt of the policy.

The company will refund the premium paid once they receive your written notice of cancellation (along with reasons thereof) together with the original policy documents.

The company will further deduct the proportionate risk premium for the period of cover and expenses incurred by us on medical examination and stamp duty charges while issuing your policy.

Exclusions under the policy –

Exclusions under this policy are under various heads. Let us see them one by one –

a) Suicide Exclusion –

The company will pay the premiums paid to date (excluding applicable taxes) or surrender value, if higher in the event the life insured dies by committing suicide, within twelve months from the inception of the policy or revival date of the policy respectively, provided the policy is in force.

For Joint Life Protection, the suicide exclusion described above applies in the event of an earlier death of either the Prima Life Insured or the Secondary Life Insured and the life cover as mentioned in the Joint Life Protection section shall continue for the surviving Life Insured subject to the payment of reduced future premiums if any.

b) Total Permanent Disability and Critical Illness Benefit Exclusion –

The following exclusions are applicable only for Waiver of Premium benefit in case of diagnosis of Total Permanent Disability and/or Critical Illness.

The policyholder will be entitled to receive the benefit of Total Permanent Disability or a covered Critical Illness results either directly or indirectly from any one of the following causes listed in the exceptions below –

1. Any Pre-Existing Disease. “Pre-existing Disease” means any condition, ailment, injury or disease –

- That is/are diagnosed by a physician within 48 months prior to the effective date of the policy issued by the insurer or its latest revival date; OR

- For which medical advice or treatment was recommended by, or received from, a physician within 48 months prior to the effective date of the policy or its latest revival date, whichever is later; OR

- A condition for which any symptoms and/or signs if presented and have resulted within three months of the issuance of the policy or its latest revival date in a diagnostic illness or medical condition.

This exclusion will not be applicable to conditions, ailments or injuries or related condition(s) which are underwritten and accepted by an insurer at inception

2. Any sickness-related condition manifesting itself within 90 days from the policy commencement date or its latest revival date, whichever is later.

3. AIDS and/or HIV related complications or any sexually transmitted diseases

4. Suicide or attempted suicide or self-inflicted injury , irrespective of mental condition

5. Participation in a criminal, unlawful or illegal activity, etc….

c) Additional Total Permanent Disability Benefit Exclusion –

In addition to the common exclusions above, the policyholder shall be entitled to receive the benefits of the Total Permanent Disability results either directly or indirectly from –

- Engaging in or taking part in professional sport(s) or any hazardous pursuits, including but not limited to, diving or riding or any kind of race, underwater activities involving the use of breathing apparatus or not, martial arts, hunting, mountaineering, parachuting, bungee jumping.

d) Terminal Illness Benefit Exclusion –

The Life Insured will not be entitled to any Terminal Illness benefit if it is caused directly or indirectly due to or occasioned, accelerated or aggravated by intentional self-inflicted injury or attempted suicide, whether medically sane or insane.

Conclusion –

So, by now you know each and every important detail about this policy. Do let me know if I have missed any important points in the comment section. Please feel free to ask any doubts regarding this policy.