The shortest guide for a 22 yr old to start investing his money ?

POSTED BY ON September 22, 2014 COMMENTS (47)

I was on Quora some days back when I came across an answer by Yuvraj Wadhwani on a thread called “How should a 22-year-old in India invest his/her money?” . It was such a beautiful answer and loaded with awesome advice to someone young to start their financial journey in life.

I instantly contacted Yuvraj, if he would like to guest post his answer on Jagoinvestor and He replied back saying he would be glad to do so. So I am putting up his answer to that question here on this blog for everyone . Read it from start till end. Its a bit different in style, but really worth .

Note : I have realigned some lines and combined them together to make proper paragraphs.

OK let’s begin with wise words I learned a while back.

The principle of “Divide Investing in 3 plans”

It took me a while to get this, but it is really empowering to understand this principle. It is wise to divide investing in 3 plans.

- Plan to be secure

- Plan to be comfortable

- Plan to be rich

Let’s take each of these in detail.

1. Plan to be secure

Buy a big term insurance policy and don’t look at market linked insurance plans (ULIPs). Set aside some money and trust that your financial planner will do a good job with it. Also, set aside some money (~3 month’s salary) as an emergency fund. Once you set this up, this should be an automatic plan that doesn’t require your time or effort.

I think everyone should have a plan to be secure. Now, before going to the second or third plans, ask yourself this question..

“Do I want to be comfortable or do I want to be rich??”

This is a very important question as it will probably determine what you do while following your plan. It’s similar to setting up your goal before buying a gym membership. You may choose to have a light jog on the treadmill, or work out heavily with weights. You choose what you do.

Now read on, I hope after reading you will make a more informed decision about which plan is right for you.

2. Plan to be comfortable

The plan to be comfortable should be pretty straightforward for everyone. If you are a salaried personnel, then you save a portion of your income. You use 80cc to minimize your taxes, invest in diversified mutual funds, SIPs, or recently infrastructure bonds, or specific stocks if you have a good education.

You also have a financial planner who can give you advice for specific funds, or who can tell you to rupee cost average your investment. You also make some money of “hot tips”. If you follow this plan, you should live and retire comfortably. There is nothing bad/wrong about choosing this plan, just as there is nothing wrong with going to the gym for a mild jog. It’s an individual choice. Most individuals would find themselves in the comfortable zone. I encourage all of those people to read further as well.

3. Plan to be rich

Extracted from a book

Q: “What’s your advice for the average investor??”

A: “Don’t be average”

Why? Because the average investor is a slave to the market.

Average investors make money when the market goes up and lose it when the market goes down. Average stock traders don’t make money. (They don’t lose, but don’t make it either). When the market crashes, the average investor loses the maximum.

Successful investing is not about the investment, it’s about the investor.

This is perhaps the least understood concept of investing. This is the reason why people ask questions like “Where should I invest my money?” and the most accurate answer to the question is the question..

“I don’t know, are you a good investor?”

Let me give you an example – “What happened during 2008-2010 in stocks worldwide? Everyone knows they crashed right? Everyone who was invested in stocks lost money right??”

WRONG!

John Paulson’s , a hedge fund manager , made more than 15 Billion $ for his company in 2007. (That’s a billion with a B). That money is almost equal to 80,000 crores.

Many claim that he made around 4-5 Billion Dollars of personal money during (2007-2010). That’s more than 20,000 crore rupees. While this was claimed the greatest trade ever, the point I am making is that it is entirely possible to make money when the market is going up and down.

So what are the differences between average and rich (above average) investors?

Simply stating, successful investors have 3 E’s that average investors don’t have.

- Education

- Experience

- Excessive Cash

1. Education

A successful education starts with a good mindset. A successful investor has much more education than the average investor. A successful investor is committed to getting better and better with their education. How do you define commitment?

Do you know that friend of yours who plays the guitar? Do you know who else plays the guitar?

Got it ?

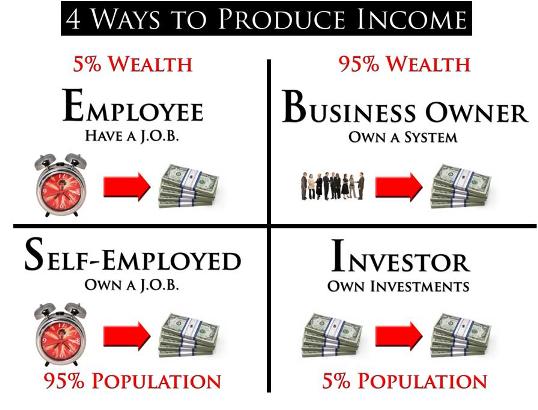

One of the differences between them is their commitment to playing. So how is the mindset of a successful investor different from an average investor? Let me draw a diagram to better explain. In the world of business, there are 4 kinds of people

- Employees

- Self Employed

- Business Owners

- Investors

Simply put, average investors think from the left side on the diagram and rich investors think from the right side of the diagram. Does that make a lot of difference, you may ask?

