Don’t buy “Return of Premium Term Plan” – It does not make sense!

POSTED BY ON December 22, 2020 COMMENTS (262)

Does it makes any sense to buy “Return of Premium Term Plan”?

The one-line answer is “NO – it does not make sense”

A “Return of Premium Term Plan” or TROP as its called – pays back all your premiums at the end of the period, whereas the plain term plan doesn’t return back anything. Before we get into the analysis further, I want you to know why these return of premium term plan came into existence!

Why the Return of Premium Term Plan came into existence?

Term plans have become very popular in the last few years. We are seeing so many advertisements screaming about term plans importance. However, a lot of investors who don’t understand term plans fully, still feel a pinch that their premiums get “wasted” if nothing happens to them.

They equate “paying premiums” as “losing premiums” if they dont die. They compare it with an investment policy (read traditional insurance plans) where they get back there a sum assured towards the end of the policy.

Insurance companies sensed this behaviour and they introduced something called “Term Plan with Return of Premium” which can now proudly tell customers that they have nothing to lose. They get claim money on death, and if they don’t die, they get back all their premiums paid. Many investors who do not understand the time value of money concept fall for a product like this, as to human mind “getting back all your premiums” sounds very attractive offer.

Now, let’s talk about why it does not make sense as a product.

Return of Premium Term plan has an extremely low return

The premium for the TROP (return of premium term plan) is higher than the plain term plan and it can be 2x-3x times the normal premium in some policies.

So basically, you are paying an extra premium for getting your premiums back after 30-40 yrs!

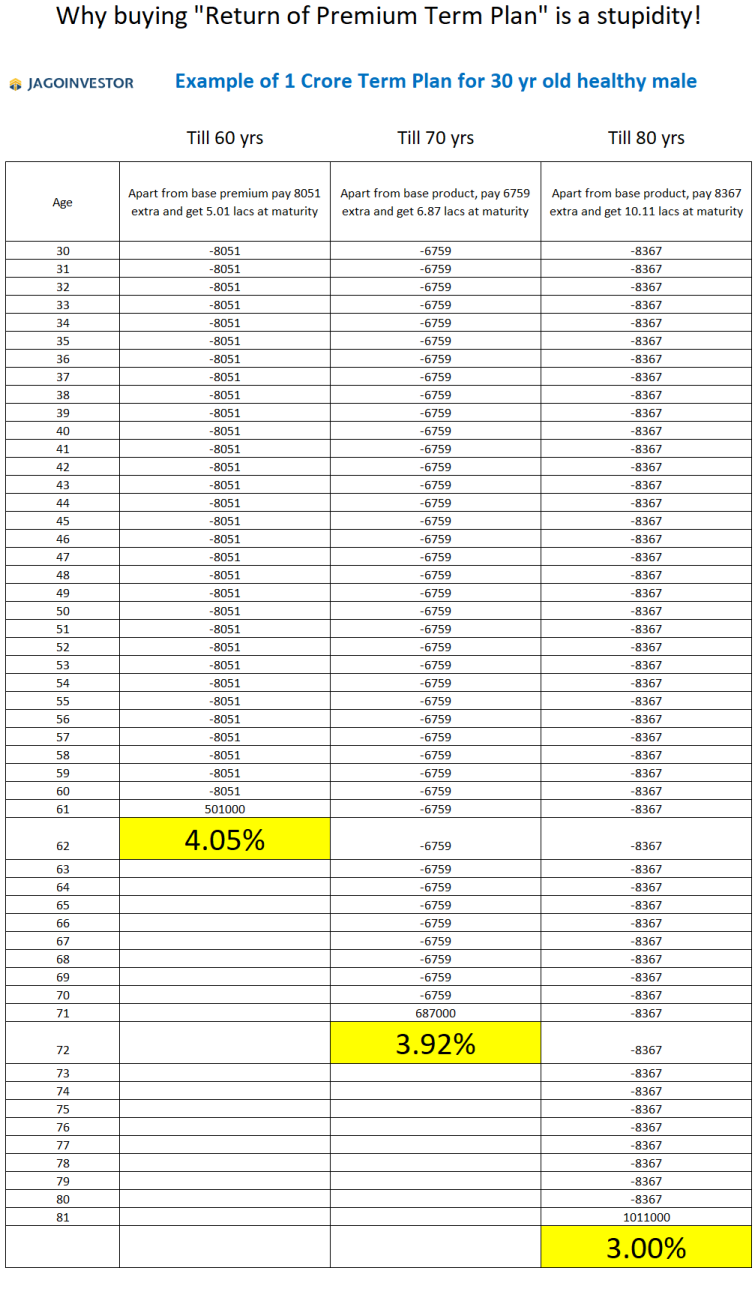

Let’s look at an example of a 30 yr old male, who wants to buy a 1 crore term plan till 60 yrs of age (for 30 yrs tenure). In which case the premiums are as follows (Example is of Max Life Term Plan as on 21st Dec 2020)

| Type of Plan | Yearly Premium | Details |

|---|---|---|

| Simple Term plan | Rs 9912 | One has to pay Rs 9912/yr for 30 yrs for Rs 1 crore cover. You don’t get back anything at the end on survival |

| Return of Premium Term Plan | Rs. 17,969 | One will have to pay an extra amount of 8057 for 30 yrs (apart from 9912) and will get back Rs 5.01 lacs (this is all premiums paid excluding the tax amount) at 60th year |

If you look at the example above, you can see that in both the plans you are paying Rs 9912 for the Rs 1 crore cover. Only difference is that in second policy, you are paying an extra Rs 8057 to get back Rs 5.01 lacs (excludes the taxes part) at the end. This is the only difference between the two versions.

So internally, the term plan with return of premium is simply a bundled product of a normal term plan and an investment policy. If we ask what is the return of this investment policy where you are paying Rs 8057 per year and getting back Rs 5.01 lacs after 30 yrs.

The answer is 4.05% CAGR.

Yes, its barely above saving account rates and a little below a normal fixed deposit interest.

I did the same analysis for the tenure of 40 yrs and 50 yrs policy (read why you should not take such a long tenure term plan) and the IRR return was 3.92% and 3.00% respectively, which means that if you buy the policy for a longer tenure, the return gets lower and lower and the product becomes even worse.

Below is the IRR return calculated in an excel sheet for your reference

Note : The above calculations are done in Excel for just one company plan, however similar kind of numbers are expected from other companies return of premium term plan. Please do IRR calculations yourself if you looking at other companies plans.

Return of Premium Policy ties you up with the product

What do you do, if you want to stop a “Return of Premium Term plan” in-between? Let’s say after 10 yrs?

It will not be as simple as a normal term plan, because, with the return of premium policy, your mind will tell you that you just have to continue it for another 20 yrs and you will get back all your premiums. Very smartly, the insurance company has converted a pure term plan into an “investment policy cum term plan” with very bad returns.

so the better alternative than a “term plan with return of premium” is to buy a simple term plan (here are 20 checklists before buying term plan) and invest the extra amount in another investment products like PPF, FD’s, Equity mutual fund or debt mutual fund and you will have better flexibility and returns.

