Should you Invest in IDFC Infrastructure Bonds

POSTED BY ON October 7, 2010 COMMENTS (139)

From the Budget, infrastructure bonds are also eligible for additional tax exemption upto Rs 20,000 over and above Rs 1 lakh under Section 80C. IFCI Ltd was the first company to issue these infrastructure bonds and they have collected a substantial amount in the last few months. Now, IDFC Ltd has introduced its infrastructure bonds and there are a lot of investors, who are considering these bonds as an option to save additional tax for this year. Rajendran and Prashant have also asked the questions related to Infrastructure bonds some days ago on Jagoinvestor Forum. In this article, I give you brief information on IDFC Infrastructure Bonds.

The maturity period of these bonds is 10 years and the lock-in period is five years. These bonds will be listed on the Bombay Stock Exchange and National Stock Exchange. After completion of five years, you can keep these bonds for additional five years and withdraw money at the time of maturity. In case, if you need to withdraw money before maturity, then you always have an option to sell these bonds on stock exchanges. Thus, these bonds can be traded like stocks on the stock exchanges but only after the lock in period of five years is complete. You would require a demat account and Permanent Account Number (PAN) to invest in these infrastructure bonds. The face value of each bond is Rs 5,000. The minimum application has to be for two bonds and in multiples of one bond thereafter. Hence, the minimum investment required is Rs 10,000. You can invest more than Rs 20,000 in these bonds but the tax-exemption would be only upto Rs 20,000.

Taxation on Infrastructure Bonds

You will get tax exemption benefit up to Rs20,000 when you invest in these bonds. However, the interest gained will be taxable. The interest would be added to your income and taxed at the existing slab rate. this taxation rule will be same even after Direct Taxes Code (DTC) Bill comes into effect. Both, the current Income Tax Law and DTC require you to pay tax on the interest earned.

Infrastructure Bonds in different series

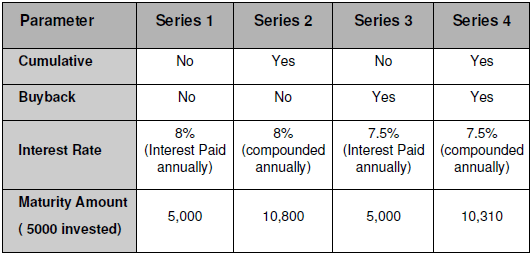

Note that these bonds come in 4 different flavors and they are called as Series 1, 2, 3, 4 . Each of these series is different from each other in some way. There are two main things you should understand , which might be of concern to you.

Interest Cumulative : Series 1 & 3 do not provide cumulative interest. They will pay interest annually. For example, if you invest Rs 10,000, then after completion of 12 months, the interest amount will be paid to you every year and the bonds maturity value would be same as your investment. However, bonds which have cumulative interest will keep accumulating interest. And this interest would be compounded every year. (see CAGR)

Buyback : Series 3 & 4 have buyback option. Buyback option means that you can sell your bond back to issuing company after five years; once the lock in period is complete. In return, you will get back your original invested amount and the interest accumulated for five years. You would notice that interest rates for series 3 & 4 is 7.5%, which is because they have an added advantage of buyback facility. If you don’t want buyback option, you will get 8% interest. People not opting for buy-back options will depend on secondary markets to sell their bonds if they require money urgently before maturity (10 years). Thus, after lock-in period (five years) is complete, they will have to find a buyer in secondary markets else wait till maturity, when they will get the money back from IDFC.

Other features of IDFC Infrastructure Bonds

- NRI’s cant invest in these bonds (Only available to Resident Individuals and HUF’s)

- The bonds don’t attract any TDS

- The bonds are rated LAAA by ICRA, However high rating is not something you should be very excited about. (Link)

- The interest accrued on the bonds will be credited to the respective bank registered with the demat account through ECS on the due date for interest payment

- Interest on the bonds shall be payable on annual or cumulative basis depending on the series selected by the bond holders

- The bonds can be pledged for availing loans after the lock-in period of 5 years

Subscribe to the Bonds in physical form

If you do not have demat account and want to apply for these bonds in physical form , you can still apply for them using these steps (link) , Thanks to Srinidhi for giving this info .

- Don’t fill up the demat details in the application form

- Compulsorily provide the following three documents with the application form:

- Self-attested copy of the PAN card;

- Self-attested copy of a cancelled cheque of the bank account to which the amounts pertaining to payment of refunds, interest and redemption, as applicable, should be credited.

- Self-attested copy of the proof of residence. Any of the following documents shall be considered as a verifiable proof of residence:

- Ration card issued by the Government of India; or

- Valid driving license issued by any transport authority of the Republic of India; or

- Electricity bill (not older than 3 months); or

- Landline telephone bill (not older than 3 months); or

- Valid passport issued by the Government of India; or

- Voter’s Identity Card issued by the Government of India; or

- Passbook or latest bank statement issued by a bank operating in India; or

- Leave and license agreement or agreement for sale or rent agreement or flat maintenance bill; or

- Letter from a recognized public authority or public servant verifying the identity and residence of the Applicant.

Should you Invest ?

