Post Office Monthly Income Scheme (POMIS) – How it works and Rules

POSTED BY ON January 31, 2011 COMMENTS (388)

Are you looking for a safe option to invest your money and earn decent returns? If yes, then I can explore one of the post office schemes. Today, we look at post office monthly income schemes (POMIS) which are not that well-known among urban investors. We often look to fixed deposits and other debt options to park our money or generated monthly income. But the monthly income scheme post office offers myriad possibilities. Let’s explore!

Post Office Monthly Income Account

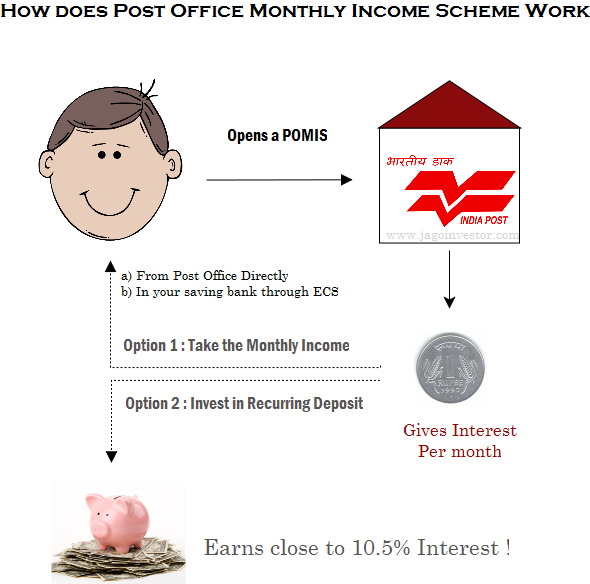

Post Office Monthly Income Scheme is one of the post office schemes which gives you a guaranteed return on your investment. Anyone who wants to generate a monthly income can open this account and get an assured monthly income. You get an 8% interest per year, which is payable on a per month basis. You will get the interest each month from the date of making the investment, not from the start of the month.

For example Ajay invests Rs 4.5 lacs in the post office monthly income scheme. His interest per year is Rs 36,000 @8%, hence he gets Rs 3,000 per month as income. If you do not withdraw the amount for some month, it would not earn any interest and just lie in the account.

This post office saving scheme does not come under sec 80C so there is no tax-exemption for the amount you invest in this, and interest income is taxable, but there is no TDS cut in this scheme. Read 7 Tax saving Tips

You can deposit the money in the POMIS with cash, demand draft or local cheque. Once you open a monthly income scheme account, you will be issued a scheme certificate and a passbook to record the transactions against the post office MIS scheme. The maturity period of this scheme is 6 years. You will also be eligible for a 5% bonus if you retain your scheme foe 6 years, so eventually, your overall return including this bonus can turn out to be around 8.9 %. There is a limit on the amount you can invest in POMIS. It’s limited to Rs 4.5 lacs for a single account and 9 lacs for a joint account. You can have any number of accounts, but within the overall upper limit. There is no compulsion to take your money out after maturity, you can leave the money in the account, but then it would earn the interest equal to saving bank account for the next 2 years only.

Getting Interest income in your Saving account

You get to withdraw the POMIS income amount by directly going to the Post-office. However, there seems to be a bit of confusion, if you want the income in your savings bank account. According to per some resources, you can get it credited to your savings bank account, provided it’s in the same post-office. But elsewhere, some guys confirm that you can provide ECS information at the time of opening the account and get the interest amount created in your Bank account (see the list of cities covered by Post-office). I found the comment below on this website, where a user claims of using ECS.

YES! you can opt for a ECS facility whereby your monthly interest amount will be credited to any savings account of your choice (here HDFC). After you open the POMIS account, you need to fill up the ECS form, attach a blank cheque of your HDFC savings account and you’re all set. You don’t need to open a Savings account at the Post office just for credit of monthly interest.

The information I’ve given here is authentic, because I’m personally using the ECS facility.

Pre-mature Withdrawal from Post-Office monthly Saving Scheme

Even though the maturity period for POMIS is 6 yrs , there is a facility to break it and take your money out. However you can take your money only after 1 year. You have to pay some penalty which is as follows

- If you break it within 1-3 yrs: 2% penalty on Deposit amount

- If you break it after 3 yrs: 1% penalty on Deposit amount

Example: If you deposit Rs 1 lac in POMIS , and want to take money out in 2nd year, you will have to bear the penalty of 2,000 and you will get back 98,000. If you take money out in 5th year, you get 99,000.

Confusion of returns by mixing POMIS along with RD?

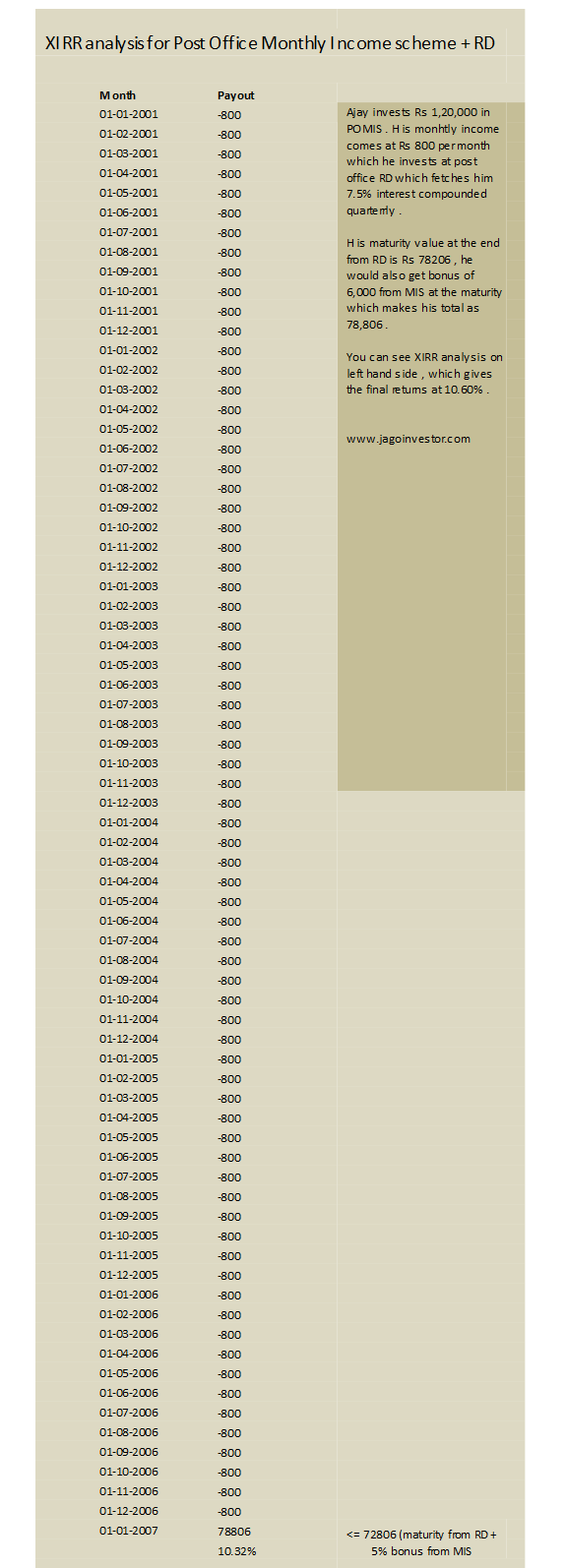

There are some claims which say one can invest the monthly income coming from Post office monthly income scheme into the Post office RD and earn a return of 10.5 %. This at first looks amazing, but its kind of untrue and marketing gimmick. I did a XIRR analysis of the whole cash flows and found out that considering everything , your final and actual return is just 8.77% , which means that when you invest your money in POMIS , direct all the monthly income to an RD and at the end when you get the maturity amount along with the bonus of 5 %, in total you have made an annual return of just 8.77%, which is quite ok considering the safety and conservativeness of the product. But considering the tax to be paid at the end of the tenure, again you might not get great Real Returns! , Remember that the RD comes for the 5 yrs, but it can be extended for 1 more year and it can be made for 6 yrs.

However, the Post office website claims that you earn 10.5% when you put your monthly income into an RD, which is just to attract investors and not give a complete picture. This 10.5% figure is actually only after considering the bonus amount you get at the end, If you remove the Bonus of 5% from the scene , then the return drops to 7.92% . In the below example, you can see that a person who has invested Rs 1,20,000 will get Rs 800 as monthly income , and he gets 72808 as maturity amount from RD, 1,20,000 back as the initial investment and 6,000 as bonus amount .