Check out this video from Subramoney talking about this product

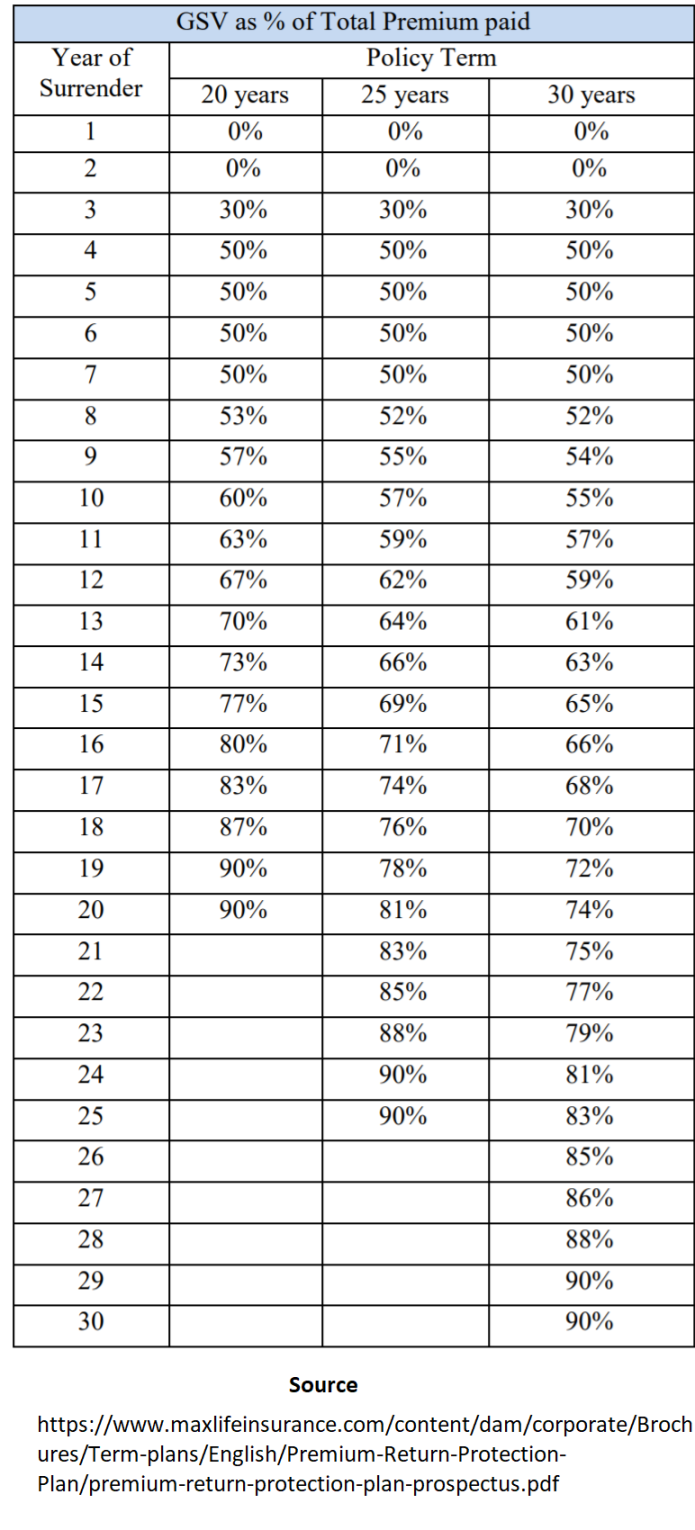

What happens if you stop paying a premium for Return of Premium Term plan?

There is an option to get a surrender value if you stop paying the premiums in between. Just like traditional plans, there is the concept of “Guaranteed Surrender value” in these kinds of policies which comes into picture once you have paid 3 yrs premium. However, the amount you get back is a fraction of what you have paid. There is a percentage assigned for every year which tells what part of the premium paid will you get back if you surrender the policy in a year. Below is a snapshot of the chart taken from Max Life Brochure

So, as per this chart – if one wants to surrender the policy in 10th year, they will get back only 55% of the premiums paid (excluding premiums).

Some other Info

- The TROP gives you income tax benefits as per sec 80C

- There is an option to pay premiums on a monthly, quarterly or yearly basis

- There is also an option for limited pay (pay in 10 yrs) or in one single premium

Conclusion

So TROP is a very carefully designed product which favours the insurance company but makes the product look very good and works on the psychology of the investor. Better stay away from it. The best idea is to buy the simple term plan with the lowest premium.

If you have already invested in this kind of plan, then you need to evaluate what will make sense for you!

Do let us know if you liked the article and does it make sense to you? Share in the comments section!

pleas review “IndiaFirst Life Long Guaranteed Income Plan” in some post

Avoid!

Thanks for sharing some of the great and informative insight into the term plan. Keep up the great work.

Thanks

HI Manish,

Thanks for the article..I already have SBI E -Shield term plan of 50 L for 30 years and paying since 2014 onwards & it is wiser to have another term plan probably for another 50 lakhs… please suggest

Yes..

But its better to take a single 1 crore term plan now if costing is fine .. and close the old one!

Manish

Sir, I m confused I m invest in term plan or mutual fund plz suggest me .

You dont INVEST in term plan, its for your life insurance purpose. You can invest in mutual funds for long term

Do one thing , just leave your details here and our team will call and guide you http://www.jagoinvestor.com/pro#schedule-call

aergon ireturn plan.. for 20 years if i invest 11459 rs for a cover of 50 lakh.. i get my premium returns 11459 -112 rider – 15% service tax multiply by 20 = 223540.)

now term plan comes to around 4405, but for others its 6-7k.. so i invest remainder in tax saver FD every 5 yearly for 4 times.(20 years) i get 240000, around 15k more than investing in this plan while 220000 if i invest in other term insurances..

so ultimately its almost the same thing.

Hi sid

I am not clear on what is your question. Please repeat it with more clarity

Manish

Hi Manish,

Thanks for the well written article. The example you have given above is just for 12 Lakhs. What happens if the minimum sum assured is 1 crore? Will we still be able to compare the PPF+life term option.

the example is still applicable ..

Hai Sir, I have Jeevan Taran Policy. i have started by 2012 Feb up to now i have paid regularly.Now after gone through your articla i am scaring to continue my policy. I have a doubt if i complete my tentur i.e 20yar at the end how much money i will get . i thought full sum assured (600000) + Additional Benifits i will get after the completion of 20yrs .But you have mentioned in that artical only special assured only i will get afte my accumulation period.Sum assured after my death only it will come or after the tenture it comes to me….please guide me sir……

Yes, as I mentioned only what is written in policy documents will be done

hi Manish,

I have simple question for you on this, I think you have posted in some other post about the tenure of the term plan. if you know(high probability) that you are going to survive more than 70 years of age then take cover only for years when your family is dependent on you(for income purpose) i.e. till 60 years. so if I already investing in ppf & mutual funds already then would it be better that I go for term plan with return of premium? I understand I would be paying more but as you mentioned anyway I am going to survive full term of the policy so I would atleast get my money which I gave to insurance company. Is it correct way of think?

Please advise as I am planning to buy term insurance with rop in next couple of days.

Thanks

Sameer

No Sameer

Its not correct way to think. You are not taking into account VALUE OF MONEY concept. The money you will get after the full tenure, just think how much it will be after 25-30 yrs , it would be peanuts at the end and at that time, it will not help you at all .. So right now just go for normal term plan and any extra money use for investments.

Manish

Hi Sameer,

Simple explanation to your query would be value of money decreases as the time passes because of inflation, this concept is called time value of money.

For example, just compare the purchasing power of a 100 rupee note in your childhood to its current purchasing power.

In the current context, the purchasing power of what you get after 20 or 30 years (premiums paid) will be very when compared to the extra premiums what you pay now to get it back at the end of the term.

Hi Manish,

My name is Ravi and I am staying in Bangalore.

I am planning to get a term policy worth of 50lkh coverage and also I would like get return on my investment if incase nothing bad happens to me. So I contacted SBI and they said they have a plan where I need to pay 28600 for 30 years and as I said if nothing happens to payee he will get 28600*30=858000.

After reading your comments I am in doubt whether I need to go for term policy with return on investment or just go with simple term policy and invest in mutual funds.

My age is 32

My investments:

LIC:32400 Per year

MF(ING):48000 Per year

MF(RIL):35000 Per Year

Br

Ravikiran

Better not to go for it ! ..

Dear Manish,

Thanks for the Mathematical explaination however scenario changes if we go for higher coverage value e.g 1.2 Cr instead of 1200000 as Term insurance is meant to pay all your debts plus provide enough income to your family for all those rest of the years one whould have been earning. In such case, the premium difference is coming out to be 10000 ( regular term plan (max life) 14700, premium return plan (aegon religair 24000 with coverage 1.2 Cr & return of premium) Do you still suggest to go for regular term plan in this case say for 20 Yr policy term?

Hi Sandeep Chandrashekhar Pawar

Even then term plan is a good choice . Let us know if you need our help in choosing and buying a right term plan . You can leave your details here – http://jagoinvestor.dev.diginnovators.site/services/life-insurance

How is the insurer Edelweiss Tokio ?? I am looking for a term insurance.

Hi Vikas

Every insurance company is fine as far as you are honest in filling up the form . HDFC Click2Protect is a great option too , and you can look at it . If you want a call back from them , you can participate in our Action month we are running this month and you would get our support in choosing the plan .

Check out – http://jagoinvestor.dev.diginnovators.site/2014/12/december-action-week-for-life-and-health-insurance.html

Its a new company . I cant comment on how good or bad it is, but you can take it if you can connect yourself with it. Why not go for other companies like LIC, HDFC , Aviva etc !

Dear Manish,

First I want to say Thank God, that I visit this site today.

Today I am [35 yrs old] goining to pay today my Aviva i Life insurance policy 5th premium Rs 5099/ [30yrs term plan – 50 lacks]. Now days I am seeing term plans with return premium so I am confused. Please help me that I have yo continue with these policy or I have to exit and take new one. I have more to ask you regarding my financial planning but first i want guidence from you for above mentioned issue.

I have gone through all your bloks and impressed very much with your advice.

I like to join this forum too so please help.

Thank you.

Best regards,

Dipak Katekar

You can go with it .. no issues ..

Thank you very much for you guidence

Hi Manish,

I have subsribed to term insurance from aviva ilife term is 35 years SA is 60lac age is 29 years, all this is along with health insurance for 30 years SA 10 lac from aviva, now could you please suggest me shall i continue with my LIC tarang or go with balanced and growth oriented MF or PPF, thank in advance

You can be with LIC tarang for investment reasons, from insurance point of view I think its anyways not a big amount and does not serve you !

Sorry to bother you again

I have term insurance of 60 lac from AVIVA plus health insurnance of 10 lacs all this for term of 30 Years, would like to know shall i invest in PPF or MF or in both if i want to generate maximum out of my investment

Thanks,

Yashwant

Yes, you can invest in PPF or MF , but how is it related to your insurance part , they are totally seperate part !