Though, it’s mentioned that the interest rate on these bonds are 8% or 7.5%, the interest earned would reduce further to 5.5%-6% range when you count the tax paid on interest. But if you look at it from a different angle, and count your money saved due to the tax-exemption at the time of investing, in that case the return would turn out to be around 9.5%-10%, but do you think it’s the right way of looking at returns?

What do you think about these bonds ? Are you investing or not and why ?

Is it better to opt for the buyback offer or wait till maturity for IDFC Long Term Infra Bonds (2011-12)??

Awaiting for an early reply as I’ve to give consent till 21st Nov.

I have no clue on that

For the infrastructure bonds – is it best to go for buyback option or sell it through stock exchange with STT?

Better go with buyback option.. as the liquidity in stock exchange might not be there !

Thanks Manish for the reply. I have IFCI Option Infrastructure bonds. I see there is some liquidity in the exchange. The volume is 52 on 5th July. From the tax perspective, does it make any difference between selling through the exchange and buyback?

From tax perspective it makes no difference!

Dear sir,

I have also invested in L&T infra bonds on 22/2/2011.

I want to know when the money will be credited to my account from these bonds.

DP ID/ CL ID / Folio #: 383344-10541972

Regards,

Manish Chawla

9136001645

Hi ManishChawla

This is very specific query which you should follow up with the concerned authority only. We wont be able to comment on that

Manish

Hi,

I have L&T bonds which are now lock free. I dont see any liquidity to sell these in the market. Is there nay other way to sell these?

Anuj

No, if you dont have to buy them. YOu can only sell them back on maturity

Hi,

I think you are the one who can guide me. Pretty nice details.

I have series 2 bonds which I bought in physical form during November 2010. Can I sell it through my demat account?

Thanks,

Murali

Yes, but you need to first demat it, only then you will be able to sell . Also there has to be a buyer for you to sell.

Manish

how to i sell it after that lock in period of 5 yrs..i bought it in papers and not via demat

If the lock in period is not over, then you can try your luck on secondary market to sell it, but I think you will face issue ! ..

Hi,

I purchased through ICICI direct and i can see these in my Demat Portfolio under FD/Bonds.

It seems there’s some corporate action also recently as i got mail like below:

Demerger IDFCB3 IDFC LTD SR-3 7.5 BD 12NV20 01-Oct-2015 Transfer of Infra Bonds from IDFC to IDFC Bank Ltd.

But i am unable to sell them using ICICI demat as it says stock not traded in the exchange. Last traded price shows as 31sth March 2015.

How can i get rid of these bonds 🙂 ?

Thanks

I know this is an old article – though article mentions selling bonds in secondary market after 5 year lock-in, the tax treatment in such cases is not clear. The gains from selling in secondary market can’t be called interest – so, will this be treated as capital gains?

Yes .. thats the advantage of these bonds 🙂

I Have invested in it .20k for taxbenefit.

Fahad

Accha .. which tax bracket are you in ? You will benefit max if you are in 30% , if you are in 10% then it does not make sense

manish

Okk i got some stuff.Dtc applies from april 2012 meaning the year from april 1 2011 to 31st march 2012.Tax calculation will be done in accordance to DTC.

Hence investment in this bond after 31st march 2011 will be considered in accordance to DTC hence it will be EET model but ths year EET is not applicable and as mentioned in article investment for this year will or need to be considered in accordance to EEE model as investment was done before DTC came into existence.Thats the reason there are some articles saying not to invest in mediclaim according to tax constraint for next financial year.

Anyways doubt is clear and as said before ill invest elsewhere and giving the bond a miss.

Sohil

NO , its EET at the moment , the interest is taxable when you get it in hand , so its decided that its EET , nothing becuase of DTC here

Manish

Please reconfirm it manish(with some CA >i am also planning to check the same with my ca as i visit him coming month) agree its on EET basis but as mentioned by the CA in this article ,DTc is progressively applied and investment made in instrument before DTC sets are bound to continue on EEE line.

I was asking because on of my friend is keen to go for the bond anyhow.

Last night i was searching income tax site to get reference where it mentions 80ccf only gets EET but i wasnt able to find any such reference.

Sohil

You dont need to find much on this , its EET only at the moment and will be for the whole tenure , as menioned in DTC

Manish

Sohil

the rule with DTC is that , if a product will continue to get the same benefits as before the DTC for its full tenure , so if some thing is EET when you take it , it will continue to be in EET mode for that part . Which means Infra bonds are EET before DTC and hence if will continue to be so

Manish

Can you get me the link where it states infra bonds are EET instrument.

I was searching for same.

One link which i found out in support of the article is

http://www.incometaxindia.gov.in/archive/BreakingNews_RevisedDiscussionPaper_06152010.pdf

see page 6 and 7.Though only point missing is the section and instrument name.

A dig on the bond calculation by newspaper saying if same goes the calculation than sbi 9% return fd gives more than 19% return

Sorry for the pdf link but onsite the table is not there which is there in this pdf

Sohil

Thanks for the link . It would be of help to others

Again a problem.Now another article by a reputed CA have pointed out that investment in this year should be made as per DTC comes from next year so EET model wont apply and EEE mode of taxation will be applied and one should go with the bond.

http://www.dnaindia.com/money/column_new-infrastructure-bonds-window-may-not-open-again-after-march-31_1499116

Again i am totally confused.