Scene 1 : If you consider the 800 payment per month in RD for 6 yrs and the maturity amount of 72,806 at the end of 6 yrs , then the returns are just 7.92% (XIRR)

Scene 2 : If you consider scene 1 along with the Bonus amount also , which means you get 72,806 + 6,000 Bonus also = Rs 78,806 , in that case your returns are 10.32% , but its misleading as this bonus is the cost of your 1,20,000 getting stuck at one place for 6 yrs and not an RD feature . So this is not the right way of looking at it . (See chart above)

In case of scene 2 into consideration , then the return from “Only POMIS” is just 8% , but if you consider POMIS + Bonus only then its 8.91% .

Note that this setup operates automatically, you have to set up this once and then no more overseeing. It will happen automatically each month (official link)

Other Features of Post Office Monthly Income Scheme

- A minor above age 10 years can open an account on his/her own name directly. There is a limit of 3 lacs for guardian and it would not be clubbed with guardian limit (More on Clubbing rules)

- Non-Resident Indian / HUF cannot open the Account.

- Interest not withdrawn does not carry any interest.

- Your POMIS account can be transferred from one post office to any Post office in India free of cost.

- The amount deposited in POMIS is exempt from Wealth Tax

Nomination

You have to make the nomination for your Post office monthly Income scheme at the time of applying, however, if you don’t do it at the time of opening, you can also do the nomination later. Incase of the death of the account holder the money will be paid to the nominee. Read more on nomination here.

I have invested some amount in POMIS and it is matured on 01/01/2016. But as I am currently not in India, I did not claim it yet. What happens now? Does PO auto renewels or PO pays with interest whenever I actuallly withdraw or there is no extra interest post maturity date? Could you clarify.

I am not sure on that, but I dont think its on auto renewal. It will be kept in an account which will not grow

There are two dates written on my India post MIS pass book. One is Registration Date : 27/11/2010 and another one is Issue Date : 02/12/2010. It is a 6 year plan, hence it is going to be matured in this year that is 2016. I am confused about the maturity date, is it 27/11/2016 or 02/12/2016 ? Will be extremely helpful if you can help.

Hi Abhishek S.

Thanks for asking your question. However, I dont think I am eligible to answer your query as its either out of scope of my knowledge or its not related to money matter directly

Manish

I have 1.5 lakh , can i deposit in MIS and what is the monthly income

You need to check it with them only

Sir, If I open MIS A/C , Can I withdraw the interest amount per month

Yes

Above 9 lac can be invested by a jointly senior citizen ?

I am planning to invest In MIS scheme …as we are 3 members and each holding a pan card …and I want to invest 4.5 lacs each !so do I need to pay income tax ?

Income tax is paid on INCOME ! .. Not on investment.

Agar mein 4.5 lac ka mis karta hoon to tax dena parega keya?

Yes

Sir

I have 3nos. of MIS of 14 lakhs. But the Post master does not issue RD. Now I want to transfer the interest amount from MIS to RD. Is it possible. if, how ?

Hi MihirSarkar

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

Agar me 4.5L MIS ka scheme karna chahta hu to kya mujhe imcometax varna padega?

Hi sir,

I invest 100000 in mis in 2013

I want this money

Can i get my money in 2016 ????

Yes, you can withdraw it. Please talk to them

I m planning for MIS. Some one already having MIS told me that bonus facility no more available now.

Is it so ?

Rgds

Thats correct

Sinior citezen ke liye MIS limit kya hai ?

9 lacs

Mene mis a/C open kiya hai jisme pese 9 date ko kat gaye the par koi wazah se a/c opning me deri ho gai hai to post master mis ki date ajki laga raha hai to mere ko janna hai ki mere ko per month intrest konsi date ko molega ???

we are 3 in the family all are holding pan i want to invest in mis scheme of post office with all the thee as a joint holders invest will be like this 450000/-*3 ac which will be 1350000/- where there would not be exceed in limit and if one person diesthe other 2 can close one ac and continue the other 2 ac which comes to 9 lakhs 450000*2 whether that is possible.please explan

No , the maximum one can have is joint account with 2 people . Thats all

Hi

Is it advisable to do POMIS of 9 Lakhs (joint) and put monthly income into ongoing exisitng SIP portfolio of diversified equity MFs.

Thanks

Yes you can do that, This way your principle will be intact. But then how is it helping you ? I mean return wise !

Thanks much for the useful article!

A query: My PPF investment already covers the max limit of 150000 in Section 80C. Now, if I invest in MIS and arrange for the MIS interest to be invested in a PO RD a/c, isn’t it true that both the MIS interest and the RD interest are taxable? ?

Yes, both of them will be taxable !

can i deposit in mis scheme with my huf pan number

then it will be in HUF name !

I HAVE A MIP DONE AT MEERUT POST OFFICE AND NOW AS IT IS MATURED I HAVE TO REDEEM IT,BUT PRESENTLY I AM IN LUCKNOW,CAN I REDEEM IT IN LKO ITSELF

PLS ADVICE

You need to visit the branch I guess!

Hi Manish G,

can you explain what is the rule of Interest, after death of a join account holder,in MIS.

is it true ? no interest will be paid after such period by PO after the death of any one in both account holder ?

Regards,

Kailash

I am not sure on this, but it looks like that rule cant be there. I suggest using RTI to get the right answer !

Hi Manish ,

What is the rule? in case of death (,Monthly interest scheme )

Please check it with the post office itself !

if i deposit 1200000 amount . i want interest every 3 months sir, how much amount did i get …any tax problem..which documents should i submit sir,…did it was single or joint

Hi kotesh

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

Dear sir ,

I invested Rs 300000/- in MIS in 2011. The interest accrued each month will be 2100 or 1950?

Hi dillu

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

Dear sir,

In case of dispute between joint holders of MIS Joint B, what are the rules and regulations, please tell mee.

What dispute ?

please tell me the process of transfering the MIS account from one post office to another.

I am not sure on this

from 1. 4. 2016 the interest rate is 7.80 %

? is that so?

The current interest rates will apply .

hello sir,

is pan card mandatory for opening mis for second holder.as i want to open it with my daughter i have pan card but my daughter is not.kindly enlighten

Hi shailly

Thanks for asking your question. However, I dont think I am eligible to answer your query as its either out of scope of my knowledge or its not related to money matter directly

Manish

Hi sir I m Nutan , my mother opened mis of 2 lakhs in chandimandir post office n transfer it from chandimandircantt post office to thanabihpur post office on Oct 15 now every month my mother went to post office for transferred book. Post office man denied that book not receives here

Next month mis will matured. Pl help me what we will do. Post man also refused to talked to us. They say I called u to come n transfer your account from here. I will not do any thing go from here. My mother is illiterate. Pl help me sir.

Hi nutan

I suggest that you now take the RTI route. You can file the RTI and ask your queries to them. THey are bound to reply you on your queries.

Its a bit long cut, but works well

Manish

I open AC in POMIS with 2 lack & my joining date is after 01/05/2016.how many interest I take

Hi VILASCHANDRA

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

I Mr Santosh if I deposited 100000 how many rs will return me monthly

5,000

Hello Manish Ji,

I want to open POMIS with 3lakh rupees and want inetrest in my Sukanya Samridhi Yojna A/C which is operating in Bank of Baroda. Is this possible?

Kripya ye bhi bataiye ki intrest ko SSY me deposit karna better rahe ya India Post ke R/D account me?

I want to do all saving for my daughter.

Thank you

I dont think its possible

Sir,is it the upper limit of RS 450000 per account or after accumulation of all MIS accounts?

Also,is there any upper limit for FD in post office?

Please advise.

Thanks and regards.

All the MIs accounts !

Cosmos co oprative bank MIS scheme 9.25%

Intrest credited monthly.. + saving account 4% intrest rate

good one

Hello Manishji

I want to know that a minor of age 12 can open a account without a guardian name and if a guardian is compulsory then this amount will be included in guardian’s investment.

Hi purnima

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

MIS with ECS facility has been operating since last 5 yrs, but in january 16 the interest is not credited in Bank. Bank can not tell the reason. Can you tell if this could be due to sudden revising of maturity period from 6 yrs to 5 yrs.

Please visit Post Office where your MIS is and you need to Physically give the Withdrwal SB-7 form and get Cash of your monthly interest. I faced the same problem last year for 3 months. Its due to their upgradation of Core Banking Facility so ECS not working !!

Hi AKDas

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

My aged mother has been having MIS account in Basavanagudi HPO, Bangalore for so many years. All these years one of her children used to go and collect interest in cash. Now Post office is forcing my mother to open a savings account only for interest. It should be vo,untary. Why force us?

Moreover she already has a bank account to which her goverment pension gets credited. When we wanted to opt for ECS post office employees refuse to allow whereas on tneir web site it says it is allowed.

First of all employees do not turn up till 9.25am and Post Master is not to be seen anywhere.

Not sure how to address tnis. My motner is immobile and at home.

First, they can force you to have a bank account to crediting the interest if the rules have changed by govt.