Great review…

thanks a lot first of all for posting such a easily understandable article.

i want to take your valuable advice for my future planning and will be highly thankful to you always.

(i am 24 year now and will take term plan for 54 year term.[because taking 30 year term will be probably make no sense. as in general average indian will not die till 70 year]

my current income is 4 Lakh per annum. and wish to take cover of 1 crore).

my budget is around 24,000 per year for term insurance + investment options.

i also wish to have corpus after 20 years around 10,00,000(in current value of rupee-please calculate inflation as i dont know how to calculate it :sorry for inconvinience).

what should i plan for the best possible return and that too considering life insurance in mind ???

i think i should buy term plan from AEGON for 1 crore (as it is the cheapest and longest cover provider )

so should i go for AEGON or change the company ? or split into two companies ?

but i have a doubt regarding their existence after 54 years ???

and second doubt is claim settlement ratio as i found that it is only 67% now a days for 2012-2013 ???

what do you suggest to me for above situation ???

pls. guide me and suggest the best looking into current trend …..

p.s :-can you meet me personally (or do you have any assistant) in surat,gujarat ???

THANKS A LOT N LOT N LOT IN ADVANCE…..WAITING FOR YOU BEST REPLY SOON…

Hi Mayank

You should read this article – http://jagoinvestor.dev.diginnovators.site/2013/04/why-you-should-not-take-term-insurance-till-75-yrs.html

thanx a lot first of all.

i have read the article you mentioned above. my question is that difference in premium is only 516 rupees per year for coverage till 75 year & 60 year. then why to take chance ? if i dont want to continue after 60 years of age then just stop paying premium and thats all. but in case i wish to go for new cover on that age it will be highly costly.

and another question is that why should WASTE money with insurance company by taking insurance till 60 years only ?as per general circumstances average age of indian is 75 currently. (instead take till 75 and pay around 150000 more to insurance company and take 1 crore is a better deal what i think) WHAT IS YOUR OPINION ?

AND sir , perhaps you missed my another question regarding 10,00,000 corpus after 20 years from today .. pls. reply on the same sir,

Thanks a lot once again.

Mayank , you can go ahead if you are ok with the extra payment !

Dear Manishji

As i have checked on policybazar.com while showing that i am a mariner, there are few company like Aviva, Maxlife they have the option in their “profession” column, Marine. So should i take from there?

Please advise me that what are the things need to be checked before taking the term policy.

Regards

Prabhash

Yes please choose it from dropdown and move ahead . They might put some loading factor or deny it , but you cant do much from your side, go ahead !

Dear Manishji

Good day

I am a mariner & want to take a policy of 50 lacs for 20/25 years. Please advise me which term policy should i take, as i dont have any idea.

Thanks a lot

Regards

Prabhash

Hi Prabhash

I can see you also opened a thread on our forum for this . Lets wait for answers there . From my side I can tell you that very few companies will be ready to give you term plan , You should look at some offline term plans . Contact each company in market and tell them you want it, see what they say ! .. There is no one company which is known to give it to mariners !

Hai manish, me and my brother have taken ULIP policies from lic namely lic money plus and market plus1 each with premium of Rs10000 per annum, 5 years ago.. Their performance is not good.. Do U suggest us to surrender them..

Excellent article Manish !!

Thanks

Hi Manish,

Nice contribution to leyman investment knowledge..

Keep posting such posts.. I’m loving it!! 🙂

Thanks & rgds,

Rakesh

thanks Rakesh

sir,

nice reading with an easy illustration.Thanks

when i taken the home loan,bank asked me to take insurance plan to cope up with the unexpected emergency related with the my life.But i intend to take a term insurance plan other than offered from the bank.My age is 37 and loan amount is 12 lacs for 20 years.Can u suggest a term plan for this purpose?

thanking u

biju t n

Hdfc click2protect

hi sir

i had 2 children ,and which company i choose for term plan for high risk coverage

and better claim settlement in future if iam nomore ,what is ur valuables suggestions.

and children plans for future my childrens ;i want to take

term plan with combinations of children plans.

i will pay rs:25000 for annum ,so pls help choose ever good plans combinatios.

my age :30. children1:2yrs children2:02months

Can you put your questions points wise ?

hi sir

term and child plan combinations tell me sir

my age :06/06/1983

my wife:31/10/1986

my son:05/02/2012

i will pay for annum: up to 25000

pls give u suggestions ,tem and combinations of plans

thanking u sir .its ugent

Get a 1 crore term plan

good evening sir,

in insurance industry , in which company is best,andchoose term policy

Kotak ,Aviva and HDFC are good options !

Dear Manishji,

I am 42 years of age and diabetic. I have quitted smoking 5 years back. I want to go for term insurance, PPF and SIP. Can you pls suggest what term plan and SIP i should invest.

HDFC click2protect and HDFC Prudence !

Brilliantly written article! Removed all my confusion about these so-called “Return of Premium” term policies. Thank you for this highly informative post 🙂

Welcome Sandeepan . Spread the knowledge !

Hello Manish interesting read ..

I would like to get some clarification regarding splitting of term policies .What are the benefits for splitting of policy ?

I will give you the biggest one .

When you split a term plan into two , you have a choice later to stop one incase you want , if you do not split, the only option is to close the whole term plan and take a new one with lower sum assured , it will be high premium one because that time your age will be high .

Manish

Hi Manish,

I am unfortuntly one of those who read your blog late. I guess I realised this pretty late that if its your money don’t trust anyone even if they are certified financial investors company, be vigilant.

I got trapped in TROP offered by aviva my policy has a term of 30 years with yearly premium of 16500/- and a cover of 50L.

I have already paid two permiums and i am thinking of not paying the third one, taking a new traditional term policy (with premium of 10000 and 1cr coverage) and investing the rest of the amount 6500/- in the PPF (8.8 %) for next 30 years. Do you think its a right thing to do or should i keep the existing one?

Yes, thats a right move . Go ahead !

Hi Manish,

Can you plz provide your review on EdleweissTokio online Term plan giving max of rider which are not available in other Online Term Plan??

Its fine to go with them .. NO issues

Hi Manish,

I have a LIC term insurance plan for which I am paying yearly premium of Rs. 10160.

Now, I am planning to shift to aviva term insurance with premium return plan.

For which I am supposed to pay Rs10577 yearly. so illustration u have given shows a major diff in premium but in this case their is a marginal difference. What whould you suggest ?

This is an old article, the new rates are very less

I know

But I wanted to know your opinion …

I did lil research on premium ..Aviva charging hardly four thousand for a basic term plan whereas for ROP Rs. 10000….what you said in your example still applies.

Now I am planning to shift my policy to some other good company. Can you please suggest me few of them.

You have other options like Kotak , HDFC life

Hi Manish,

I want to thank you for educating people like me on investment and planning.

I have taken Aviva Life Shield Advantage Plan (ROP) for Rs. 1 crore with an annual premium of Rs. 61500 (Rs. 40000 basic premium + Rs. 20000 as health extra, as I was diagnosed with high cholestrol levels) without any riders. The insurance agent told me that in case of normal policies (no ROP) the extra premium for health related issues will be 100% to 150% whereas for ROP policies it is 50%. If we consider Rs. 15000 as premium for non-ROP policy then the premium may increase upto Rs. 37500 (Rs. 15000 basic + Rs. 22500 health extra considering 150% increase). What is your take on this? Now I am thinking what I can do. Whether to stop this and take another policy or continue?

You need to discuss this in detail here – http://jagoinvestor.dev.diginnovators.site/forum/

Really nice, I was planning to take premium return term insurance. Now after reading your article I have decided for just term insurance.

Thanks for explaining by providing simple and easy understandable example.

Good work. Keep posting good articles.

Good to know it helped you Raj !

Hi Manish

Nice article.

I want to know , should i go for Aviva term insurance plan. I am 27 years and want to have term insurance plance for 50l.

What do you suggest ?

Aviva is good ,go for it !

Hi Manish,

First of all.. Nice work 🙂

hey i have a Met smart plus (sum assured 12 lacs)

its on multiplier 100% allocation

i have paid the premium for the same for 3 yrs (dec 2006 till dec 2009)

after which i opted for the premium discontinuance (with the policy being active).

reason:i wasnt really happy as the total invested was 144000 (48000pa*3yrs) and the fund value till today hasnt really been good. i guess the market aswell hasnt been doing good since then.

Metlife charges a substantial sum if i take the money out so i dont have a choice but continue. so the service charges whatever is getting deducted every month.

few days back i got a call from met life asking me if i want to reinvest a part of my premium that i had paid to reinstate the policy. And this part that they would take out of my premium will be treated a partial withdrawal.

my question to you:

1. do u think i should go for it? (the partial withdrawal- for the premiums that i havent paid)

2. you think i should again start paying the premiums..which would mean that i wld have to first cover the premiums that i havent paid for so long since 2009.

3. or should i just wait for nother 4 yrs for the return charges comes to zero?

if i have confused yu then lemme know 🙂

Any advice is appreciated.