Sohil

Nothing is there to be confused about , it talks about nothing different that what you know right now . So interest is taxable at the end , as its the rule at the time of taking . If you are in 30% bracket, I would suggest you can go ahead , but does not make a lot of sense if you are 10% or 20% , better pay tax and enjoy the the liquidity for next 5 yrs , use your 20k in a better way and you can make some more money

Manish

But does it mean whether tax which was getting accrued every year and which needed to pay at maturity wont apply and this will be treated as EEE model.

Also DTC applies from april 2012 so next financial year if any bond comes wont the same be under EEE application as that too came into existence before DTC date?

Just asking as a financial advice type.As i have already decided not to go with the bond.

Sohil

The Bonds come with two options , interest payout and accumulation , depends on which one you are choosing , if you choose “Payout” , then you get interest every year and pay tax on the interest every year , If you choose “acuumulation” , then all the interest is accumulated and you get it after 5 yrs and then you pay tax on whole interest that year .

Its EET , and will be EET only. Forget DTC

Manish

Paying a tax of 4,120 @ 20.6% or 6,180 @ 30.9% means that a tax-payer remains with 15,880 or 13,820 in his/her pocket. You need to earn approx. 25.94% (4120/15880) on 15,880 or approx. 44.72% (6180/13820) to reach to your original 20,000. Consider it:

Your Savings A/C. earning 3.5% will take approx. 7.4 years (for 20.6% tax bracket people) & 12.8 years (for 30.9% tax bracket people) to reach this figure. FDs @ 7% will take approx. 3.7 years & 6.4 years respectively. Equities @ avg. 15% will take 1.73 years & 2.98 years respectively. The list goes on & it leaves me wondering why the hell we are thinking so much in investing 20K to save tax, which is exclusive to only these Infra Bonds. So in 20.6% or 30.9% tax bracket I would surely go for it.

Found this link about the IDFC bonds. – a general review –

http://www.dnaindia.com/money/report_idfc-infrastructure-bonds-face-tough-run-again_1495911

Still trying to get my head around all the calculations!

Thanks, Manish, for the article, and to all the others too for all the insights.

This is a most enlightening site.

Sudha

If you dont understand it , thats ok . Ask here what are your questions ?

Manish

Thanks, Manish. Appreciate. But, on second thoughts, think I have some better uses for whatever monies to be invested. So, have decided to give these a miss now.

Sudha

thats a great thing , Infact its a good move ,better use that 20k in next 5 yrs , rather than lock it for tax saving of 4k (assuiming you are in 20% bracket)

Manish

Instead of going into the Rs and paise calculation do see if you can buy this.

1 Does every one need asset allocation in Debt? Yes.

2 Which are the best debt instruments ? EPF and PPF but there are limits to how much one can invest.

3 If asset allocation necessitates some more investment in debt what are the avenues available which also give tax benefit beyond the 80C limit? Infra bonds.

4 Is investment risk free.? No investment, which gives you some return, is risk free. The return is compensation for the risk taken. Even if you keep money at home, it has the risk of being stolen besides the silent thief i.e Inflation”

5 So if one wants some more tax deduction beyond the 80C limit infra bonds are the best option.

I absolutely agree with you here.. People should not lose their sleeps over this.. People should cultivate money saving habits, cut on their discretionary expenses as much as possible, do their investment planning & tax planning right from the beginning of the financial year as its as important as earning money etc. etc… the list is endless so stopping here.. & No Offence to you Manish.. 🙂

Shiv

Yea .. agree with your point that they should plan for taxes from advance of the year .. good point for you . Keep adding valuable comments 🙂

Manish

Hey Manish.. Sir I’m also a very big supporter of “Building the Nation by Paying Taxes” but I favour Tax Saving & am strictly against Tax Evasion. Basically its only the Govt. which makes these provisions & its completely legal. Moreover, “A Tax Rupee Saved is a Tax Rupee Earned!!” & gives more pleasure than a Rupee earned.. 🙂

Shiv

You are getting me wrong here . I am also against tax evasion . All I am saying is not investing money just for the sake of tax saving and better pay the tax to the govt . Many people are there who are so mad about tax saving that they compromise on the returns , liquidity and their comfort .

People who need 20-30k in next 2-3 yrs are also investing money in Infra bonds and other tax saving funds . Tax saving is secondary thing , first one has to see his liquidity and other comforts . One can NOT save in tax saving funds , save the lock in period and can use that money in better way

Manish

I agree with you that a person should first save tax u/s. 80C & then in order to save further tax u/s. 80CCF, he/she should invest in these bonds. Whether a person should invest in FDs or ELSS or NSCs or save tax through any other way u/s. 80C depends on his/her “Risk Profile”, “Asset Allocation” or personal preferences.