The answer is YES.

Let me put forward a few myth busters to put it in perspective.

(Avg Investor): My house is my biggest investment.

(Rich Investor): A house is a liability(Avg Investor): Diversification reduces risk

(Rich Investor): Diversification is de-worsify-cation (Warren Buffett quotes)(Avg Investor): Stock market is risky

(Rich Investor): Risk comes from not knowing what you are doing(Avg Investor): Avoid risk

(Rich Investor): Take more control and manage risk(Avg Investor): Real estate never comes down (extremely popular in India)

(Rich Investor): All markets go up and down(Avg Investor): Saving money is good

(Rich Investor): Saving money pays maximum ~8% before tax, inflation is ~10%, so saving money is a guaranteed loss.I could go on, but hopefully you get the point.

I am not saying what the average investor is saying above is bad advice, but it is average advice. As I mentioned, average investors make money when the market goes up and lose it when the market goes down. And if you have been reading till here, then you might be interested in making money whether the market goes up, down or sideways.

Also, if you find yourself arguing against the Rich Investor statements, that means you too are thinking from the left side of the quadrant.

So, how do I educate myself for being a rich investor?

- Books

- Tapes

- Workshops

- Mentors

Remember, successful people have coaches, amateurs don’t. Sachin Tendulkar may be the best batsman in the world, but he still has a coach. In case you are wondering, then investing is a subject that you may never be perfect in. Just like there is no perfect batsmen in cricket (everybody gets out), there is no perfect investor. But the more education you have, the better your chances are.

2. Experience

This should be a no-brainer. How do you get experience? By applying what you learn. Start small as mistakes will happen. If you stay on track it will become easier and easier. It might feel like trying to eat with your opposite hand. In the beginning, you will spill your food, you will be frustrated and probably won’t be satisfied, but in time you will learn it eventually.

3. Excessive Cash

This is the tricky part, but if you have educated yourself well, and have gained good experience, then excessive cash (or some cash) should already be rolling.

A note on the ultra rich

The rich investors invest in assets (stocks, bonds), but what do the ultra rich invest in?

The ultra rich don’t buy assets, they create assets. This is the secret how the richest people in the world created their wealth. They created an asset which millions and millions of people want to buy. Bill Gates created Microsoft, Larry Ellison created Oracle, Warren Buffet created Berkshire Hathaway.

Final Words

Q: “How should a 22 year old Indian graduate invest money?”

A: “I don’t know, are you a good investor?”

All right, you have my attention, now how do I get started?

Cool, this is what I would recommend.

Knowledge begins with words.

What does that mean? Let’s take an example. Many times when you travel, you meet people or are around strangers and you hear them talk. Most of the time you can guess their professions. Have you wondered how?

It’s by the words they choose and say.

I evaluated the students and the grades are good.

(Teacher)My boss is not a good person.

(employee)I shorted that stock as the P/E ratio was high.

(stock market trader)That patient had to be given a muscle relaxant.

(Doctor or medical professional)

So the lesson here is that if you want to excel in any field, you must learn (hopefully master) their words. And you know what, words are free! (yeeiiiii)

So tell me if you understand any of these words.

- P/E ratio

- Volatility

- Bull Market

- Bear Market

- CAGR

- Y-o-Y growth

If not, then this is your first step, to learn and understand these words.

How?

- Read your business newspaper.

- Listen to the market news.

- Use google.

Let me tell you a secret

Most of these complex sounding words are actually simple concepts. Really???

Let me tell you the job I had previously. I was Production support analyst for a retail POS application for a telecommunication company which sold products in multiple verticals. Only the job title is complex. So why do all these finance companies and news channels use these fancy titles and words? Because they want to sound smart, and want to sell you stuff.

So when you start learning words, you’ll understand the bullshit most TV channels and financial advisers preach as “investment advice” is really sugarcoated salesmanship.

So when the next time you read an investment advice column and say, “That’s nonsense”, Congratulations, you are making progress. If you are reading this, that means you don’t want to be average. So I encourage you to take the next step in your education and start learning words. I’ll try to help as much as I can.

Thanks Yuvraj Wadhwani for giving permission to publish his quora answer on this blog and share his knowledge

Business is always a good exercise to enhance vision and capabilities. JAGOINVESTOR, thank you for sharing this information.