Thankyou

Keith

I guess 5 yrs is now complete , you should now get 100% of your fund value , take it out now

metlife says it would charge 50% of a years premium if i withdraw now.. and every year it would fall by 10%. so by the end of 10th year it will be nil.

They want me to go for the partial withdrawal scheme..by which they would invest 80000 back to my insurance.

I am not sure if i should go for this or just stay put and wait for 10 yrs!!

i dont want to lose my money and in a way i am losing it bit by bit with the charges they levy every month.

How would the company benefit by reinvesting my own money?? m not able to understand that. and also would that be beneficial for me??

Thanks for the speedo reply..

regards

keith

I think you should check what does the document brochure says about withdrawing of your money, what ever is written there will apply !

Hi Manish

Thanks a lot …i will read up more abt MF and also check out the funds u have suggested. Really thanks a lot again for ur suggestion i will keep in touch with the blog for more smart ideas.

Hi Manish

Thanks a lot for ur reply but what do u mean by ”policies”. I thought traditional plans are a sign of Safety even is the returns r not very rosy …aren’t Mutual Funds more riskier than ULIPs..

Neetu

By policies I mean any products which combines insurance and investments , Yes Endowment products are Safe , 100% safe , but only in terms of return of your money + some basic returns like 4-5% .. Why do you need endowment plans in that case ,you can be better off in a Bank FD in that case .

Look at products from returns above inflation point , else you are loosing a lot .. I would suggest you get my book from flipkart and read its 3rd chapter on Equity and Debt , that will open up that concept very well for you , here is the link : http://www.flipkart.com/books/9380200415?affid=INManish2

Thanks a lot … i understand what u mean about traditional plan. But as u said ULips r no good then the only thing remains is mutual funds ….but what abt ppl like us u have zero knowledge abt M.F ..how will we know where, how & how much to go about it .

Neetu

Truely speaking , you need much less info about mutual funds than you can imagine to start investing in mutual funds. I really suggest you to take few understanding about mutual funds first and then ask your questions on our forum http://jagoinvestor.dev.diginnovators.site/forum to get more idea .

To start with , I would suggest pick 2 funds – HDFC Prudence and DSPBR top 100 . Do a SIP in both the funds for 1 yrs . Dont look at them on regular basis !

Hi after leaving on the last post i read ur answers & guides thoroughly and finally decided that i will not opt for any ULIP plan any more .. so i have decided to go for Birla sun life’s ”Birla Vision” for 5K montly for 25 yrs plan with life cover 12L…and also another 5K in Tata Aig’s ”Maha Life Gold” for 15 yrs with life cover 10L & lastly SBI’s ”smart sheild for 25 L policy for 30 yrs . I Hope i am doing the right thing this time . Ur Opinion will be highly apprieciated .Thanks a lot

These plans are worse then ULIP’s /.. never invest in “policies” , just take few mutual funds !

Hi Manish

i am 35 . i have read ur blog recently & i found ur suggestion & guides really helpful to ppl like us with Nil knowlegde …U really r doing a great job …thanks a lot anyways i have recently started off with the investment plans . So far i have taken LIC 2k (10L insurance) plan & Tata Aig invest assure (2K) montly for 20 yrs PT. i want to take more plans with 50 to 75 L cover & also good returns , My agent has suggested that i take Aviva freedom Life advantage where the Sum assured is 1000000 , PT is 15 yrs , PPT 5 yrs , premium 100000(p.a) on my kids name so that the mortality charges r less & along with this take Aviva Life sheild on my name with the cover of 50 L (ROP) with 22000 premium (p.a) .. do u think i should go for this or should i take the freedom plan from Aviva & life insurance plan from LIC ..kindly suggest if u feel i can do any better ..Thanks In Advance

Just get term plan for life insurance and as I suggested some time back , take mutual funds

What a clear , simple explanation . I just had a realization of how much fool I was when I took an endowment policy without any idea what I am doing 🙁 .

Thanks a lot for saving my day .

All you need to do now is define the next action !

Hi Sir,

I’m now 31 Years old. I want to invest monthly 5000/- for a period of 15 to 20 years Horizon. I’m deciding to opt for the following.

1. Aegon Religare I maximize ulip plan(rs 2000/- monthly)

2. Sbi Subhnivesh/Kotak Capital Multiplier Plan/ HDFC Life Sampoorn Samridhi Insurance Plan.(rs 25000 PA)

Kindly suggest if ulip of religare is worth & from 2nd whicle one is good(kotak, sbi or HDFC)

I want have some good & guaranteed returns after 15/20 years. Please guide me.

Many Thanks.

Radharanjan

If you want to have guaranteed returns , then you should put money in bank FD, all the other kind of investments will have some kind of risk . I would suggest you putting money in mutual funds through SIP over 10-15 yrs

Dear manish and others

I am sorry to deviate from this actual article. All suggestions by manish are good

for active personal finance manager. but i think from the mutual funds we can go

to an extra mile. I used to see the portfolio of successful mutual funds in moneycontrol.com and invest directly in the list of company stocks specified there.

At the same time i purchase the mutual funds also. The results are amazing. My portfolio grows very fastly then the original fund NAV and goes down fastly when

my fund is also going down a bit slowly. so instead of investing in a particular fund

we can follow the updates of the fund and proceed ourself to gain maximum

Prasanna

Good that this worked for you, but you might have just bought a couple of stocks in that fund and in that case you were lucky that what you bought went up . Next time if those went down , then what will do you , for how many years this has happened ?

Hi Manish,

Does Aviva has any return on premium term plan insurance?

I am not sure on that , why do you want return of premium term plan ?

Dear All,

I wish to suggest all SIP investor one fact about Reliance SIP Insure scheme.

Pls be carefull in selecting term of Rel MF Schemes with SIP Insure feature as there is 2% exit load on this scheme and later on you can not change the term also.

Agent or the company people may not tell you about this fact.So go through clear terms & conditions in fine prints.

Regards

Thanks Saurabh

Good to know those points from you . Keep contributing !

Hi Manish,

Your suggestions and guidance is very impressive. Its good that finally I landed on a site I have been looking from long time.

I have 1 yr old daughter and now I would like to start investing for her education and marriage. I have 10L savings and paying insurance of 1L pa. Policies include Jeevan Shree (24K), Money Plus(10K), New Bima Gold(6K) and few Ing Vysya policies. I get 12K per month on my 10L savings.

I have a home loan of 26L with EMI of 26K for 20 yrs. EMI hasnt started. After my expenses and home loan I will be left with 15K from my salary.

Now for my daughter’s future, I am confused whether to take any SIP or Quantum Gold ETF. Please suggest if any better choice.

ChPCR

First you should slow down and relax. The first thing people start getting worried is child education the moment they are born ! . All you need to do is take a good term plan with right cover and start investing in mutual funds and other simple products for long term wealth creation !

Can you please suggest good term insurance plan?

ChPCR

There is nothing like that . it all depends on your trust and belief . LIC , Kotak ,Aviva ,HDFC are the options

Hi Manish,

I found out abt religare and since I am 34 years old, for 1 crore sum insured its coming to about 15000 annualy.

How do I divide my 25 lacks in equity, SIP etc so that my risk is moderate

Thnx

Vishal

Vishal

If you want totally secure investment, then equity mutual funds are not for you .. I think you can take STP route here .. Put money in some debt fund or bank account and then transfer some X amount each month in some balanced and debt funds

Manish

Hi Manish,

I would like to invest 25 lacks and things that i want is the following:

1) Term Insurance for 1 crore

2) monthly benefit for my mother, I dont understand anything apart from tradational investments such as FD and buying property

Kindly guide me where to invest so as to get the maximum return on investment

Thnx

Vishal Dhish

Vishal

You can get a cover of 1 crore from companies like LIC , Aviva , HDFC or Kotak , ICICI , not sure if you want to make yearly payments or just one time payment ?

Also for generating regular income ,you can use FD and take the option of quarterly interest payment , with 20 lacs you might get around around 15k per month income or near that .. However there are other options also you can learn about them here : http://jagoinvestor.dev.diginnovators.site/2011/11/10-income-generation-methods-india.html

Manish

Hello Manish,

I have gone through all comments and forums but they are quite old, now I want to know about the current Aviva Life shield advantage term plan where I need your valuable feedback please. The plan details as per below :

My age= 29yrs

Premium = 20055

Term = 30years

Coverage = 50lac plus accidental 1cr plus permanent Total disbaility coverage

Plan=Aviva Life shield advantage plan (option B)

Minimum first 3 years premium payment required

Premium paying holiday of 2 years after 3 continuos yrs of payment

Incase to total discontinuation policy still persists but sum assured will be reduced as per time lapsed since discontinuity

Currently,

LIC 50lac term plan cost 16800 (not sure it has accidental + PTD)

As its a money back plan, The premium is so less that it beats PPF plus term plan of LIC for 30yr term and its the least Premium Money back plan in market at the moment.

Is it worth taking ? As compared to other private players how trustworthy is Aviva amoung market players and its claim/settlement please ?