Coming to your point that people should pay taxes first & then invest the money somewhere else. I dont know what all investment options you suggest people to invest here in & how much returns are there in your mind. Personally I wont do this, especially if i fall in 30.9% or 20.6% tax bracket. I think EPF is the best Tax Saving “Fixed Income” product available to a person in India (limited to Salaried Class only) followed by PPF, Senior Citizens Savings Scheme (limited to Senior Citizens only), NSCs & so on. Sorry if i missed something here. As far as investment in Equity or Real Estate or for that matter Gold is concerned the returns are surely greater than the fixed income options but they do come with their own things attached to them like risk, volatility, illiquidity, impurity, high investments and so on & so forth. Everybody knows how much uncomfortable Indian people are in equity markets. One cannot invest Rs. 20,000/- (or Rs. 1,20,000/-) in any Real Estate investment at least in India as Real Estate MFs (REITs) are still to become operative here. Then comes Gold. History shows Gold investment barely beats Inflation & is a hedge against it. Though, in the long term, an investment in Silver always outperforms Gold investment by quite a huge margin. Its only in the last few years that the Gold (or Silver) has beaten every other investment, thanks to a prolonged slowdown in U.S. So here I want to say if I’m making 12%-14% safe returns by investing an additional Rs. 20,000/- in these bonds & saving tax u/s. 80CCF exclusively reserved for these bonds then I whould surely go for it. Rest, obviously, depends on the person who want to invest & personal opinions, as these were only my opinions… 🙂

Shiv

Thanks for putting your views . My only point is that one can also think of paying the tax and not saving it .

Manish

Hi Manish

Manish people invest in Fixed Deposits which give 5%-8% interest for 2, 3 or 5 years and after which they need to pay tax also on the interest or TDS gets deducted automatically. These Bonds have a lock-in period of 5 years after which you can either redeem them back to IDFC or sell them on the stock exchange. If I invest 20,000/- & save 30.9% tax at one go, it comes out to 6.18% per annum (30.9%/5), without any other thing being considered in the calculation. If I fall in 20.6% tax bracket, it works out to 4.12% and 2.06% in the 10% tax bracket. When I consider the return of 8% interest also, the yield goes higher. So I dont find any reason for me not to invest in these bonds for tax saving. Though as a pure investment, I do believe there are better products available like MF/SIPs & SBI kind of bonds which SBI brought in October 2010 giving 9.5%/9.25% interest and got oversubscribed 17-18 times on the first day itself.

(Note: The calculation are done to make it as simple as possible.)

Thanks & Regards

Shiv Kukreja

Shiv

Ok , got it .. However for a person who has still not completed exhausted 80C , but still wants to invest in these bonds , it does not make sense , a tax saving FD would be a simple choice . What do you say !

Another point is “not investing for tax saving” can also be a wise choice ! , this 20k extra tax deductions has made people so much that they are not considering what all they can do by not investing the money , paying tax and then utilizing this 20k in some other way in next 5 yrs !

Manish

Hi

I’m an Independent Financial Advisor based in South Delhi. Currently IDFC Infra Bonds are up for subscription and closing on February 4th. I think Infra Bonds are a good investment option as they offer tax deduction u/s 80CCF on an investment of Rs. 20,000 over and above Rs. 1 lakh deduction u/s. 80C. The tenure of the bonds is actually 10 years but after 5 years of lock-in period you can either redeem the bonds back to IDFC, which is called a buyback facility, or sell these bonds on stock exchanges. The bonds carry a coupon rate of 8%.

Shiv

I am not very much convinced with the statement “I think Infra Bonds are a good investment option as they offer tax deduction” . WHY ?

Manish

Sir , I don’t understand how the yield calculation for different tax slabs has been done for the different options of this Bond . Please can you show the working in detail .

Jignesh

Which return are you talking about ? 7.5% is what company is offereing .

Manish

thanks for this useful info and fruitful discussion.

In my opinion if u r in 10% tax slab, then PF is better option as now the interst on it 9.5% and the return is also not taxable. If compounded this 9.5% then tt will be more than the effective return gained by infra bond.

Yes

Agreed with you 🙂

Manish

@Gaurav,

Just be aware that the 9.5% on EPF is only for this year as a surplus was “discovered”. There is no saying that the interest will stay the same and not revert to 8.5% from next year. Read the article http://www.caclubindia.com/forum/epfo-interest-rate-9-5-for-2010-2011-104575.asp

SBI retails bonds are much better than Infra Bonds (except for tax saving) . Any comments from your readers on latest SBI bonds. I would like to know what will be the expected traded price of these bonds on NSE.

Sundar

As SBI bonds are not for tax savings , even if their interest rates are bit higher, they would be giving almost the same net yield (net return) to the investor .

http://www.onemint.com/2010/10/14/sbi-bonds-issue/

Manish

Dear Manish,

Today I asked my Stock Broker if he will accept SBI Bonds which will be credited to my Demat account as collateral for my trading. He could not understand initially. Then I explained to him that presently some NCDs like Tata Capital, L&T are trading in NSE under cash section. After some investigation he replied saying yes he can accept these Bonds for Margin requirement. That was a good news. It is like keeping your fixed deposit and trading in Stocks and F&O.

SUndar

Good to hear that 🙂 , but at the end , how does it matter , you are putting it as collatral , ifthings go wrong , you will have to liquidate it anyways ..

Normally brokers want margin money for stock futures of about 20% of the value and 15% for Index Futures. They accept presently stocks and hard cash in your account as collateral. Bonds were never accepted as collateral as they cannot be liquidated easily etc. Presently only very few NCDs are traded on the NSE and volume of trade is very low. But SBI has stated that they want to create a vibrant secondary market for their Bonds. However many Brokers are not accepting this view. I think SBI Retail Bond will change all these hopefully. But I was happy to get “in principle” approval from my broker. In case of default he can always take those bonds and do whatever he wants with them. But getting him to accept it for margin money leaves me with more cash to trade. That is my point.