Welcome !

That’s very nice advice. Thumbs up.

Thanks for your comment John

Your post is like “I am reading Rich Dad Poor Dad and other books of Robert Kiyosaki”.

Though your efforts are good to educate people.

Keep up the good work!

Thanks for that compliment 🙂

I was just searching on internet about stock options and came across your site. The whole site is very useful and this article specially covers many important things to which I can relate to as I am also 22 years old and serious about saving and making money.

From now on I will be follow both of you guys

Manish Chauhan and Yuvraj Wadhwani

Thanks Abhishek

You are at right place .. keep reading and keep coming back !

Good Pointers. Apt for all ages of Investers. Few points make sense how ever few does not. I will conquer on the House one. Home is the biggest necessity for all types of Investers and its regarded as a Physical asset / dream of every Indian. How ever it does not make sense to invest in big budget houses yielding low ROI. If You calculate the actual Rental return then its below the FD / ANY sort of Investment. I will say arround 4-5 %. In order to have a balanced and diversified portfolio one should have a egg nest of all sort of investment products with maximum allocation given to Equity (70-80%) if you are a Young Invester . I personally doing this and benefited from this.

Job well done Yuvraj and Manish. Waiting for your next one..

Thanks for sharing that point . I agree that focus should be on ROI !

Wow!!

Great answers/info..especially for 22 years old.

I’m humbled..:-)

thanks.

Vikas

Completely disagree on the statement “House is not asset but liability”. Dont rich people own Houses. if it generates only 5% why do rich own them. Note in city like bangalore buying a property while its available matters. Eventually the property is bound to appreciate later. its difficult to predict just like the stock market.

Thanks for sharing your view point on this matter

Dear Srinivas ,

Asset is defined (in simple words ) as any investment which puts money into your pocket.

Liability is defined as any investment which drains money from ur pocket

Now house ,ll need money money for maintenance, hence branded as liability. If the same house has rental portion then it’s an asset .. though capital appreciation is not only criteria to brand it as asset .

Note: empty plot need no maintenance so an asset .

Great work Manish, thanks a lot!! 🙂 By the way, I have written couple of articles on personal finance .. one is the story which happened with my father and other just read about it and made an article on it. Is it possible for you to read it and if found good publish it. I assure you its my own work. Like you, I just want people to be financially educated.

Mr.Anish,

Pl. share it. I am man to practice when any body shares his practical experience.

Yes, please send it to me !

The contents of the post is from Robert kiyosaki book rich dad and poor dad as mentioned in one of the previous comments..

Cashflow quadrant of robert says 5% of wealth is owned by 95% of population and 95% of wealth is owned by 5% of population this is not his original thought actually economist named paretto has invented this..

Robert says create assets buy assets which produce cash, but how can a employee and self employed buy a assets when he buys the biggest liability of his life namely the house by taking home loan?..Emplyee and self employed category ppl dont have excess cash to invest or start a business hence they are in this category…

Point is Employee and Self employed rarely gets the opportunity to move to Investor or business man category..

Thanks for that info

The articulation is excellent. Such read ignites me to learn more and more, share And intern feel confident while taking decisions.

Thank you for sharing…!!

Glad you liked the answer Prashant.

Awesome..! I have also read this answer. It’s good that you shared the same with your readers. Thanks.

Great Mihir !

Manishbhai,

Thanks.

Great service.Pl. keep to deliver such articles.

I have to say like this:

Note:Pl. edit below given idea to be more effective, if you find worth in it.I will be obliged to have input from others.

“Out of Box thinking”

Investment as a Business – how?

People says, money can be with the entity who does the business. You can get services of others, where in professional life, it is as per Gujarati saying, “Paind Kamye Paind Khay”. He can be only worker to become milliner. Professional like doctors and lawyer have to work himself and cannot employ a large force to multiply his earning. This limits the earning power.

If you start a business, it will be in particular sector viz: IT, Pharma, Capital Goods, Reality, FMCG, Food products, Hospitality, small grocery shop and so on. Out of these, few may be cyclic, few may be influence to Govt. policy, world level crisis effected, climate or drought effected etc. Business may have gestation period at least minimum of one year or more and in bad circumstances one cannot be get rid of immediately and start a fresh.

People generally try to establish monopoly business to get maximum profit within shortest period of time. Here in stock market business, it is favorable/good to have competition. If competition is there to snatch the shares of good-growing company, share price will shoot up. This is a profitable condition in any other business this situation will not be.

Why one should establish business?. It is like saying; Foolish man (King) built house, but lizard lives in it. It is just like cloud computing, you have cloud earning company. No such other business exists. It does not need to have factory premises or even not office so to say.