Also m thinking of Aviva + LIC of 1 cr total, means a

ROP(50L) + NROP(50L) = 20055 + 16800 = 36855 per year

while LIC 1 cr premium costs around 33600

how does it sounds ?

Thanks in advance.

Rajendra

Rajendra

I dont thikn you should still buy it , can you compare it with same company term plan + PPF or same company term plan + Equiyt funds ?

Take the cheapest term plan + PPF , compare with that

Manish

which term insurance plan is better??? i want 25k insurance for my family

Please advice….

Santosh

25k of insurance ? Only ? Are you saying premium or sum assured ? Is 25k not too less-

Manish

Dear Manish

It is great to come across this article. I need some advice.

#1. I am 51 yrs and not insured much (Just some PLIs for 2 lakhs) . My monthly income is 60k and my total monthly expenses are 35k. My sons are settled and I want to save the remaining 25k every month wisely. Can you please advise the best way to go ahead?

#2. I have some 10 lakhs spare cash which i have invested in bank FDs, Is there any other better and safe way i can increase the return?

Thanks in advance

Mukundan

As you now in your 50’s .. you can put your Money in balanaced funds assuming you want moderate risk on your money

Manish

Hi

Thanks for the quick reply.

I will go for balanced funds. Any specific funds?

Meanwhile, any advice about term plans?

Mukundan

Mukundan

You can take HDFC Prudence, for term plans you have an option like Aviva and LIC

Manish

Thank you very much

i have taken LIC term insurance Jeevan amulay for 25 lacks & premimum paing Rs 16970 per year, policy duration is 30 years.

now i come to know from calculation as this plan term increses the primium also increses.

if i salender this policy and take new one from LIC with 5 years plan i will pay less premimum.

is it advisible,

Let me know

Vishwas

Vishwas

Yes , its true that for a lower tenure ,the premium would be low , but whats the use of it , at teh end of 5th year ., you will again buy the policy but that time the premiu would be for your age that time and premium would be high . So its not advisable , I hope you are looking for insurance as pure insurance and not investments

Manish

Dear manish,

I have planning to buy term insurance for 25 years for assured amount 2500000, with rider.but there is lot of company in insurance sector and also everyone having online insurance policy also . As per i have seen above comments kotak preferred is good or some one else . Can u give me advice for to buy policy online or offline is acceptable. kindly suggest your opinion for the same. You have good knowledge on term insurance

Kindly Advice, waiting for u reply.

Santosh

Santosh

There is no harm in taking online term plan , go for it .. you can go with ICICI , kotak or AVIVA

Manish

Hi Manish,

me too vry impressed of your site……very nice site & specially ur replies & ideas are awesome…..

Regards,

VANDANA

Vandana

Thanks for appreciation 🙂

Wich company’s SIP of best

Ravindra

Your question is vague … its like asking which cuisine is best and which restaurant has better food ? Its never hte best company which has best SIP , things go up and down , what is your requirement ?

Manish

Term life insurance policy with return of premiums

Hi Kawardeep & Manish,

Actually it was told by Reliance Mutual Staff only, not by any Agent

That’s why i trusted.

I will check again with my SIP amount and no. of units being alloted to me

in my statement. This will make things clear I suppose.

Saurabh

Its no different .. people move from company to company in few months/years .. there is only code of conduct , but no track of who is following that code of conducts .. So my previous reply still stands !

Manish

hi there, thanx for good suggetion on TROP.

I have one existing Reliance MF SIP. Very recently when i renewed it they told me about insurance of SIP installments and i opted for that when they told me that they are not charging any single penny as premium for that insurance from my SIP amount.

IS IT TRUE? PLS GUIDE

Saurabh

Who told you that ? If agent has said that , then its not true because they lie generally .. what is the whole plan overall ? Please explan

Manish

Hello Manish and Saurabh.

Yes even i get some emails on insurance of SIP from reliance too. There may be some hidden charges for the same. I discussed it with my financial adviser and he is strictly against these type of products.

Kawardeep

Yea .. right . better go for just plain insurance ..

Hi Manish, Your blogs are really awesome.

Well want your advice in some cases. My age is 29 yrs, Married and i have 8 months old daughter. So i have to plan right now for her study and her marriage. I am investing 8000/- per month in SIP from last 1 year. Details are given below.

HDFC GROWTH FUND(G) – 1000 P.M

ICICI PRU DYNAMIC PLAN – 1000 P.M

ICICI PRU INFRASTRUCTURE – 2000 P.M

IDFC SMALL & MIDCAP – 1500 P.M

RELIANCE EQUITY OPP. FUND – 1500 P.M

RELIANCE VISION FUND – 1000 P.M

1. Are these plans are good enough for my goal or i have to change any one ? 2. I think i have to invest in gold through SIP for marriage of my daughter. Which funds are good for this ?

3. Should i invest in SIP or other options ?

4. Now as per my thinking i should have term insurance plan for safety of my family and my daughter’s future.

Please Advice.

Kawardeep

I think you are going good .. focus on consistency rather than funds name .. Do a yearly review .. you are ok at the moment . Dont add more funds

Go for term plan .

Manish

Thanks for your advice Manish.

i know long term investment is right way to achieve our goals.

Kawardeep

Nice .. good to see you on right direction as well as your financial advisor is good one

Manish

Dear Manish –

I may sound like a fool to some. I have some basic questions on Term Insurance.

1) Is it better to take a long term or a short term plan.

2) In case you outlive your term period, what happens to the premium.

Many thanks.

Lara

1. Dont see it like that , Take term plan for the remaining time for your retirement .

2. Nothing .. policy expires ..

Manish

Dear Manish,

Your blog is very helpful for the person like us. I am a 30 year old male living in Delhi and earning around 25k per month. From lat year, I started investing and currently I am maintaining a PPF account with SBI (Annual investment about Rs 25000)and Rs 10,000 annual investment in NPS. Recently, I started SIP of three mutual funds viz., HDFC Top 200, DSP Blackrock Top 100 Equity Fund and ICICI Prudential Focussed Bluechip with the invetsment of Rs 1000/- per month in each fund. Just two days back, I taken the Aviva i Life Term Plan from their website. Can You please suggest that whether my portfolio is OK or I need some change in this.

Please suggest.

Thanking You.

Hi Ashutosh,

Could I get your number please, I need some info on Aviva I-life, I have already filled the form, just about to make payment.

Hi Vishal,

I made the payment through my credit card.

I can not post my mobile number at this website due to privacy concerns. However, if you need to talk to me, please give me your email ID and I shall send you my contact address at the same.

vishal_kol@yahoo.co.in is my id. It will be very helpful if I can talk to you as soon as possible. I have already filled up the form and waiting for a sugestion from someone who has taken this policy on one or two questions and their impact before I make the payment.

Vishal.

Hi manish,

Need your guidence

I am 28 years of age and investing in 7 SIP namely hdfc top 200, hdfc equity, hdfc mid cap, hdfc tax saver, hdfc prudence, fedelity equity and fidelity tax advantage for Rs 1000 each.

I am planning to take two Term plan Religare and ICIC for 50 lacs each for 25 years.

Is my sip and insurance combination right or not

Regards,

akhilesh

Akhilesh

yea. you are going right

Hi Manish

i am 33 year old married with 2 kids and i want to know about sbi smart life term insurance plan.

Is this plan is sutable for me for 15 year

can i choose single premium option

and tell me any best plan.

thanks

shyam

Shyam

Take any term plan . Are you not ok with online options ?

Manish

Hi Manish,

Thanks for all the replies in patience. I am a new add to your fanlist.

Am planning to take a term policy but confused on private-public fear. I am almost finalising a deal in LIC. Have some points to conclude and hope these are the common points for all the aspirant policy takers.

Appreciate your thoughts on the below:

(a) Can I go for Private Co., with the same confidence as I have on Public Co.,s?

(b) Term policy is issued on any basis (like salary of a person multiples, individual networth or just the paying capacity of an individual…)?

(c) Is it suggestible to go for riders (like permanent disability, etc)?

(d) If I take the term policy from 2 different Co.,s, will the beneficiary get the insured sum in full from both the compaines?

Once again highly appreciate experts inputs as this is a once in a life time decision.

Regards,

Chakri

Chakri

1. There is lot of confusion here , There are few ununderstood things because of which public is too fearful . Its true that if you are with a new company and its an early death , it would be not as easy as it would be with an old company and late death (more than 2 yrs). So truely speaking I would say split the cover with LIC and non-LIC . balance can be there .

2. Yes , if its a large cover , it would be your networth and mainly its dependent on how much cover you alreayd have ?

3. There is no suggestion , each riders provides you some benefit , its only you who can decide if you want it in your life or not

4. yes , the beneficiary will get it from all the companies in full

All I would say is take action , you have done the ground work , not where is the action , I want you to complete this and take the term plan and share your victory with us here . I am setting up the deadline for you 🙂 . Next 15 days !

Manish

Hi Manish,

Excellent Forum and hats off to you knowledge.

I need you advise.