Also, you should take help of RTI here to find out in writing what are the rules and then show it to the Post office guys

I like to know the period where the 5% bonus was not authorized on MIS. It was discontinued for some time, after few months it got reverted back.

Hi Rajendran

I suggest that you now take the RTI route. You can file the RTI and ask your queries to them. THey are bound to reply you on your queries.

Its a bit long cut, but works well

Manish

• A bonus of 5% on principal amount is admissible on maturity in respect of MIS accounts opened on or after 8.12.07 and up to 30.11.2011. No bonus is payable on the deposits made on or after 1.12.2011.

Dear Manish,

I have a joint MIS account with post office from 8.8.2009. My wife has expired on 05.10.2013. It has matured on 08.10.2015. Now I want to get my money and I have the first name. Tell me how to go about it, I have a form to fill (the regular withdrawal form). Does it need my wife signatures.

Yes, her signatures would be required

I searched the net including the official website of Indian Post but could not get any answers to my queries. Details about how to open an account is available everywhere. But, nowhere could I find how to close a MIS upon maturity. Could you, please, let me know the procedure for closing a MIS account after maturity and what documents are required for closing it. Thanks in advance.

I think you need to visit the post office for that with your passbook if any.

Been there. Done that. Was asked for a pan card. Don’t have one. Have only passbook. Is pan card really necessary? Or, is the post officer just harassing to extract his pound of flesh? What are the rules? Thanks for replying.

I think they have a clear RBI mandate that a PAN is required to be furnished .

SIR,

I HAVE ONE LAKH RUPEES MORE THAN THE MAXIMUM LIMIT IN MY MIS ACCOUNT FROM 4 YEARS.

I HAVE BEEN RECEIVING INTEREST FOR THAT EXCESS AMOUNT ALSO.

NOW, POST OFFICE WANT TO RECOVER THE INTEREST AMOUNT PAID ON MIS ACCOUNT FROM ME.

CAN THEY DO SO?

IF SO, UNDER WHAT PROVISION?

NOW, CAN I CONVERT INTO JOINT ACCOUNT?

THANKING YOU IN ANTICIPATION.

I think they can recover it as you have breached the limit .

what is the best scheme to get a monthly return on a investment ?

FD with quarterly interest or MIP

Mane 200000 rupes mis me diposit karna cahta hu but kitna per month milega

Pls reply do

Tkanks

1500

Respect sir . I have invested POMIS scheme the interested will transfer POSB account .we get ESC facility. And how pls tell me

Hi Lekha

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

Manish sir

Mai ek sath 4.50000 monthly incom me dalna chahta hu.ab aap a batay ki paisa jama karne k kitne din bad or kitna paisa mahina milna suru hoga.

Hi Shambhu

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

Dear sir my mother and father have a joint ppf acc in post office.my mother died in 2012 but father us alive but he can’t able signature and we can’t able to take out 3000 amt for last 2 years.money go directly in their post off account which I go regularly and update on post office pass book.i am nominee.i want to know is our money safe.as I informed post office verbally that mother passed away they said it’s ok.but we didn’t take out mother name frm account and its still joint in name of mother and father.kindly let me know about ur view in thus situation. Thnkx

Hi nipunjeet

I suggest that you now take the RTI route. You can file the RTI and ask your queries to them. THey are bound to reply you on your queries.

Its a bit long cut, but works well

Manish

if a joint account ( MIS joint B) is opened who has to pay the income tax on the interest earned ? the first person or the second ?

First person

THANKS

Dear Manish,

I would like to open a MIS account in post office with a minimum balance 1500 rupees.My question is if I open a MIS with 1500 is it possible I can contribute 1500 ruppes on monthly basis to same MIS account,& how I will earn the interest

ie

1st month for 1500 rupees I will earn 11 RUPEES as monthly income

and if I add 1500 again on next month total become 3000 so am able to earn how much on monthly basis

POMIS is mainly for investing a lumpsum and earning interest out of it . What you need is a post office recurring deposit !

Dear Manish Sir,

1) Is there any Similar Monthly Income Scheme in the market other than Post office MIS scheme ?

2) I am 35 years old now, doing private job. Please advice me any good investment scheme which can give me good return at my retirement time (other than PPF).

Thanks in advance.

Vasim

I can only suggest any equity based product to you like Mutual funds !

Manish

Thanks sir.

my father died in April 2015 and his MIS matures in June 2015. I am the nominee. if I submit a claim in May 2015 will I lose the 5% bonus on maturity? if I submit the claim on maturity in June 2015 will I get interest for May, June and also maturity bonus? please reply ASAP.

Yes, you will loose the 5% bonus anyways !

Hi Manish,

My dad (retired for 6 years) had opened an POMIS account post his retirement and chose to invest the interest income in RD.

This year he has received the RD amount along with the applicable interest. He hasn’t shown the RD (basically the monthly return from FD) in his annual income for the previous years as it was within the applicable limits and it was the only source of income for him

My question is : As the RD amount has matured in this year, is it advisable for us to file returns for the previous years now and show the respective interest income (RD) for the years (as showcasing the entire income (RD+Interest) as the current year’s income would make it taxable). Pl advise.

You can now file the return for the full interest income in this year

Manish

can any one invest beyond the limit on mis on joint or individual?if yes than how tax calculated on that?

None of them ..Both offer a below inflation return .

sir, mene 2013 me 1500rs RD par monthly karwai hai 5 Saalon ke liye postoffice se kya aap batayenge ki last me mujhe kitne rupees milenge,,,,,,,,plz

thankyou sir ji.

Hi Sanjay

You should do a rough calculation with 8-9% return .

Manish

Hi manish,

I got little bit confused after reading this article.

Because I had invested 90K in POMIS & then transferred monthly interest to RD. after 5 years ( MIS & RD rate was 8% & 7.5% resp)

total amount i rcvd was 43734. without bonus

it means i got 9.71% of interest.

In current scenario ( MIS & RD rate is 8.4% for both ) so same amount will fetch arnd 10.4% of interest if put it as a MIS & RD

correct me if I am wrong ( all calculations without bonus )

Are you calculating these numbers on CAGR basis ? Or just a plain % return ?

For MIS its plain %

where as for RD its CAGR, rather i’ll say compounding is done on a quarterly basis.

Better do one thing . Take an excel and write your the full cashflow which will happen over the years in both the options and see where you are earnin more return on absolute level !

Sir i want to save money of my grand parents(age-above70).Which one is best for senior citizens….MIS or FD with the banks but i want the facility to take out the money at any time.

FD for senior citizen would be simple and best !

Hi Sir

I have opened an MIS account in my hometown. I stay 4 hrs. away from my hometown and need to close it. Do I need to be present in-person to close the account? I have nominated my father as a beneficiary/nominee in the account opening form. Would that be okay if he signs on the premature account closing form?

Please advice.

Thanks in advance,

Priyanka J

Only you can sign and have to be there to close it !

Respected Manish sir,

I have invested 450000 on my account in MIS scheme and 900000 as a joint account in MIS in August2013. both’s intrest I am utilising ti RD per month in same post office. Then pls tell me how much intrest I am getting individually on MIS and RD per month?!(I would like to know current intrest rates on MIS and RD individually per month)

Hi Suraj

That info you can get only from post office .

I have invested rs. 2 lakhs in M.I.S in post office in 2008 . maturity is in 2014 . march. The post officials have not paid my amount till this today. kindly help in this matter.

Did you apply for it ? It does not come back to you automatically !

My POMIS is maturing next month, i.e. August, 2014. Can I get the bonus and how much if I invest Rs. 4.50 lakhs ? What is the procedure to discontinue the scheme ? Thanks.

I dont think you are eligible for bonus as per new rules

sir..ihave not paid the amount for the past six months in RECURRING DEPOSIT account at the post office…………..do i need to follow any extra procedure to get my account back to normalcy???????/…kindly reply me sir!!!!!!!!!!!!

Not very aware about it . please ask on http://jagoinvestor.dev.diginnovators.site/forum/

Manish, this is a nice article clearly describing what POMIS scheme is all about. My question is given that there is no tax advantage, the interest rate is only 8.40%, and the max. investment amount is 9 lakhs (Rs. 6,300 monthly interest), isn’t it better for someone interested in generating monthly income from their savings to go with traditional FDs instead? The interest rates are higher at 9% and SBI is offering this rate up to 10 years.

Yes, you can surely do that – Its not just about returns, but at times convenience and structure. Someone who has better access to post offices and wants a income on regular basis might prefer POMIS , we living in cities might assume that post offices are not the best choice, but still in smaller places and villages, post offices are very much sought after 🙂

Manish

Can U please tell can I invest in post office monthly income scheme for my son as i have already taken for me and my wife.

Yes, why not !