Sundar

Ok got your point now , but just make sure its on paper that they will accept it , just saying that we will accept on email or phone is not recommended

Manish

L&T also offers infra bond….

as per the one of the site…

>>> L&T Infra has got approval from the competent authority to make investors able to purchase its bond even without having demat account. <<<

Thank you.

Is it advisable to invest more than 20k in this bond???

Thanks

Raja

hmm..

I dont think so , whats the point in investing more than 20k , because your tax exemption is limited to only 20k .

Manish

Thanks Manish…

Hi Manish,

Being a Layman to terms like CAGR, IRR etc, this is how I look:

If you invest 20,000 in bond you will get 20000+X-Y where X is the interest and Y is tax applicable.

Assuming you fall under 20% bracket, then pay 4000 as tax this year and directly invest the remaining 16000 in ‘IDFC Shares’ (with a risk associated).

I think by all means we would recover 20000+X-Y after 5 years especially by mitigating the risk to a certain extent by investing directly in IDFC itself.

Do I sound convincing? 🙂

Regards

Sunil

Sunil

Looks convincing and great 🙂

Manish

I also want to invest in IDFC Infrastructure bonds but I wont have any demat account. Is there any other procedure of Investing in IDFC Infra bonds, if yes, then kindly guide me and suggets me

Anoop

No , you need to have demat for this

Manish

Actually, applying for the bond in physical form is possible. Check the IDFC website for details at http://www.idfc.com/infrastructure_bonds.htm

Srinidhi

Great, I have included this info in the main post , with a thanks to you 🙂

Manish

Manish,

Here’s what I think: http://www.vinayahs.com/archives/2010/10/12/investment-strategies-idfc-infrastructure-bonds-a-simple-way-to-decide-whether-to-invest-or-not/

Most of the analysis that I’ve seen on the web talks about yields and such. Jargon that doesn’t actually help you make a decision. 🙂

Vinaya

This is good 🙂

Hi,

I have been evaluating the 5 year option and following is the data point i got.

–> 5 YR CUMULATIVE OPTION

Tax Slab 30 20 10

Investment 20000 20000 20000

Tax Saved 1st year (A) 6000 4000 2000

Annual Compounded Interest Earned in 5 yrs (B) 8713 8713 8713

Tax on int ( C ) 2613.9 1742.6 871.3

Total Earned in 5yrs (A+B-C) 12099.1 10970.4 9841.7

CAGR 9.92% 9.14% 8.33%

–> 10 YR CUMULATIVE Option

Tax Slab 30 20 10

Investment 20000 20000 20000

Tax Saved 1st year (A) 6000 4000 2000

Annual Compounded Interest Earned in 10 yrs (B) 23178 23178 23178

Tax on int ( C ) 6953.4 4635.6 2317.8

Total Earned in 5yrs (A+B-C) 22224.6 22542.4 22860.2

CAGR 7.76% 7.84% 7.92%

An equity diversified fund like HDFC 200 will provide better returns and liquidity options is my opinion.

Great

Thanks for the calculation , is it easily understood by others ?

Manish

All calculations in comments section are doing a basic mistake, you are taking the savings on Tax in first year as the net savings and adding the interest of subsequent years.

This is wrong, to get the effective yield.

The savings in first year will also earn a interest (if invested!).

So, the calculations should be as follows:

Assuming 30.9% Tax slab.

Total investment: 20000

Tax Saved: 6180

Net Amount Invested: 13820

Total interest for 5 r at 7.5% – 8713

Tax on Interest – 2692

Net Interest: 6021

Therefore for money invested of 13820, we get 26021, which is Yield of 13.49%, which is quite good.

Thanks

Praveen

Praveen

thanks for the calcualations

Thanks Praveen. You are right.

One point missed in the calculation, 6000 saved in the first year itself,

it can be re-invested again, which will again add to my total income(interest).

Column 1 : Capital Invested – (100- 30% tax) = 70

Column 2 : Interest – 8% per annum

Column 3 : “Interest after tax” 8*0.7 = 5.6%

Column 4 : 30 Rs distributed over 5 years, effectively getting 30 Rs in end.

Column 5 :”Effective interest yield” ( 3+4)

Column 6 :”Effective interest yield before tax” (5)/0.7

1 2 3 4 5 6

70 8 5.60 3.79 9.39 13.41

8 5.60 3.79 9.39 13.41

8 5.60 3.79 9.39 13.41

8 5.60 3.79 9.39 13.41

8 5.60 3.79 9.39 13.41

8 5.60 3.79 9.39 13.41

70+30

——————————————————–

Putting 3.79 per year for 5 years @8% interest rate gives you 30 Rs in end.

“@8%”

0.00 3.79 4.09

4.09 3.79 8.51

8.51 3.79 13.28

13.28 3.79 18.43

18.43 3.79 23.99

23.99 3.79 30.00

I am not understanding what is all this !

Manish

Please. Can some expert provide detailed calculations for a person in 30% Tax Bracket. As it seems SIMPLE calculations will make decision taking Simpler. Regards

Raj

If one is in 30% bracket , then invest 10,000 would mean that you first save tax of 3,000 as you would have paid that if you had not invested in the product ,now what ever you earn in 5 yrs ,that will be again taxed at 30% (provided you are in same bracket).