I have the Endowment Assurance policy from LIC

Sum Assured:3,50,000

Policy & Premium payment term:30 yrs

Premium:10,667 per annum

Accrued Bonus:1,97,400

I have already paid 10 premiums (policy commenced in 2000)

Apart from this I have Principal Personal Tax saver (investment 80k,current value 60k, divident received 19k) & HDFC Tax save (investment 45k,current value 44k, divident received 7k) thru SIP which i could not continue for long as I have booked a Flat and am paying 10,oo,ooo as the EMI.

Currently I save 8000 a month after paying EMI, I need a term plan for family security, wealth accumulation for my 1 month old son’s education etc… health insurance is thru company so am not thinking of additional Health plan.

Aviva iLife is the cheapest term plan with 50,00,000 cover,35 yrs term, premium 4769 pa. Is it ok to go as I did not find anyone enquiring for this or suggesting this? After this I will be left with about 4000 pm. My complication is should I liqidate the LIC, agent says I will get about 2,00,000 if stoped and if completed the term I will get 8-8.5 Lakhs on maturity. I also have to start SIP for wealth accumulation.

You advise is highly appriciated.

Regards,

Vishal

Vishal

You have too many questions . Please ask generic questions which can be answered with ease .

Manish

Sure Manish,

If you can help me with this.

I have only one LIC policy which is the Endowment Assurance policy Sum Assured:3,50,000

Policy & Premium payment term:30 yrs

Premium:10,667 per annum

Accrued Bonus:1,97,400

I have already paid 10 premiums (policy commenced in 2000)

Now I think I need atleast 50,oo,ooo coverage for my dependants.So am going for a term plan. Now an confused which will give me more benefit , If I continue I will have to pay 10,776 for LIC and 5000 aprox for term plan. The agent says I will get 2,00,000 if I surrender the LIC.

Should I surrender, which means 5,000 aprox in term plan and balance 5000 in an SIP (Mutual Fund).

Which will be more beeficial if you can give an illustration as you have in some cases above.

Regards

Vishal

Sorry, forgot to add.

According to the agent , if I complete the policy I will will get 8-8.5Lakhs at maturity.

Hi Manish,

I just happened to stumble upon ur blogs, they are excellent!! Your passion for this field is clearly visible in you clear and simple writings…. Keep up the good work 🙂

Regarding Term Insurance plan I had a doubt…… I am a Marine Engineer by Profession so a physical disability of any kind would render me jobless. Will the term insurance cover this? or do i have to take a separate medical insurance for that?

Also as I am more than 180 days out of India, I do not pay tax, so am I eligible to invest under PPF and ELSS?

Thank you for your time.

AJ

You need to take a rider called “Disability Rider” along with term insurance , that will give Sum assured in 10 equal parts each year .

You have to see what is your residential status at the end ,if its not NRI , you can open PPF .

You can invest in ELSS anyways

Hi Manish,

Let me put down my financial condition and my personal life requirements.

My monthly take home is 28k

I have one personal loan 2 lakhs wich will close in next 5 years. i have invested this amount in my brothers business. out of that i am getting 2000 pM as intrest and same will be invested in Jeevan Saral insurance taken for 20 years.

Loan EMI is 5584

House rent is 6000

Other expence is 10000

Let me put down my requirement

Recently i am blessed with twin baby girls.

I need to take care their education and marriage expences.

Please suggest me the best investment plans.

Also i 50k in my hand now.

Regards

Naveen

Naveen

You need to invest in equity for long term for those goals . Relook at your current policy and find out how much are they givning you in llong term .

Manish

I am planning to invest 3000PM in mutial funds in two different AMC’s

Please suggest me the best mutial funds

And what is your openion on investment in Silver

Regards

Naveen

Naveen read this : http://jagoinvestor.dev.diginnovators.site/forum/thoughts-on-investing-in-silver/1186/

Hi Manish ,

Gr8 work here.You cleared all my doubts regarding term insurance (whether to go with the one which returns back the premium or the one which does not).I have a question here..We have finalized one property (90%) and have applied for a home loan from IDBI bank.

I have heard that if u dun have adequate cover (atleast worth the loan amt which we have taken) , the bank will ask us to take an insurance forcefully , whose premium is added to loan amt and we end up paying the interest on that too.Is it true ?

If yes , would you suggest us to go for a term policy from Aegon Religare , which does not return premiums ?

My income is 26K pm and my husband’s is 49K Pm.

I would also want investment tips from u , in order to get steady returns , so that we can pay off the loan amount periodically and finish it soon ?

We are currently invested in HDFC top 200,Reliance banking sector SIP and Birla Sunlife SIP.We also have 4 LIC policies (I guess with a premium totally amounting to 30K PA together)

Just to add , the property which we have finalized will be ready in August 2012,for possession.We have a loan amount of 27lakhs and we will be paying a Pre-EMI interest now (maybe starting from April 2011.)

Thanks in advance!

Priya

Yes Banks will ask you to have adequate cover , incase you dont have , it will be in home loan itself , you might consider that , actually you should !

The other suggestions which you have asked needs a detailed look and committed time to plan , You should look at paid services for this

Manish

Thanks for your reply Manish ..

You have said “incase you dont have , it will be in home loan itself , you might consider that , actually you should !” ..Do you mean I should go for the insurance products that are sold by bank ? I have heard they add this premium to the loan amount and we end up paying interest on that as well ? About Aegon Religare iTerm plan , I googled to find out if there are any exclusions.But I could find only one , the suicide one.

If you are aware of any hidden exclusions , can you plz tell me ? If there are none , then I thnk this is the perfect one!

Priya

When you take a home loan , there can be a added term plan with it self which will cover your life upto the cover amount, the cover will come down as per your loan , so at any point of time, it will cover you for the loan outstanding.

These loans are designed to give you many benefits like it will cover you from even partial and permanent disablement , loss of job etc ..

Hence over all its a good thing , but the premiums for this is higher than a stand alone plan which you buy from outside .

So you have to choose over cost and convinience .

Manish

Thanks Manish..I will enquire about it. Regarding Mutual fund investments , you have mentioned about consulting paid financial services.How do you rate HDFC bank’s investement services ? I personally am not willing to listen to agents’ advice on this , because many of them are misleading.But agents claim that banks like HDFC who offer investment services , will advice their own mutual funds to us..I want a genuine advice..Plz suggest.Even if you are able to help us out periodically , as and when u have time , thats ok ..because we still have time for the EMI cutting to start (about a yr and a half)..so isnt it enough time to plan a portfolio ?

Thanks in advance for all your advice..

Priya

Its recommened not to go with specific banks as they will advice for thier own products .. they have to …

Let me mail you on paid services part

Manish

Hi manish,

I am pragnesh and i am 28 yrs old married person. Here is my portfolio:

Total income – Rs. 35K/per month

Home Loan – Rs. 5800/- per month for 4 yrs.

Insurance:

1 New Bima Gold (873491503) 13884 (4 lac coverage) — shall i surrender? how is this policy. just 4 yrs old

2 Jivan Mitra Policy (873257493) 5010 (1 lac coverage)

Mutual Fund monthly SIPs:

HDFC Top 200 Fund 2000

IDFC Premier Equity Plan A – 2000

Sundaram Tax Saver Fund – 1500

DSP BR Equity Mutual Fund – 1000

PPF total investment till date: Rs. 20000/- (NO EPF deducted in my co.)

I want to take Term plan. suggest me what should be cover i should buy and from which company and do you think i need to add more SIPs to get more returns?

Regards,

Pragnesh

Pragnesh

Ask it on forum : http://jagoinvestor.dev.diginnovators.site/forum/

Thank you manish. I have just ask under Financial Planning. please reply.

Pragnesh

Keep an eye on it , it will be answered there

Manish

Hello Manish

I have 30 years Jeevan Mitra Triple cover policy with quarterly premium of Rs. 6,887 (Rs. 27,550 /year) from April 2006 onwards. It has accrues bonus of 1,00,000 as per the LIC data against the policy vailable online. If we consider appr. 14,000 yealy spent to cover insurance portion and remaining 13,000 is invested the return of 1,00,000 as bonus is almost 13% return on 13,000/ year investment for 5 years (I used your Excel tool to calculate) which in my opinion much better return.

I did this exercise after reading your various articles on term insurance when I was getting convinced, the above figures make me rethink.

Your reply is appreciated. Thank you. Am I making any mistake while doing the

Jayjonty

So you paid only 4 premiums of 27,550 each per year , which means you paid around 1.1 lacs till date ,with that I doubt that your bonus would be 1 lacs as of now , please login to your account in LIC and see how much bonus is accrued . Also get your agent on this and ask him details .

Manish

Not possible.

You might be choosen OPtion A.

Try to calculate with OPtion B.

For 50 Lac coverage of 30 yr age for 30 year term ….

ROP of advange : 20762

Premium of Plus: 13732. ( without riders )

Now remaining 7030 per year put in PPF.

at the end of 30 year amount will be 8,77,673.

ROP total is 6,22,860.

Hope this helps now.

well manish can better explain whether with riders it wll be good or not?