Hi sir

I am 31 yr old and working in corporate and have planned to start my own business.But before starting my business i want to play safe so have decided to invest a half money in POMIS so that monthly income of nearly 10000Rs is fixed.Can you please guide me is it good or some other better options are available for investing such huge money.Pls guide me asap.

I think its a good idea, but why POMIS ? Why not a simple FD in bank ?

Manish

Hello Everbody,

Apologise at the outset as my comment is going to be rather long – but I can assure you it would be informative to some.

I came across this page while surfing to find whether a MIS started by my father, due to mature this month is eligible for bonus or not. I appreciate the effort put by Manish and all other contributors to let others know their point of view or the information that they have themselves. Unfortunately, however, I could not find the answer to my question here – or rather I wasn’t wholly satisfied by the answer I found here. My simple point of view was (and I am sure everyone would agree) that if someone invests in a government scheme being aware that on maturity he/she is entitled to a bonus of X%, the government CANNOT unilateraly change the act at a later date, so as to deny the bonus to that person. In any case, POMIS does not issue a legal policy kind of document that details all the terms and conditions. All you get is a standard post office pass book and the terms are understood to be as per the applicable act/scheme issued by the finance ministry at that point of time. Therefore, not paying the bonus to someone who invested, after being told that there would be a bonus, should be construed as a fraud on the part of the government – and regardless of the rampant corruption in government offices that we all know of, I don’t think the Indian government would commit such blatant fraud.

The conviction, however, led me to do more research (read surfing), speak to some acquaintances and also a visit to the local post office (to speak to the staff – who simply said that bonus is no longer paid). I could not find a straight answer from anyone, but based on all the research, here is my take on this entire issue of bonus applicable on POMIS. I sincerely hope this post would help a few people at least.

(A) – Prior to 13 Feb 2006 (not sure since when – but it is immaterial now as all such accounts have matured by Feb 2012) the bonus paid on POMIS was 10%.

(B) – Between 13 Feb 2006 and 7 Dec 2007, government withdrew bonus from POMIS.

(C) – The bonus was re-introduced effective on 8 Dec 2007 but was reduced to 5%. This continued till 30 Nov 2011.

(D) – Since 1 Dec 2011, no bonus is payable on maturity of POMIS and also the maturity period was reduced from 6 years to 5 years.

This is the history. As I understand therefore, for all MIS maturing between 12 Feb 2012 and 6 Dec 2013 (category B) no bonus would be payable, as these accounts were initiated when the prevailing finance act did not guarantee any bonus (unfortunately, my father’s MIS falls in this category).

However, accounts maturing between 7 Dec 2013 and 29 Nov 2017 should get a bonus @5% if they fall in category C.

It should be noted that there is a maturity overlap between category C & D as the tenure was reduced to 5 years for category D. Therefore, if your POMIS matures between 30 Nov 2016 and 29 Nov 2017, whether or not you would be eligible for bonus would depend on when you opened the account (category C or D).

I think that this is how it should be and how it is. The reason, not even the PO folks know about this is probably due to the “funny” coincidence that immediately after the latest act was notified (Dec 2011), the schemes that started maturing were those in category B (maturing since Feb 2012), leading to the misunderstanding amongst all (including the staff of various post offices – who should have known better) that bonus is no longer payable. It is my firm belief that after 7 Dec 2013 we will hear that bonus is being paid again!! Would like to hear a confirmation from someone on this site in 2 months time.

And going by the difficulty I faced in this little research of mine, there would be absolute confusion in the post offices across India between Dec 2016 and Nov 2017 – for reasons I have explained above.

Regards,

SG

All I can say is Check your agreement with Post Office , What is written there ! ? Is it written that the rules can be changed anytime in between , if yes, then you have agreed to it . I suggest you open a thread on our forum to discuss this , also keep things short – http://www.jagoinvestor.com/forum

Manish

Dear sir, I invested Rs-9,00000 on 4-10-2011 for M.I.S. as a senior citizen, the interest of which was used on recurring deposit.what will be the total amount I will be getting after maturity. can this amount be extended for six year & what will be the total amount I will be getting on maturity.

Your maturity amount will be communicated to you only by the POST OFFICE . Kindly enquire there itself .

Sir… According to me FD is better than POMIS, coz in FD we get 9.25% for 5 to 10yrs in SBI. and if i choose for 1 yr term it increase to 9.50%.

so is’t right according to me plz help me in this. is’t I want to deposit in BANK or Post office

Yes from interest point of view. FD would be better

Sir, My mother has opened two joint accounts with a total amount of 675000 and 225000. The joint names are my mother and me. She gave the nomination of my father. Sir, she expired two years ago. Should we inform about this to the Post Office. Or there may problem while closing the accounts, Plz suggest. Thnx.

If you can close it without informing then better do it

Sir, Actually I want to know that when we open a joint account MIS with a amount of 900000 (which is for two persons) and one of the account holder expires in between, then it will be treated as a single account. Then how we can get a full amount to a single holder. Is it possible to get it.

Yes, one can get it

Hi Manish, This post is certainly the best place to know more about POMIS. Appreciate your efforts of answering all the questions. I have read through all the questions and got most of my doubts clear. Yet I want to confirm once more on the bonus as I am planning to invest more on POMIS.

I opened the MIS acct on Oct 2010 maturing in Oct 2015 – Will I get bonus ?

If I open a new MIS as on date will I get bonus ?

Thanks

Jaideep

No Bonus after 2012 matured accounts

manish i want to know that interest of my mis can be directly deposit to my canara bank. and for this what are the formalities

You can give the bank details to the Post office

Hi,

I have MIP registered on 28/06/2007 and getting mature on28/06/2013 . am i eligible for bonus ?

regards

No

Dear manishji I invested Rs.300000 in MIS in 12-04-2007, and on maturity I didn’t get any bonus as told by PO, sir I want to know the actual period when bonus is withdrawan (is it between 01-01-2006 to 31-12-2007). Further I want to know that if I reinvest this amount should I m eligible for bonus or not, kindly guide.

No bonus if your MIS matured after 2011-2012

Sir my father and mother invested 4 lakh amount 3 years back in post office MIS plan at Utterpradesh post office Now my father expired and I want to transfer all account to mumbai post office. Will it possible and what is the procedure ?

Hmm .. this is not so simple .

First you need to see if NOMINEE is there in the account or missing . If nominee is missing , then check if WILL is written or not . Only if these are in place, you will be able to transfer it easily by showing the death certificate and filling up a claim form .

It is a joint account of father and mother and my mother is alive ……………

Ok then she can operate it

Hello Mr. Chauhan,

I have gone through several posts about POMIS and found that yours is an excellent one!

I have a unique requirement and I need your suggestion about it.

I want to invest Rs. 15 lakh every month. Therefore, at the end of a year, my total investment will be Rs. 180 lakhs.

I want monthly income and from the safest sources only. I think the best options would be either POMIS or FD accounts.

I do not want to pay tax/TDS etc. What is the best option for me?

Thanks in advance.

Nilesh

Nilesh

The first thing is where ever you invest, if the interest crosses your limit like 2 lac per year, you will have to pay tax ,there is no way you can avoid that

Now coming to POMIS , there is a limit of investing upto 15 lacs in POMIS, so you cant invest more than that

Hello Manish,

As you told me, there is a limit of Rs. 15 lakh in POMIS. Can I open more than one account in POMIS, I think I can open any number of acount. So are you saying that my aggregate of all POMIS should not proceed 15 lakh ?

I have the same question about fixed deposit.May I open more than one fixed deposite account with same name in same branch? Or may I able to add more deposits in the previous ly opened FD account?

In both cases, POMIS as well as FD, my question is that if I want to add some amount, say 10-15 lakh every month, what is the best option? Am I able to open another account or add it in existing account?

Thanks.

I dont think same post office will allow POMIS, you can do that in another post office

Thanks for such a informative page. My question is very hypothetical , hope you will answer it.

If I want to get about 10,000 rs monthly just by investing my money in Bank schemes, how much money will I need to invest. Also which schemes will best suite my requirement.

Around 12-15 lacs would be a good amount !

When compared to POMIS, is it better to invest in a FD with any nationalized bank for 5yrs or 6yrs??

Yes .. i would have choosen FD

Thanks Manish..

My uncle had opened an m.i.s. on 6.3.07 for 6 yrs. He was getting Rs.2813 per month

in a quarterly basis. But surprisingly, when he went to draw his 3rd quarter interest in

Sep.’12 the post office said that you will not gets any interest henceforth, because your

tenure is complete. Then he asked that i have took the m.i.s. for 6 yrs how it comes close? they replied that as per new circular the M.I.S. will be for 5 yrs. and those who opened for 6 yrs. will be closed after completion of 5 yrs. Now, let me know that is it true, if it is true than from when the circular comes in force.