Manish

Kindly Check Manish,

1. Effectively invest <Rs. 14000/- get Rs. 7500 (@7.5%pa X 5 yrs X 20000)

2. Again pay Income tax of 30% on 7500 = 2250 + serv tax etc. = 2250 + 250= 2500

3. Invested 14000/- got 25000/-

4. i.e 12.3% Compounded Interest vs 8% from PPF etc. or 15.7 Simple Interest vs Bank's FD

Raj

How you got 25000 by investing 14k ? Not sure

You got 7500 only and tax is 2500 so just 5000 you got as profit .

Manish

1. Dear Invested Amount is Rs. 14000/- But Bonds are worth Rs. 20000/- and

2. You get Return of of 7500 – Taxes say Rs. 5000/- SO YOU WILL GET 20000 + 5000= 25000/- by investing 14000/-

3. i.e 12.3% Compounded Interest vs 8% from PPF etc. or 15.7 Simple Interest vs Bank’s FD

i will not invest, because my debt exposure is already high and i don’t have much room in category.

Cheers

Marshal

Marhal

‘

Makes sense , in a way thats portfolio rebalacing , good one 🙂

Manish

I would be more comfortable investing when LIC comes with the infra bonds.

LIC hai to kahin aur kyon jaana :)-

I dont have good investment in debt stuff(almost all in MF and stocks) , so i would probably go with the infra bonds just to have something safer.

Mithilish

I am sure they would come up with the bonds only after december , they dont mess up with the timings and take Bharpur Fayda of the trust they have created over the years

Manish

Hi Manish,

In your table Cumulative Option is showing YES in Series 2 which is wrong.

Please Rectify it.

Cheers

Amit

Why do you think its wrong , I guess its correct . http://www.idfc.com/infrastructure_bonds.htm

Confirm please .

Manish

MiSS IT … for all

Bonds are always Baa….. They are no good, we can keep the same in Bank FD for 5 year lock-in Period and earn the same returns and tax benefits.

IFCI had defaulted previously in its Bond Maturity. Ten year is long thing with Bond’s Fund Dedicated only to Infrastructure is quite risky too.

There is no soverign gurantee in this Bonds…but we have in Bank FD’s upto 1 lac.

Choice Apna Apna..

Happy Investing.

Vinay

Yes, these bonds do not have much juice like other products , but what about investors who want to save extra tax than their 80C limits ,for them any choice would not make sense .

Comments ?

manish

Hi,

Manish

The 20,000/- Limit other than that of 1 Lakh exemptions in not quite appealling & commited for most of us and its also for only for 1 year. It should be extended upto 5 years.

And again there is No Gurantee on this Bonds which is concern becasue its dedicated to only Infra Sector and Projects. History says that Sectoral fund or Bonds are Risky.

If sectors or companies starts defaulting on their payments after couple of years then we will be in trouble from this Bonds.

For saving additional 30 % on tax we are risking the 100 %

This Bonds are like 70 MM Big screen films which make most noices and do not gurantee the Performance.

MIND IT !!!!!

I am unable to understand the calculations indicated under the comments section as well as in the table being advertised by IDFC in various newspapers.

It is very clear that the interest payable on this bonds is taxable and this taxataion shall be at the same rate as applicable to the individual’s tax slab.

So if a person in 30% slab invests some amount say Rs. 10000, he is effectively investing only 70% (or Rs 7000/-) as he saves 30% income tax which he would have paid had he not invested this Rs 10,000/- amount in IDFC bonds.

But at the same time the interest payable to him (say 7.5% annual option) will be taxed at 30% rate and so the interest yield too reduces to 70%. As the effective investment is 70% of actual and same is the case with the interest earned on this investmet, the effective interest yield remains the same i.e. 7.5%. Can somebody confirm if my interpretation is correct?

Hemant

Hemant

The IDFC and other newspapers try to show the retuns are 12-15% pre tax , they consider it assuming the tax not paid or they are including the tax saved in the calculation and showing it as part of return , because even that is in a way return for investors , but then all the products can be shown to give those kind of returns .

Manish

I would like to draw attention for going in series 3 & 4.

if you want to go for buyback, there is time limit for intimation. the intimation is to be made on specific period during three month before the end of five year.

Once you miss them, then you have to wait for 10 years to complete. – Please correct me if i have wrong interpreted the literature.

In this comparision IFCI bonds had buyback period on every year 6th to 10th year. Further the return in buybak option were 7.85% though it was not secured. Again in coming month interest going to rise as market is going very healthy so you can wait till december – you may get better option may be from IDFC itself as they will also come with second issue as well.

Expecting feedback on this from the knowledgable people

Krunal

thanks for the info , from where did you get this info , if that is the case , people investing in 3 & 4 series can look at IFCI bonds

Manish

Thanks for the post, was thinking to invest in these funds.

Not sure which option should opt for Series 1 to 4.

Rakesh

Rakesh

All options and pros and cons are there, its not a tough thing now to choose , whats blocking you ?