Regards

Jig, Manish,

Yes i used the option A

But i have downloaded the policy document from their site.

It says the following regarding options –

Option A: single premium or regular premium (equal to policy term)

Option B: regular premium (equal to policy term)

The only difference i came to know was if you go for option A the maximum sum assured is more and if you opt for option B the maximum sum assured is 50,00,000/-.

Thank you both for helping me.

Regards

Dr.Amarnath Awargaonkar

So finally did you get your answer and able to take decision or not ?

manish

Hello Amar,

I think still you are looking somewhere else.

Option A is Plan without Return of Premium

Option B is Plan with Return of Premium

please check with patience and sure your doubt will be clear.

I mean either of the plan is for ROP and other one is without ROP.

Regards

Jig, Manish

Life shield advantage is ROP

in that there are two options

option A where there is no cap on sum assured but you can insure yourself only upto 65 years of age

and Option B where the cap is 50 lacs for sum assured not only that when i downloaded the brochure for Life shield advantage it clearly mentions –

Option A: single premium or regular premium (equal to policy term)

Option B: regular premium (equal to policy term)

any way i have opted not to buy the ROP plan and continue with my old term insurance that is Life shield plus plan

where there are no return of premiums.

I have to admith although that my doubts have not cleared.

Regards.

jig, manish,

Life shield advantage is ROP

Life shield plus is pure term insurance

ROP plan has two options

Pure term plan does not have options

I believe in manish’s words “….but looks like the return of premium makes sense in this case unless I am not able to decode something hidden” If he is not able to decode then i thought it is best to stick to the term plan but i would like the members here to have a look, so that if it is really a good plan then it can be reccomended.

Regards,

Dr. Amarnath Awaragonkar

As i mentioned we can take an example of SA 50 lac for term 30 years and age 30 years. now below are the outcome of results for

Life shield plus

Life shield Advantage with ROP.

1) WIGHOUT ROP

Product Features

Name of the Product: Aviva LifeShield Plus

Unique Identification No.: 122N064V01

Sum Assured : Base Plan ADB Rider Aviva Dread Disease Rider

5,000,000 Not Opted Not Opted

Policy Term: 30 Years

Single Premium/Regular Premium Option : Regular Premium

Premium Paying Frequency: Annual

Base Premium: Rs. 13,732

ADB Rider Premium: Nil

Aviva Dread Disease Rider Premium: Nil

Regular Installment Premium : Rs.13,732

2)NOW ANOTHER ONE WITH ROPProduct Features

Name of the Product: Aviva LifeShield Advantage

UIN: 122N081V01

Plan Option : Option A – Regular Premium

Sum Assured : Base Plan Aviva Dread Disease Rider

5,000,000 Not Opted

Policy Term: 30 Years

Premium Paying Term: 30 Years

Premium Paying Frequency: Annual

Base Premium: Rs. 16,367

Aviva Dread Disease Rider Premium: Nil

Regular Installment Premium :16,367

well in both case i didnt include riders.

AND YES IN THIS CASE AVIVA GIVEN GREAT OFFER WHERE ROP BEAT NORMAL PLAN + PPF.

THANKS AMAR TO BROUGHT THIS HERE.

REGARDS

JIG

Jig,

Thank you for the appreciation.

This forum has helped me a lot and if i can give back something it would be worthwhile.

Regards.

Dr. Amarnath Awargaonkar

Hello Dr Amarnath,

Recently Aviva launched Life Shield Platinum. Can you share your view on that? I tried to understand its monthly income plan but still not clear about it.

I request Manish to review it and please share merits if good for readers.

keep sharing

jig

Jignesh

its a pure term plan , what review are you expecting ?

Here is a review you can read :

Manish

I have taken Lifeshield plus term plan (term 30 years) from aviva. Sum assured 60lacs and an additional 50lacs for accidental death, as i am overweight they have charged 11k extra. The total premium is 38600/-. I have this policy from one year.

My agent is telling me to get it converted to Lifeshield advantage, reason it is premium back term plan. We calculated the premium for 65L and it came around 30,500 although you do not have the facility of ADB rider. But the biggest advantage of this policy is, it is premium back term plan. Even if we add 11K as extra charge for being overweight it would be 42K but i will get back my 30,500 at the end of policy.

What do you suggest??

one more thing i lost my password i am a existing member of jagoninvestor can you retrieve it.

Dr. Amarnath Awargaonkar

Amarnath

You should read this article for clarification on return on premium plan : http://jagoinvestor.dev.diginnovators.site/2009/04/return-of-premium-term-insurance-is-it.html

Rearding your password thing , i hope you are talking about forum, can you please create it once again, I think because of inactivity , it got removed

Manish

Dear Manish,

My poinf of contention is that if we go to avivaindia site and calculate premium through their site the premium for pure term and ROP term plan comes near about the same give or take 5,000 Rs. how is it possible?

If it is!! then it would make logic to buy ROP term plan.

Regarding the password issue I tried to register with my old email id it is not accepting, it says email id already taken up or something like that.

Kindly advice about the term plan vs ROP

I have 25 more days to pay my yearly premium for the pure term plan which i have taken one year back.

Thank you and as always it is my honour to have a friend like you.

Dr. Amarnath Awargaonkar

Amar

You should do a similar analysis what has been done in the article , see how much is the difference in premium , What if you invest the difference in some other instrument like PPF or Equity funds , can you make more than what you will be paying in total tenure ?

Show me the maths .

Manish

Manish,

Here is the maths

Life shield Plus policy

Term: 29 years

Premium: 27,818/-

Maturity benefit: Nil

Sum assured: 65,00,000/-

Life shield advantage policy

Term: 29 years

Premium: 30,602/-

Maturity benefit: Return of premiums paid excluding rider premium, taxes and extra premium paid if any.

Sum assured: 65,00,000/-

All this calculations done on avivaindia website considering my age as 36 years.

Please suggest as i am really confused!!!

How can a company launch such a product where the beneficiary is only the customer?

Regards.

Dr. Amarnath Awargaonkar

Amar

Hmm.. I did the maths , but looks like the return of premium makes sense in this case unless I am not able to decode something hidden , It would not pay the taxes involved , so in the premiums of 30,602 you also have taxes at 10.3% , which means your without-tax premium is only 27541 . So for 29 yrs you will pay total of 8 lacs . Now you can save 30602 – 27818 if you go for first options , Only if you can generate 13-14% return in next 29 yrs CAGR , then you can get more than 8 lacs by investing the difference in some mutual funds , which is possible , but if thats the case ,going with the ROP option might make sense !

Manish

Artical is excellent. However one has to look while choose the Insurance company. Till now, LIC is the best for claim ratio and others (private players) are not tested. And there are lot of hasslement during claim. If Family is getting the claim, what is the point of investing?

Manish can you write something about this issue?

Dip

Yes i wll comeup with that soon

Manish

What is Age limit of opening PPF account? I am 45 yrs old. If I open a PPF acount for 15 yrs, it will mature at my age of 60. As per the PPF rule, is it possible? OR is this adviceable to you Manish?

Dip

No limit on age, you can open it anytime

Manish

An eye opening article.. Awesome 🙂

Satish

Thanks for your appreciation 🙂

Manish

Hi Manish,

First of all great article and superb advice.

However, I would like to point out one scenario where ROP might look relevant. My acquaintance is 38 yrs diabetic (on insulin). As a result, his term application has been rejected by one company and the initial response from other companies is not very encouraging. This is when someone from LIC told me about the ROP policy. According to him, in ROP, medical is not required and the policy application will not be rejected even after disclosing all the facts.

So, in this situation, I find ROP relevant, not because it is better that Term, but it is the only option which gives a high cover and the net cost (after adjusting the capital returned) is managable. Do let me know your opinion. In case you wish to suggest any other insurance plan (with a high cover like Term) which is better that ROP in this situation, please do let me know. Some one told me whole life is better, but I am yet to analyze that.

Rgds,

Varun

Varun

Great point. In that case yes ROP term insurance would make sense . When one can not get pure term for medical reasons but he can get ROP , then he can go for it . Whole life plan would not make sense , i am sure on that , You can check Jeevan tarang analysis on this blog . It a whole life plan only .

Manish

Hello Manish,

I have 30K per month to save,protect and building wealth. Asset Allocation is about 50% equity and remainig 50%. I dont have any insurance right now. I will turn 30 in Dec 2010. My calculated Insurance amount is 1 Cr. I am confused with ULIP/ Term Plan/ Premium Return Term plan.

Can you suggest me best way of planning the insurance and investment?

let me know if you require any more information aside.

Thanks & Regards

Jignesh

Jignesh

You should invest in Mutual funds through SIP and take a pure term plan .

Manish

Thanks a lot. Exactly i was thinking for the same. You really made life simple for so many ppls.