Yes, thats true ! .. whats the harm in that .. ask him to take the money out and use it again in some other MIS

Dear Manish,

Under Monthly Income Scheme if Mr. A & Mr.X had opened MIP of Rs.10000/- maturing in 01/10/12 and Mr. X & Mrs. X had opened MIP of Rs.600000/- which matured prior to Dec’11. Mr. &Mrs. X could withdraw the funds on maturity but when Mr. A wants to withdraw Rs. 10000/- in Oct’12. Maturity amount is held back saying investment of Mr.X has exceeded its limit of Rs. 300000/-. Since Mr. X is common investor, can both MIP be combined to check the maximum limit of Rs.300000/-. If so, then what is a remedy to collect the maturity amount? or what is a penalty to come out of this situation?

Dara

I think there is no remedy in this , check with our forum members http://jagoinvestor.dev.diginnovators.site/forum/

may i know the minimum amount that we can deposit through this scheme

Maximum 4.5 lacs

I think it was some 1000 or something . .check on their website !

year 2006 se 2008 k bich me kya govt ne bonus 5% pomis scheme se withdraw kr liy tha kya pls check kar ke bta skte hai humare agent ka khna h ki govt ne circular issue kiya tha is period me nd bonus withdraw kar liya tha tha.

Yes, Bonus will not be given those those whose maturity is after 2010

great work sir

This is an excellent article and analysis on Post Office Investments!

Thanks Uma

Hello sir,

Im little bit confused,as u knw tht now stock market are up..and i have invested Rs4lacs in mutul funds, I want to knw should i take out my money from mutual funds and invest in POMIS along with RD.Pls guide me sir,i will be very thankful to u.

there is always a risk of money going down in short term .. what is your time frame ?

I had invest money on 12.04.2006 for next 6 years and closed my mis in the month of may-2012, so should i get bonus or not ? Kindly advice us.

I dont think you will get it , any MIS maturing after 2011 will not get bonus

awating your reply.

Dear Mr.Manish,

I read your answers for people’s questions & noted that, for post office MIS there is no bonus payable for accounts opened even before this budget also. But, in the circular released by Govt. of India on 24.1.2011 clearly mentioned in clause 1(iii) that, ”there shall no bonus admissible on maturity in the accounts opened on or after 01.12.2011.”

This means for the accounts opened before 01.12.2011 this bonus should be applicable I mean. I have post office MIS opened jointly with my wife for 9 Lacs opened on 31.12.2009. Can you clarify this matter.

Rgds,

Rajanna K V.

Yes, you should then get the bonus

Dear Mr.Manish,

But, as per your answers as mentioned above for several persons & as per the link of TOI provided by you, the 5% bonus is not admissible even for MIS opened before 01.12.2011 also. So I am not clear about this & I had invested 9 Lacs by considering the bonus factor. If you want I can send you the Govt. of India publications which I downloaded on 24.11.2011. Since it is in PDF format I will send it to your mail. Please clarify.

Ask it on forum – http://jagoinvestor.dev.diginnovators.site/forum/

Sir, My mother opened two MIS accounts with a total amount of 9 lakhs and both accounts are of joint accounts naming me and my mother. Sir, she expired recently. Sir, does there will be any problem withdrawing the amount on maturity for me, if so, what is the way to withdraw on maturity because the amount deposited is for joint holders.

Sowrabh

Not much, but yes, incase htey want joint signatures, then you might have to produce death certificate and other required documents !

Sir, Very much thanks for the reply. Sir, I would plz just want to know what are the documents required, if you can, please tell. Thanks.

It will be death certificate only and a letter incae of joint account, if its not a joint account , then nominee will have to show the id , relation proof , death certificate etc etc

Hello,

I have question:

I have MIS account with amount of 300000 and it’s completed with 2years. Now I have plan to break the deposit and also didn’t took any interest till date.

So how much Money I will going to get now, if I break my MIS account?

2% Penalty

Hi Manishji,

I am planning for go for POMIS so plz guide me for more safe saving shall I direct my interest in RD or not..??? I have account in SBI and already have RD account of 1500 pm for 1 year..Also please guide me for PPF saving . my monthly income is 25 k in hand…Please guide me safe saving I will v very much thankful to you..you can mail me at savisingh_80@yahoo.com

Just keep money in FD and RD in that case, you seem to be very risk averse !

Dear manish i m getting 72358 rs as maturity in case of rd excluding the bonus will u plz tell where i am going wrong?

What is your doubt ? Do you feel the amount is incorrect ?

Yes

can i invest 4.5 lakhs in secunderabad post office, another 4.5 lakhs in delhi and another 4.5 in chennai. whats stopping ?

Yes you can do that !

Dear Mr.Manish,

How is it possible to invest 4.5 Lacs each at 3 different post offices when the limit is only 9 Lacs jointly for POMIS.

I think that should be possible

manish chauhan

AS POST AGENT, CAN I PAY ALL RD SCHEDULE THROUGH INTERNET????

I am not sure about it, you should enquire it at our forum : http://www.jagoinvestor.com/forum

What is the current status of MIS BONUS ? I’ve opened MIS a/c on July 2009.

You will not be getting bonus , All the MIS maturing after 2012 will not get bonus

Dear Sir,

I have invested Rs 2,10,000/- in MIS post office. How can we calculate with RD + Bonus. Please give me exact answer with calculation

You should be getting a montly income and now there is no BUNUS on MIS , i think you should be knowing that !

I had invest money on 29.11.2011 so should i get bonus or not ?

i want to invest in mis of Post office , how much amount can i invest for a year

There is a limit of Rs 4.5 lacs for per person and 9 lacs for joint account

Glad to see this blog, with a very good option(MIS) which I never heard before.

I have been brosing websites for 3 weeks to invest my 1.5Lac rupees. excuse me if that is too long to think for investing 1.5lac of money. But I am looking for 0 risk investment.

I have already started small RD with 3000 and a 5000 for 27 month period @ 9.25% with HDFC.

Also I have a PPF account started this January. I am already exhausted at 80C section. So took infrastructure bond last year and planning one for this fiscal too.

I have been thinking of Fixed deposit(1 -1.5L) with HDFC/ICICI or NSC and now MIS.

It would be really wonderful if you can guide my investment as my brain is already storming with what to do. 1.5L have been sitting in my SB account for more than 2 months now. I actually do not need that now. As myself and wife are working and earn monthly around 60,000. So we would save further with our monthly salaries and would look in similar way(as per your answer for this question) for future investments too.

So can you please guide where to invest MIS/FD/NSC.

a. FD I have looked/liked is HDFC @9.25% compounded quarterly for 1year 16 days. I would reinvest the capital after maturity in same or similary FD. (interest gained would be put into PPF)

b. NSC VII issues @ 8.60%

c. NSC IX issue @ 8.90%

d. MIS @ 8.50%

Please post with maturity value, monthily/quarterly/annual interest accrued as applicable. I would file 15H for FD so no TDS. Please provide amount(figures) for each of these. Also it would be great if you can provide me link for XIRR excel sheeet, I would like to experiment with that too.

Thanks in Advance and looking for your reply.

I think you are complicating the situation , just make 2 FD;s for 75k each , that all you need to do if you are looking at it from short term point of view ..

thanks Manish for a very quick reply.

And after your comment, I was not yet fully satisfied(Sorry). So was still browsing and surprisingly again landed in this jagoinvestor website only.. 🙂

this time your PPF column.

Actually I was calculating different ways, how much interest I would acrue.

for 1,50,000 investment:

HDFC FD 6M1D @ 7.75% = 5902

HDFC FD 12M16D @9.25%=15030

HDFC FD 6M1D @7.75%=5902 ; reinvest including interest again for 6M1D@7.75%=6134

MIS @9.50% 5 yrs = 1061 p.month, 12741p.annum, 63706 for 5 yrs

NSC @8.60% 5yrs = 78525 for 5 yrs

Of all these cases, HDFC FD 12M16D is more efficient as year end yield is higher compared to any other.

But interest received is not of my more interest. So was checking where I could invest the interest accrued. There I reached to PPF.

Hence if I invest 15030 per annum into PPF, I receive much lesser than investing interest 1061 (from MIS per month) every month into PPF.

Where PPF is considered to e 8.6%.

My 1,50,000 would still be continued/re-invested in MIS/FD whichever case you advise.

your inputs are appreciable. And please let me know if I can share your link in Facebook. It is really a useful link.

I think you are complicating the situation beyond the limit , The difference in two options is very small to work so hard 🙂 . Why do you want to reinvest your interest part somewhere else ? Just choose the interest cumulative option in the FD itself .

Tell me 5% bonus begins in which time? Also tell me that when I commence the MIS 2010 then bonus was guaranteed @ 8%, so tel me that in that case whether I will eligible for bonus @8% ?.