Manish

After 5 years DTC will kick in. The Tax slabs will be different to present. The interest earned at end of 5 years in cumulative options would be most probably be accomodated in resonable slab for most investors. Hence interest income is not a big issue.

Those going for Series 2 should note that presently NCDs which are traded on the stock exchange are quoting at present market yield. So if this option is traded on the exchange then if the interest rates rule higher than 8%, then the investor will face capital erosion if he sells in the market. Hence this option is very risky.

In my opinion the best option for investor is Series 4. After 5 years give it back to IDFC and include the cumulative interest in your income under DTC and hope that tax slabs will be revised.

Sundar

Sounds like a right thing 🙂

Manish

if govt wants my money. It should give me more incentives.

Sorry i am not interested with this offer. not investing in these bonds, period:).

Are the returns earned in the bonds also taxable? I dont think so.

As per my calculation, the yields are around 13% for people in 20% bracket and around 17% for people in 30% bracket. I have assumed no taxation on the interest earned.

Sandeep

Its taxable , all the debt products apart from PPF and EPF do not enjoy EEE unless stated otherwise

Manish

Srikanth

Sure man 🙂 , we are not forcing anyone 😉

Manish

Nice Article.

However, my view is as follows :

Investment Done : 20,000.00

Tax saved : Around 5-10k

Lock In Period : 5 Years.

Interest given : Lets say 7%

So, in this case, we get around 28051.0344 at the end of 5 years.

So, total saving : 28051 + 5k = 33k.

Now, Interest earned : ~ 8051.

Tax applied [ lest say 20% ] = 1600/-

Net saving : ~ 12k.

which is almost 60% profit in 5 years, which is way good.

Might be my calculations are little wrong.. But overall, i feel that this investment is a good one.

i second that.

Per year calculation also if we do , we tend to get good returns on 20k invested per year.If you fall in 30% slab , 30% directly saved per year ,on 20k invested + interest earned i.e 38 % per year.

Now tax on interest earned i.e 30% of ( 8% interest on 20k) = 30% of 1600 = rs: 480

tax saved : 30% of 20k = 6000

interest earned = 1600

– tax on interest = -480

——————————

rs 7120 earned on 20k per year i.e 35.6 % pr year

I am not sure about calculations that are going in here..From my perspective is it worth a miss to 10%(i am in here) tax slab guys? Lets see

Investment 20000 and save tax of 2000

Let me choose Series 2 which is cumulative and 8%

my return is =29387

After tax on interest=27000(approx)

Saved 2000 in Mutual Fund with conservative return of 12%

Return=3525(tax free)

Total Gain= 7000+1525=8525/-

Net return =28525/-

Assume not invested it and payed the tax.

Hence 20000-2000(tax)=18000/-

Invest in Mutual Fund(Equity Diversified) with average return of 12%.

Return =31722/- (no tax )

Gain=11722/-

Assume if MF(Equity Diversified) returns just 10%

Return=28989/- (no tax )

Gain=8989/-

Any use for guys like us..i don’t think so!.

Prabeesh

How many years of calculation have you done ? I assume 5 yrs .

The only thing which is missing in ELSS option is the stability which the bonds or any other debt option provides , you should be mentioning that 🙂

manish

Chetan

Without commenting on your calculations I would say try doing the same thing for ELSS , PPF and BankFD (5 yrs) , What do you observe ?

Manish

Roopesh

60% in 5 yrs is 7.5% per year compounded . Is that what you feel is good ?

Manish

I would give it a miss. This is because, 5 years lock-in is too long . Better would be to forgo the tax, and in that period, invest in a balanced fund. I am sure that balanced funds in 5 years time would give more returns. Even NSC or for that matter, VPF would be more fruitful.

Thanks,

Shantharam

Shantharam

Why not , if it makes sense for you , then go with balanced funds . How confident you are in saying that balanced funds would beat these bonds in next 5 yrs from today ?

Manish

I would say to look it at from the prespective of other AAA rated bonds in the market. Obvios, that is tax-exempte bond. But if we some data (preferably avergae) of corp AAA rated bond whcih doesnt give tax-exemption and then deduct the factor of tax-exemption, that should have beeen the interest or the yield on this. Isnt it? Arbitrarly fixing (or not haveing the base of 7.5/8%) is the issue here.

Abhishek

You might want to explain more on this in layman terms, i dont understand much of it

Manish

I wonder why NRIs can’t invest in these bonds. I have been given to understand that as an NRI I am not allowed to invest in some instruments viz. KVP, NSC, Post Office Deposits and even PPF. I think that the Government should find a way to allow the NRIs invest in these instruments using their funds from NRO accounts.

Venshu

hmm.. are you too keen on these bonds ? You have other opitons which you can explore .

Manish,

Not that I want to invest in this particular Bond (20,000/- tax saving is actually not too bad if I am in the highest tax bracket). The point is why are NRIs being discriminated against? If the Govt. is conccerrned that relaxing the rules could lead to Foreign Exchange violations or something like that then the rules can be revised in such a way so as to prevent suuch frauds and at the same time allowing NRIs to invest in certain Debt Instruments using funds from NRO accounts.

I actually don’t mind investing in PPF – While 8% asssured returns is just about OK, what I like is the EEE part. I have read and heard people saying that NRIs can invest in PPF but everytime I inquire with Banks, I am told no.