Regards

keep it up

Jignesh

Jig

My pleasure 🙂

Manish

Hi Manish,

i want to go for short term investment plan (max 10-15 years) with maximised returns( if insurance is there then added advantage)

there are 6 policies from which i have been told are good or any other thing you suggest would be best

1) Aegon religare premium gain plus

2) tata lakshya plus

3) Bharti Axa Bright star

4) Aviva Safeguard

5) Kotak Super Adv

6) Birla sunlife dream

any suggestions which would be best ? or any other policy which is best

Also please suggest which is the best child plan currently (was blessed with a baby last month )

regards many thanks

Santosh

Santosh

You should not buy any of these . There are ULIP’s and are not recommended unless you are profecient in Markets . Invest in Mutual funds

Manish

Manish ,

I realised it that how simple it is to calculate the returns and even we should do these at the time of purchasing any investment rather than just checking the premiums and the end amount. Thanks for the information.

Also let me know if there are other calculators for calculating returns on sip, ppf, ulips, etc

Hitesh

Hitesh

Great to hear that , you seem to not give a look at the top nav and side bar . There are many calculators which you can use .

http://jagoinvestor.dev.diginnovators.site/calculators/html/Calculators-List.html

Manish

Manish,

As read on ur blog, lic policies normally offer returns of about 6%.

I have a personal example now

My mom had a Jeevan Sanchay policy. Premium was @6059 for 12 years.Sum Assured was 50000.

She got 10000 at 4th and 8th year respectively. Now at maturity she is getting 72000. So in all she is getting 92000 aginst payment of 72708. What are the returns ?

Hitesh

Hitesh

Its exactly 4.8% . Its a wrong way of seeing that she paid 72708 and got 92000 , it matters that when did she get the money and what was the cash inflow and outflow every year . If you do the IRR analysis (the way we calculate return for situation like this) . You will see that following cash inflow .

-6,059.00

-6,059.00

-6,059.00

3,941.00 (becasue she got 10k and paid some premium)

-6,059.00

-6,059.00

-6,059.00

3,941.00

-6,059.00

-6,059.00

-6,059.00

-6,059.00

72,000.00

4.80% = IRR

See IRR post in archives

Manish

Hi Manish,

I have these policies from LIC.

1. Jeevan Anand

2.Bima Kiran

3. New Bima Kiran

4.Endowment Assurance

5. Money back – 2 nos

6.jeevan Saral

7.Jeevan Mitral (half year old)

Premiums for above is about 45000 and sum insured is about 25 lacs

Q. Which of above should i retain and which should be surrendered ?

also can i surrender the jeevan mitra which is just 6 months old ?

Additonally i have a ulip from max new york (5 years old and current value is same as total invested till date so no profit even after 5 years)

Premium is about 15000 per year.

Q. What action to be taken? Retain or wait for more time

Plus I have two SIPs

1. BSL tax relief 96 (D)

2. HDFC top 200.

Both r almost 7 months old.

Q. Are they good enough ?

My age is 29 yrs, married with one son of 8 months and dependent parents (senior citizens)

Can i think of investing in senior citizen savings scheme @ 9%?

Regards

Hitesh

Hitesh

Your overall Portfolio is so messed up , You are not insured properly and your investments are for the sake of investing and doesnt seem to be linked with your goal .

What is your total insurance cover ? You can surrender LIC policies only after 3 yr and even after than you wont get more than 30-40% of money .

you can get out of the ULIP now , it was a bad marriage and now is the time to get out of it .

You should hire a financial planner or get it done yourself by learning things from this blog .

Manish

Yes , after reading some articles on ur blog, even i realised that my portfolio is not planned. And I think so its not late to replan. Actually most of the policies were taken by my mom (agents misguided her). 6 policies r almost more than 7-8 yrs old. If i surrender them will i get more than what i have paid or less ? Then i will go for term plan purely for insurance.

also can i invest in senior citizen savings scheme, as the returns r @ 9% ?

Hitesh

I am not sure how much will you get if you surrender it now , In general you should get around the same what you have paid till now including bonus, but even if you make it paid up , you are not going to benefit much , as you will get more , but at very later point ,so overall its the same thing .

You cant invest in Senior Citizen Saving scheme , unless you are a senior citizen 🙂

Manish

Hello Manish,

Can you confirm one thing,

One of my friend who wanted to take the term insurance for 40 lakhs, got the reply from a LIC agent that he can only get the insurance of about 22% of his total income. He just joined a company and has starting package of 1.5 lach annually. So according to LIC agent he can only get the term cover of near about 30 lakhs. Is that correct ?

Pradeep

Yes , it can be the case , company relate the cover amount with the income , so as per LIC they can restrict it to some percentage

Manish

Hi Manish,

But is this applicable to all other companies or just the LIC. and why is that ? After all it is the choice of person whether he wants to invest the whole money in insurance cover or not

Pradeep

Nope , a person cant have choice like that , as per principles of Insurance , one should not take advantage of Insurance and get himself insured for more than what his worth is . So if a person earns 1.5 lacs annually and chooses to invest 1 lac in term insurance , he can take a cover of 5 crores , which is not possible as a person earning 1.5 lacs will not have a potential cover of more than 50-60 lacs , or max 1 crore , so its generally restricted at some level .

This will be true for other insurance companies also , so you cant take term insurance for any amount , there is a limit, and companies will tell you that , thats the reason why you should disclose your cover to other companies so that you are not “over insured”

Manish

Thanks Manish,

I just came to know that he has one more money back policy on his name from LIC, so it might be the case.

Thanks for the information

Hi Manish,

From past 1 week I am browsing for sites which gives me some idea on mutual funds, investing and insurance. Your site is simply superb.

Kudos to you.

chakri

Thanks 🙂 . Do keep posting your comments 🙂

Manish

Manish

The maximum term in a term insurance plan across all the major insurance providers is 20-25 years.

I found ‘Bharti Axa Elite Secure’ to be different from the rest which provides life cover till the age of 75. Wouldnt it be advisable to take a life cover with maximum term. Of course, the premium is definitely higher when compared to Religare i term.

I would like to know if only cost should be taken into consideration or the age of individual and term for which they need to be covered also to be considered before taking a term insurance plan.

Padmaja

I mailed you 🙂

Anyways .. you can take the insurance till 75 if you plan to work till then and if someone is going to be financially dependend on you .. Insurance is protection against the loss of income , so if you are planning to retire around 55-60 , you should look at retirment date – current date kind of tenure .

Manish

hi manish ..

thk 4 reply..

please provide your valuable feedback on the following MF portfolio:-

uti master share ( D)

reliance regular saving E. share (G)

reliance natural resources (G)

require your suggestions.

Is there any risk associated here?

plz suggest me more funds ..

(i want 2 invent 2 to 3 thousand per month )

i also want to do insurance policy or ulip ., which is more suitable for me . my age is 22 ..

Dear Manish

Nice to read all your views. I am 35years old. Do you have any info on Met Suraksha Plus Term life insurance? Their website calculator is quoting me the cheapest per annum for 25 Lakhs and for 30 (Rs 9183) or 35 years (Rs 10562). Is it worth to go for the longest term 35 years or for a lesser term like 25 or 30 years? Only LIC and Metlife offer term life for 35 years. Your inputs on this will be highly appreciated.

thanks

Vinoth

All the term insurance plans are same except the premium cost and claim ratio . LIC is considered the best in claim ratio but its costly . you can take this one but make sure you split your cover in two 🙂

Manish

Dear Manish,

Thanks for your comments.

For insurace I have just taken one example of family health, company have lot’s of reasion to reject your claims. How policy holder get all the list of reasions before taking policy because there is no use of taking term plan if your claim is rejected by the company.

For term plan I should go with LIC+iTerm or iTerm only.

I am planning to invest 5K every month from my salary in above MF. As you said SIP is better than one time investment. I have 30K please suggest how to invest this money for long term.

Thanks & Regards,

Vivek

Vivek

Take the SIP in 2-3 good funds , invest whatever is comfortable for you every month , the key is consistency .

Manish

Hi Manish,

I want to take term plan but have some queries.

1. Go for goverment(LIC) or private fund(iterm).

2. What I think both the companies don’t like to give money to your family, they have lots of reasions to reject your claim. If my family don’t get any amount from companies so what is the perpose of term plan. For example death happen due to breaking traffic rule or some family disease that you have not mentioned in you policy becasue you never notice while taking policy .

3. Tell what steps we need to take so that I we can insure that company will not reject my policy claim. While selling policy companies don’t highlights points that they show during claim process.

Please suggest how to acheve my future goals

My age is 28,software engineer, married, one six month old boy, monthly salary 45000,staying in rented house cost 10000 per month.

Future Plans:-

Want to take Term Plan

Want to Buy House

Want to take Child Education plan

For Retirement taken SBI Pension Plan–annual premium 50000

For Health Insurance — Company provided 1.5 Lac Family Cover

My Mutual Fund Investment plans are to start SIP

1. Reliance Regular Saving Equity(G) — 1000 SIP(Monthly)

2. Sundaram select midcap(G) — 1000 SIP(Monthly)

3. HDFC Top 200 — 1000 SIP(Monthly)

ELSS

Can Robeco Equity TaxSaver — 1000 SIP(Monthly)

Please suggest……….

Thanks & Regards,

Vivek

Vivek