Deba

Do you have a written proof of bonus at 8% , I have never heard it more than 5% and now its abolished also !

I want know regarding payment of bonus on POMIS. I had taken POMIS by depositing a sum of Rs. 200000/- in May-2006, which is going to mature after completing 6 year of term by 1st. June,2012. Let me know if any bonus is payable to with principle amount.

No , recently in last budget it was scrapped and policy have maturity in this year are not going to get bonus .

Dear Bhag Singh,

Did you receive any additional bonus?

Thanks !!!

The interest rates have changed recently.

MIS – 8.50% per annum w.e.f. 01.04.2012 and no Bonus

RD – 8.4% per annum

Thanks

thanks for the update Srinivas

The info. you provide is of great help to senior citizens. Is it possible to get back the investment done on 11th may 2011, fifteen days prior to the year, as we need the money urgently.

Thank you

regards

saras

Look at the minimum lock in period , I think its one year only

Dear Manish,

How NRE can invest in this scheme? What kind of documents has to be submitted while opening this account?

PTNM

that info you can get from POst office website .. you will mostly be needed to be physically present !

is there any check point between all POST offices that in one name maximum limit 4.5 lacs only allowed?

i mean: imaging one guy opened PO MIS in mumbai post office 4.5 lacs

& he also later open another PO MIS in pune or delhi post office for another 4.5 lacs…

is there any cross checking there existing?

PTM

I dont have info on this .. Its possible that one person can open a MIS at two places … Better ask it on our forum to get more clarity http://jagoinvestor.dev.diginnovators.site/forum/

hi sir

what will happen if an NRI hides his status and opens PO-MIS with RD…..

PTM

Its possible that NRI can hide his status and open the POMIS , but incase they come to know that you are NRI , then all those rules will get applied.

what are those roles that will be applied? can u clarify more please?

PTM

I mean whatever penality/rules are defined . In this case you will not get any interest

Thanks , Manish. Please also tell me about some best available monthly income schemes of different banks, which are similar to POMIS. Also clarify the investment limit of those schemes, rate of interest given by the banks and TDS deducted from the interest.

Girish

The only comparable things like that is Bank FD with monthly or quarterly interest nothing else. MIP mutual funds with divident options also are one of the option !

Thanks for the mentioning the ECS part in the post. Jus verified ECS to other s/b accounts is allowed in select cities only !! link below

http://www.indiapost.gov.in/ECS.aspx

Rajiv

Yes , it might be the case that htey allow it in some cities only !

Girish, Dt 17th march 2012

from the above articles many of my confusion have been cleared. Pl let me , which is more beneficial, whether to keep money in G.P.F account or to withdraw the money from G.P.F account and then invest it in POMIS and P.O saving account.

Girish

GPF would be more better, but then its not 100% in your control

Manish

I wanted to know from which month/year the 10% bonus on MIS discontinued

SHernaz

From this year itself . Now onwards when you invest in the MIS , the bonus will not be given and it was 5% , not 10%

hello all

Going through a tough time as my father expired last month…my father had 3 FD accounts for the POMIS of Rs 3 lakh each…all 3 are joint accounts…2 in name of my mom-dad with my name as nominee,,and one joint in name of dad-me n mom as nominee….Date of deposit 12-5-08,,dateof maturity 12-5-14….same in all 3 FDs…….I want to know is it necessary to close these joint FD accounts prematurely??One thing more,,the saving account passbooks of post office in which the Monthly income/interestRs 2000 from each FD was deposited dont mention any nominee name??will the nominees of these saving accounts be same as FDs???plzz advise…i shall be highly obliged….thnxx in anticipation

Sahaj

No its not neccessary to close down those FD’s , because its on joint name , so the other person is now the main person who can manage those FD;s . the FD nominee’s can be different than the saving bank account . Check the saving bank data

Manish

thnxx a ton manish….i m really grateful

thnks frnd this is realy good information about mis and to reinvest the interest in RD further …………….

Thanks Pradeep !

Dear sir, i am planing to invest 8 to 10 lack in post office monthly income plane, how much money i will get every month ??? or where should i invest in monthly income plane?

Dear sir, i am planing to invest 8 to 10 lack in post office monthly income plane, how much money i will get every month ??? or where should i invest in monthly income plane????

MIS means monthly income scheme,but till today ie 6 2 2012 the interest has not been credited to my s/s a/c.It will take another 2 or 3 days which has been informed by the po authority,when it was enquired. I do not like to complain but sorry to say service should be improved immediatelly.

I want to know that interest from MIS with RD is taxable or not?

Taxable

Dear Manish,

I want to know how to invest in PPF – On monthly basis or yearly.If yearly when it has to be deposited to earn maximum interest.I have opened PPF account just one month back.

Please suggest.

Regards

Rahul

Rahul

invest monthly before 4th

Manish

I have 10 lacs. Pz advise where and how to invest?

Manju

What is your requirement ?

Manish

Hi Manish,

Gone through your blog, its very good and informative.

Please revert on my query. Thanks in advance.

My uncle was having an MIS account with deposit of 3lac with his wife as a nominee. He used to withdraw the interwst money in every 3-4 months.

Uncle died last year in April 2010. Aunty , got to know of the account and had taken time to collect the documents like death certificate n all and gone to post office in in May 2011 to inform Post office as well as to withdraw interest (2000 per month ) from post office. Still they gave her the interest money and told her some procedurs needs to be done to close the acount. (uncle had last withdrawn the interest accrued in March2010 )

Now, in september 2011, she requestd for MIS account closure, then they asked her to return the interest from April 2010 till september 2011 .

1) If they were not supposed to give the interest then why did they give in the first place in May 2011? ..

Post office people state that they came to know about uncle’s death in Sept 2011, only

2) Now aunty had given the interest back to them, is she eligible to get atleast the basic interest of saving bank account from April 2010 till September 2011. Since the deposit money of 3laC (April 2010 – Sept 2011) as well as the interest of 2000 rs (April2010 – May2011 = 14* 2000 = 28000) was with Post office only.

Please excuse for the length of the question.

Thanks,

Akshay

@ Akshay

Recently we faced similar situation like yours. This is what we have learnt. When a person is died, there should not be any interest withdrawls from the account henceforth. No one else is supposed to operate the account. Once the death certificate is submitted, PO has to cancel the account and refund the amount to the nominee. PO would investigate the nominee claim and verifies the death certificate through investigation. It takes about 2 months. Once it makes sure everything in order, the principal and interest (from date of death to cancellation date) would be refunded to the nominee.

Krish,

Does that mean that The Nominee will receive the interest (standard 2000 rs @ 8% or @ savings bank account rate(example 3- 4%) ) for the period from date of death to cancellation date

i.e. Will my aunty eligible to get the interest from April 2010 – September 2011

(SOme post office people are only suggesting that you file a complaint against this, you should get atleast the interest @ savings bank account rate.

Please clarify and tell the actual amount of interest for amount deposited of 3lac .

Thanks a lot

Akshay

Your aunt should receive Rs.2000 a month from Apr’10 to the refund date along with a principal. In our case, PO paid it like that (8%). I don’t see any reason why PO should deny the interest or pay less interest if person is not alive but money is with them.

Thanks a lot Krish,

Now, i will tell my aunt to file a case against PO and ask for the relevant interest.

I want to invest Rs.10 lacs, so pl advise me where/how to invest?

What is the meaing of SIP?

Manju

SIP is Systematic Investment Plan. It means investing monthly in mutual funds .

Manish

Govt increases the interest rate from 8% to 8.2% but scraps the 5% bonus on maturity. Also it states that rate notification will be from Dec-1 and the MIS of old schemes maturing after Dec-1 won’t get the 5% or 10% maturity bonus? Is this true? If yes then we should take forward it; how can govt not increasing the interest rate of our savings from the date of invested even not giving a single penny of increased interest rate rather they are snatching the maturity bonus (5% or 10% of old schemes) from us if the maturity date falls after 1-Dec.

Jit

As far as I know , the new rates and scrapping of Bonus is applicable only for new accounts . Any old account will get all those benefits which was mentioned before . Where did the info that old accounts will also not get BONUS ?

Manish

Manish;

Here is the extract of an article published in Times Of India which states that:

“There are some disappointments as well. The government is withdrawing Kisan Vikas Patra, on suspicion that this is being used for money laundering. It has also decided to do away with the 5% bonus that MIS customers got at the time of maturity. What is even more disappointing is that this withdrawal of bonus payout will be applicable even on old accounts that remain operational on or after December 1. ”

The link is:

http://timesofindia.indiatimes.com/business/india-business/Now-get-more-on-small-savings/articleshow/10913006.cms

Please clarify on this.

Jit

As far as we know also that anything new should be applicable on new items only and old schemes would be in tact as it offered earlier till its maturity. But if this is the case of hampering old ones too as per claim made by Times of India’s article then don’t you think investor are going to lose a large chunk of their waited bonus.