Can someone please throw more light on this matter please?

Venshu

Regarding these bonds , its govt who will have to give clarity on why its not allowed .

For PPF , its simple for NRI’s , they are not allowed to open and invest in “fresh” PPF account ,if one had PPF account before becoming NRI , then then can continue paying the PPF premium till maturity .

Manish

As a NRI, you CAN invest in PPF. This is not right topic to go inside, but explore more. You got number of options.

@ gopal,

Please throw more light on NRIs being allowed to invest / NRIs can invest in PPF. Manish has clarified above that NRIs can not invest in PPF and this is what I have been given to understand from a lot of others. I am really curious now and will be more than happy to open a PPF account and start investing if there is a legal way to do so!

I recently came across an interesting interpretation for NRIs investments in PPF, KVP, NSC etc. Those NRIs who get income from Indian Investments and are paying taxes in India, can invest in PPF, KVP, NSC etc. to reduce their tax liability in India. Only those NRIs who do not pay taxes in India cannot invest in above instruments. Please get clarification from some well informed expert on this. I was also shocked to hear this interpretation. But it sounds logical considering that both Residents and NRIs have equal rights before law to legally reduce their tax burden.

I came across an interesting case on NRO account. Here again some expert opinion was that as long as NRO account is not misused for siphoning money out of India, there is no need for the NRI to designate his resident account as NRO. It will not be treated as violation of law. It seems RBI knows that many NRIs use resident accounts without designating them as NRO. But if the Resident account is misused under FEMA then it is not acceptable. Hence please check this matter with some expert.

Sundar

Not sure about your reasonsing for PPF , look at my reply to venshu

Manish

Manish,

You are probably correct. But I wanted to mention that All investments for NRIs are governed by definition of FEMA and not Income Tax act. FEMA definition is quite different from IT definition. So far RBI has not brought any clarity on FEMA regarding this.For example if somebody can prove that in the previous year he stayed in India for more than 182 days and then went abroad for a definite period with total intention of coming back, then most probably he is Resident as per FEMA and he can open a PPF account although he is abroad. But I am not an expert on this matter. But I know RBI has not brought forward a single case before Courts till date. Income Tax people do not care for FEMA, they go by their own definition of NRI and only bother about Tax due.

Sundar & Manish,

This is getting really interesting now. I file my tax returns using TaxSmile website – thier services are excellent and so is the ease with which the returns can be filed! – and hence do not have access to a CA / Tax Consultant to clarify the subject points. I really wonder how I can learn more about this matter. Any help from fellow JagoInvestor readers is welcome.

Dear Venshu,

I suppose you had sometimes applied for Mutual funds or PO savings schemes etc. You will always find a small box where you have to tick choices like Resident Individual or NRI or NRO etc. Then you have to provide foreign address for NRIs etc. Have you ever thought this requirement comes not from IT rules but from FEMA rules? If RBI was so severe on FEMA then millions of illiterate Indian workers working in Gulf etc. can be prosecuted as most of them even don’t know what is NRE or NRO etc. They just send money to India and it goes into the system as Residents only. Even Banks don’t know the nitty gritty of FEMA. Basically as long as money keeps flowing from abroad no body cares for FEMA etc.Even RBI does not care it seems. But reverse flow is sensitive as far as RBI is concerned. They are more careful on this. This is my personal opinion.

Sundar,

Quite an interesting school of thought. I want to dig more on this issue and see how I can make it work to my benefit – without breaking any rules of course!!

Venshu & Sundar

I have started a thread on this on forum for members to discuss : http://jagoinvestor.dev.diginnovators.site/forum/fema-rules-for-nris/378/

Manish

not investing: because of unfavourable opportunity costs.returns are <10%.far less than EPF returns.the tax on interest is a bummer.5 years is a longish enough period for even the stock market volatility to be taken care.

my debt investments are mainly VPF.currently these bonds are highly unattractive .no marginal improvement either in risk reduction or return enhancement to my porfolio. gonna give it a wide berth.

Pravin

Ok , seems like the best thing for you would be to avoid it .

Manish

Hello,

I think it’ll be beneficial for those who’re in 30% tax slab. For those who are on 10% slab, looking at so much of lock-in period & rising inflation, it will not be much beneficial.

Gopal

Agreed , for people who are not too keen on more debt and security , they can give it a miss .

Manish

I THINK THAT IF YOU INVEST IN BANK FD AT 9 ~9.5% pa & PAY TAX ON INTEREST, THE POST TAX EARNINGS WILL BE SAME/BETTER THAN THE BONDS(INCLUDING THE 80C TAX REBATE), DEPENDING ON YOUR TAX SLAB.

PLUS THE LOCK IN PERIOD OF THE BONDS……

MARGINAL CASE, NOT WORTH HOLDING FOR 10 YEARS !!!!

Kumar

Yes what you say makes sense , the different is not very high , but it can be .5% or 1% or even go upto 2% , which can be phenominal for some people .

Manish

I agree with you.. 10 years for maturtity and 5 years locking period… too much.

Interest earned on this at maturity is TAXABLE.

So it is complete NO

its best for high tax slab individuals – go for the buyback option ….the IRR for a buyback option after considering int payout every year and taxed at max rate is a healthy 15% post tax return….definitely recommended