Jit

Jit

Yes .. but if at the time of taking the product , it was mentioned that the govt rules can change and the rules at the time of maturity will apply , then you cant do anything

Manish

Jit

yes .. i saw that article

Manish

I gone through the official notification on MIS by MoF; it states that

” There shall be no bonus admissible on maturity in the accounts opened on or after 1-12-2011″

So how come this is possible as per Times Of India article to curtail the bonus on existing accounts maturing after 1-12-2011.

Jit

Actually I also saw that and I could not get an offical wordiings on this . It might happen that TOI thing is wrong . You must check with PO directly on this

Manish

please tell me the bonus rate with effective date to closing date

Hey Manish

Read you blog for the first time today, and I must tell you, its just great !

keep writing and keep helping us 🙂

And, I assure you, I will pass on this information to others as well!

Rohit

Good to hear that 🙂

Hi,

Govt recently change the POMIS interest rate from 8% to 8.2% and discontinue the 5% bonus.

My question is which scheme is better, new one or old. from which i will get the more return?

Amit

from absolute return point of view , the old one was better because you got 5% bonus at the end .

Manish

Sir

i have deposited an amount of Rs. 90000 during january 2006.i want to know how much bonus i will get

Venkat

venkat

it would be 5% of 90k which is 4.5k

Manish

If your intention is to make your money grow, then probably KVP is a better option than going for POMIS + RD.

Smith

Have you done any number crunching on this ? please share

hello

I want to know that i am having 100000 to invest, no. of years is unlimited as i am 32 yeras and i want monthly return from this money.

So how much i will get as monthly return..please suggest

Pooja

You can expect 600-700 per month

Manish

Hi, I want to invest 4 to 5 lac per year in post office or any other monthly scheme. I want very good monthly return.

pls guide me

Pooja

If you want a fixed and secure return , then you can get average returns only , not “good” or “great” returnrs . for that you need to invest in MIP or something else

Manish

My MIS will mature shortly with 10% bonus. I have been paying Tax on the interests I have been getting. Will the bonus be taxable at the applicable rate for me. My highest slab of tax at present is 30%. Is there a way I can save tax on this bonus?

Swapan

Bonus will be taxable

Manish

Hi Manish

One important query and help, Is it possible for the post office RD account, every month the amount can get auto credited from the post office SB account…

Thanks

VJ

This can be told by Post office only . See what rules they have there .

Manish

its a nice article . is there any more scheme or plan that can attract my intention because i already knew about it.

There are MIP’s or FD’;s

Manish

rate of bonus investe date in mis=26-4-2006

I Have invested rs. 600000=00 date-26-4-2006. please give me bonus rate after 6 years.

Manish,

very nicely presented matter and most important, very informative.

1) I would like ask one thing after reading this article that whether one should invest in POMIS with RD or FDs.

2) I came to know that we don’t have any taxation on POMIS…is it right?

Hoping for ur great response.

Adesh

Dr Adesh

1) where to invest ? It totally depends on what you want, you know what is FD , its locking thing , its return , its risk and same for POMIS , now what is it that you want ? POMIS will lock in your money

2) Who said that , POMIS interest is full taxable .

Manish

I wanted to invest my 60,00000 money in POMIS which i got from sale of my house..Is it possibel

Nitin

No , there is restriciton of 4.5 lacs in POMIS

Manish

just visited your page for the first time, and let me tell you it is realllly interesting and informative. i’ll search for all materials that interest me. good work, thanks a lot.

Sure 🙂 . Keep reading

i have a little confusion about principal amt. could you plz let me know whether i will get my whole principal amt on maturity period or not. Say by investment of 1,20,000 in POMIS for 6 yrs. on this i will get my monthly interest. but at maturity period how much i get.

We already repplied this : http://jagoinvestor.dev.diginnovators.site/2011/01/post-office-monthly-income-schemes-pomis.html#comment-21915

Manish

i have one doubt please clarify it.i would to invest in POMIS.

if invest 100,000 for 6 yrs on that i will get montly income but at the maurity period whether i get my full principal amt with bonus or not.

Ansh

Yes you will get monthly interest and you will also get maturity amount along with 5% bonus.

So in your case, if you deposit Rs. 100000 for 6 years you will get Rs 800 per month and at maturity you will get Rs 105000.

–

Jagoinvestor Team

Whether monthly interest paid in POMIS is taxable?Whether there is any TDS?What is the rate/amount of income tax one has to pay on maturity of such MIS ,say for a principal amount of Rs.10000/-?

MIS talks of joint investment upto 9lakhs what happens in event of demise ofone of the jointholder if this amt has been invested already ===can a fresh joint holder be added to this existing mis a/c

Aruna

If one of the depositors of an MIS account dies, the account will be treated as a single account in the name of the surviving depositor from the date of death of the said depositor. When a report to this effect is received in the post office, the Postmaster will ask the surviving depositor to withdraw the excess amount in excess of the limit prescribed for a single depositor (Rs 4.5 lakh) and this excess amount will not carry interest from the date of death of the joint depositor. The interest already paid on this excess amount will be recovered or adjusted.

A small care has to be taken. The surviving single account holder should effect a nomination as soon as possible.

Hi Manish,

Just a tweak to aruna’s example.

My uncle was having an MIS account with deposit of 3lac with his wife as a nominee. He used to withdraw the interwst money in every 3-4 months.

Uncle died last year in April 2010. Aunty , got to know of the account and had taken time to collect the documents like death certificate n all and gone to post office in in May 2011 to inform Post office as well as to withdraw interest (2000 per month ) from post office. Still they gave her the interest money and told her some procedurs needs to be done to close the acount. (uncle had last withdrawn the interest accrued in March2010 )

Now, in september 2011, she requestd for MIS account closure, then they asked her to return the interest from April 2011 till september 2011 .

1) If they were not supposed to give the interest then why did they give in the first place in May 2011? ..

Post office people state that they came to know about uncle’s death in Sept 2011, only

2) Now aunty had given the interest back to them, is she eligible to get atleast the basic interest of saving bank account from April 2010 till September 2011. Since the deposit money of 3laC (April 2010 – Sept 2011) as well as the interest of 2000 rs (April2010 – May2011 = 14* 2000 = 28000) was with Post office only.

Please excuse for the length of the question.

Thanks,

Akshay

Hi Manish,

A small correction to the previous post,

When Aunty requestd for MIS account closure, then Pos office people asked her to return the interest from April 2010 till september 2011

(not from April 2011)

Thanks ,

Ashay

hello, nice site

can you tell me the folowing.

1. i opened an RD account in the year 2000, and continue to pay the monthly amount of 500 regularly, even after maturity i continue to do so till now. now from march onwards if i stop what happens if i keep the amount without withdrawing tilll another 5 yr?

do i get any interest?

if so at what rate?

or is it beter to withdraw and open MIS seperately linked to RD?

can you explain?

regards

Regarding crediting of MIS interest to SB accounts in post offices,I have had bad experience,they just do not give any regular interest credit in SB account for the balance amount .If any one knows the rules about Interest Payment To SB Accounts in Post Offices,kindly let me know ? It is better to avail ECS facility and get the interest credit to any Bank.

I dont have any experience in this .

Anyone else knows about this ?

Dear Manish,

Thanks for all I know about investments through your blog/site. This link given below gives where ECS is available for Indian postal departments. I have few quires about my investment and Portfolio but first I would like to learn more so I could ask right question to you.

Thanks

Mohinder bidht

Thanks for the link

Sir please help us we I m syed yusuf are have fixed deposit in post office MIS for one year but now just complete 2,month sir now we are urgentlly need amount but in in post office say its not possible you wait 8 months your period is completed than you take sir god promise we are not wait one month also because very very need so can you give me any suggestions and help us

You can withdraw it only after 1 yr is completed , not before that , this is the rule of POMIS !

Pre-mature Withdrawal from Post-Office monthly Saving Scheme

Even though the maturity period for POMIS is 6 yrs , there is facility to break it and take your money out. However you can take your money only after 1 year. You have to pay some penalty which is as follows

If you break it within 1-3 yrs : 2% penalty on Deposit amount

If you break it after 3 yrs : 1% penalty on Deposit amount

Example : If you deposit Rs 1 lac in POMIS , and want to take money out in 2nd year, you will have to bear the penalty of 2,000 and you will get back 98,000. If you take money out in 5th year, you get 99,000.

This is really a good post, I’ll try to remember. I think MIS ia good for retired person.

Caribou

Yes .. it can be

Hi Manish , nice article as usual

POMIS gives 8% return and Senior Citizens Savings Scheme (SCSS) gives 9% return

so please give ur sight on that one too.

what if we combine SCSS with RD so that we can generate 1% extra return?

Pankaj

SCSS gives 9% and its better than POMIS when it comes to returns, but its because its limited to senior citizens , govt gives better facility to them .. so if there is some senior citizen , its makes sense for him to invest in SCSS

thanks buddy my dad is a senior citizen having 10 lakhs lookin for monthly return policy . i will suggest this to him

thanks

Pankaj

He can look at Senior Citizen saving scheme option as investment , he will get 9% interest

Manish

which scheme is more beneficial post office monthly income plan or fixed deposit scheme

pradeep

You cant compare like this ..MIP might give higher return , but it comes with some risk

manish

Hello Mansih,

Good information like always. Just want to add my 2 cents here. ECS facility for direct credit of interest of MIS is currently available only in 36 locations of post office and not throughout in India. One can check these locations through official website of Indian Post office at

Gopal

Thanks good info .. added it in blog

Manish

Hi Manish & All Members

One more thing i want to say that POMIS is good as comapred to NSC, if anyone wants to invest over 1,00,000 u/s 80c for saving Tax. POMIS gives better return than NSC. Below is a comparing chart between POMIS & NSC.

6 YearsPOMIS+RD 6 Years NSC

Sum Assured(A) 1,00,000 1,00,000

Monthly Interest 667 _

M.V Of R.D of 6yrs (b) 60,702 _

5% Bonus on SA (c) 5,000 _

Total ( b + c = D) 65,702 _

After 6 Years Total (A+D) 1,65,702 1,60,100

No TDS No TDS

So its better to invest in POMIS which gives you Rs 5,702 more than NSC on 1 Lakhs, And Rs 25,659 upto 4.5 Lakhs. Isin’t It ?

NOTE- investment upto rs 1 lakhs is good in NSC as it saves tax u/s 80c but after that limit intrest earned on NSC is Taxable. So why not to choose POMIS ?

Mukesh

Hare Krishna

Mukesh

yes ,, one can invest in POMIS , if one’s requirement is of monthly income , this makes them better than NSC

Manish

I thought.. irrespective of how much you invest, the returns in NSC is taxable.

Regards,

AK

Great information Manish! Especially the RD part.

Thanks Atul

The XIRR calculation is fallacious in the article.

The calculation in the article assumes that one invests 800/- every month.

But that is really not the case. We invest at the beginning and keep quiet and take back the returns at end of 6th year. The movement of money from POMIS to rd happens automatically and should not find an entry in our xirr calcluation!

Here are the inputs for xirr calculation!

1-Jan-01 -120000

1-Jan-07 192806 (=1,20,000 + 72806 (RD proceeds) + 5% bonux from MIS)

XIRR = 8.2200053

Lakshman

Its not fallacious , I am only considering the part where you calculate the returns out of RD and bonus, so if you invest 1,20,000 in POMIS ,you get 800 per month ,now thats going to RD , so eventually it was your money which you are investing in RD and then some maturity value is coming out of it + BONUS ,the chart shows only that part and it turns out to be 10.60% , and yes I agree that its not the right figure , because it includes BONUS value ,without Bonus value it will be somewhere around 7.9%

What you said at the end that we just pay 1,20,000 in start and get 1,98806 total at the end is the actualy RIGHT picture and the absolute returns out of the whole situation ,but its coming to be 8.77% for me . Not 8.22% , check again

manish

Hi Manish,

Thank you again for a very nicely written article on POMIS…As we know the interest on POMIS is taxable.Kindly let me know how much tax I would pay taking the same example above

thanks

Manish

Its simple, the income you get out of it will be added to final income of the year .. So as per your tax slab you will be taxed

Manish

Hi Manish,

Is there any minimum limit for investing in POMIS.

Whether it can be done with lumpsum one-time amount in a year or like a SIP?

Considering the city change, how i can manage the account?

Sangmitra

There is a lumpsum investment option in POMIS , you cant do SIP kind of investment ,. its mainly to get montly income , so you generally make a big investment in expectation of getting monthly return .

Minumum investment is 1500 i guess .

manish

10x

What is SIP?

Last year I made an investment in POMIS for my parents. At that time banks interest rate were around 6-7% which made POMIS attractive.

The scenario is changed in Jan’11. SBI is offering 8.75 rate upto 10 years. HDFC bank is giving 9% for 2+ years and looks to me that all bank deposit rates are much higher than POMIS. To me in the changed environment, it does not make any compelling reason to invest in POMIS. The banks like HDFC also ready to give out interest money on monthly basis. That too they credit to your account and you can withdraw using ATM card whenever you want.

Dear,

The Bank will deduct 10 % TDS straightly on the Interest earned on any FDs and if you don’t provide PAN, the TDS will be 20 %.

Thanks & Regards,

Sudhahar R

yeah Manish, can you clear up the doubts raised in comments?

Abhishek

I cleared it 🙂 . Any thing else ?

Manish

@Manish

Nice post. Its understandable that the interest earned on POMIS scheme will earn 10.75% in RD.(But slightly confusing the readers that if we invest in POMIS scheme and choose RD, in total the proceeds will earn 10.75% interest). As SmartSingh mentioned deposits at best will earn 8.8%. I guess it will be good if you include a sample calculation as given in india post calculator to clarify the doubt.

Regards

Jagadees

Jagadees

Yes , I have added the example chart in the main article . I agree that the overall returns turn out to be 10.60%

Manish

Please, anyone tell me that after mataurity of POMIS can we extend this or we have to restart this.

Virag

You can start a new account anytime , you can open a new account even paralally , just that the whole limit of 4.5 or 9 lacs (joint) has to be there .

Manish

10.5% is the attempt by India Post at marketing gimmicks. [To compete with the gimmicks of private players? :-)]

One could calculate the IRR for the POMIS+RD arrangement, and it should come out somewhere between 7.5% & 8%. [I’m too lazy & tired to do so myself now. :-)]

The funda is this: When your money rests with the POMIS it earns 8%, and when it goes into the RD it earns 7.5%. Compare it with a cumulative FD at X%. The principal earns interest at X% and the interest earns further interest at X% so the yield is X%. The POMIS+RD arrangement is similar except that the principal earns 8% and the interest earns 7.5%, so the final yield would between the two (pre-tax).

Note that both POMIS and RD interests are taxable so the yield will get reduced accordingly. Also note that the POMIS bonus and the quirks of RD formula* would slightly increase the yield.

[* in case one is interested, the quirk of RD formula is thus: If one makes an investment every quarter all with the same maturity date, each of the principals will be compounded for an integral number of quarters. However with RD there is a funda of compounding for fractions of quarters, e.g. the first monthly installment gets compounded 20 & two-thirds times, the second gets compounded 20 & one-thirds times, the third 20 times, the fourth 19 2/3 times, etc. Check ou t the formula at

Slight mistake in the RD explanation I think. Instead of 20 2/3, 20 1/3, 20, 19 2/3, … it is actually 20, 19 2/3, 19 1/3, 19, …, 1 1/3, 1, 2/3, 1/3 (last installment compounded for 1/3 quarter, i.e. one month).

I don’t understand Padmanabhan that how 10.5% becomes 7.5% even with fractional compounding?

@Manish and others,

The RD will not fetch you 10.5% it is the interest part which earns which is approx. Here it is how.

You need to open a savings a/c and RD simultaneously while opening a POMIS. Then the interest will be transferred to Savings A/C automatically and it will be transferred to RD. The rate of interest for savings a/c is 3.5% p.a and on RD is 7.5% which translates to 10.5% totally, which is approx.

Krishna

Actually, I tried the calculator on the India Post page ). There is really no need to calculate an IRR. Just calculate what you deposited and what you got, in the best case it comes around 8.8%.

I tried it with the deposit of Rs. 75000.

Very well said!

Here is an example to get a clear view of what you get.

Suppose you invest Rs.1,00,000 for 6yrs in this scheme. The total amount you get after 6 yrs including the 5% bonus is 1,65,702.

Now calculate the Cumulative interest using the calculator(http://jagoinvestor.dev.diginnovators.site/calculators/html/Return_Calculator.html) . The interest turns out to be 8.781 %.

Also note that the returns may not be TDS exempted. (I am not sure if the interest deposited in RD for 6yrs will be tax exempted or not?)

Kamal and Smart Singh

I tried calculating the returns with XIRR with an example , looks like when you include the bonus , the actual returns are in range of 10.5% . See the chart I added in the main article

Manish

Manish,

I am still not clear. For the example you had, you invest 1,20,000 for 6 yrs(forget the details how it gets put into RD and stuff for time being).

The total return at the end of 6 yrs is

1,20,000 + 72806 + 6000(bonus) = 1,98,806.

Now calculate the interest if compounded annually using one of your CAGR calculator(http://jagoinvestor.dev.diginnovators.site/calculators/html/Return_Calculator.html)