Investment business in stock market can cover any group of sectors. Buying a company shares means, it is like buying a company. As you buy company stock, you are earning thru work of employee of that company. And as you can buy number of company shares, you are earning from that strength of multiple of that employee. Thus you have tremendous earning power, if you have selected right (Sun rise company) company. These sectors can be selected where Sun is shining and can be disposed when Sun is about to set. Investment can be changed to lucrative sector whenever opportunity arise with click of mouse. Home grown business, no other business can be run. There is Safety and security of the person as he she has not to go out of his residence and there no fatal accident or risk of life. No local or foreign trip for business development or promotion.

People advise to diversify investment. Such as few percent in FD, reality, health, insurance etc. Here stock investment can be made in these type of industry/sectors which will serve those purposes. For example, as a FD purpose one can invest such steady FMCG and or “A” group shares of reputed promoters/company of stable sectors.

Person in this business will have no boss to report progress or development nor to take work from subordinates. As a business man, he has not to salute Faltu Govt. officers of below dignity to get favour to have license of various types. He has not to please Faltu politicians as well as Faltu union leaders. No inspector Raj.

Nobody will notice how much wealth you owns. No fear of abduction of anybody or of family members.

This business needs the art and science of investing, the capacity to take judgment calls based on imperfect knowledge …the progress of business is a sum of multiple events x the probability of these coming true..In this business who ever judges the risks best …makes the money.

In this world who are the richest persons. Bill gates and Warren Buffet and so on…How they have been qualifies?. By their investment in the company and its capitalization of their equity holding in company or companies. ……

Thanks for your views and points 🙂

Thanks for sharing your views on this . Good point I must say !

Thanks,

very good lesson for the youngers,but plse be sound to guide the youngers in proper way

Thanks Jamshed !

Good piece(s) of advise.

There are few points I would like to add.

1. There is no dearth of mentors or resources for one to improve one’s financial health. But the issue is when will one decide? Till 2006 I was literally dreading finance. I never understood my pay-slip though I was envying some of my colleagues who used to go and fight even if a rupee was short from their salary.

Then (by God’s grace) I took up MBA and started understanding finance and more importantly the importance of finance. At the same time there was a minor scam that happened in an organisation which opened my eyes to the reality. This is the trigger which galvanised me to improve my financial knowledge muscle. Now how does one get that trigger. I have no idea. This is the one that is lacking and not resources or mentors.

2. I try to pass on this info(my limited knowledge) to many relatives and friends freely from 2010-13. Many say thanks after their immediate issue is resolved and that is the end. They will not broach the subject with me till the next issue comes up. Then the cycle repeats. This is similar to the exercise regimen of many.

There is a important concept in behavioral psychology which is ” Irrational Human behavior”. Many think human behavior is rational. But there were many studies to prove it to be not very rational in many day to day circumstance. This can be seen in daily affairs. One cannot resist temptation to unhealthy foods and avoids healthy exercise.

Thus one needs to understand the issue(lack of one’s interest) and work on it before advises(like this), books or mentors can improve upon.

Those are some very good points you have added 🙂 . Thanks

I hope you don’t start fighting over a rupee like some your colleagues just because you have now taken an active interest in personal finance. Personal finance is important but its certainly not the be all and end all to be fighting over a penny.

I can’t speak for everyone here but to me its not important to be rich or ultra financially. Ultimately what matters is whether you feel rich or not and one can actually feel rich even with very meagre income and savings. There is so much more to life than just money. Think about it.

You make valid points. Developing healthy financial habits is important as developing any other habit. Quick fixes only go so far.

Awesome post… Thanks guys…

Welcome !

The advice given in this article is actually the advice of Robert Kiyosaki author of ‘Rich Dad Poor Dad’ and other books which give financial advice. I don’t know about how the website quora works, but at least credit should be given to the original by writing the source / reference used while giving the answer.

The advice is certainly good but I would suggest readers to read one of Robert Kiyosaki books on investing if they want to learn in more detail of the subject. I have personally read two of his book and both were quite excellent.

Thanks for that point Nishant . As the original content was from someone else, we could just put the same thing or dont put anything .

Manish

Nishant, you are correct. I have mentioned in the comments in the original Quora thread thread that I have read his books and some of the answer is inspired from him.

Awesome post thats what i want to hear!!!

right now m on 24 and earning good bucks, i feel that i lost my 2 years as investor :P. life is too short start investment as early as possible!!

and you remind me Robert Kiyosaki!!!

Thanks for sharing that !

Glad you enjoyed the answer Jaimin. I read Robert’s books myself and some of the answer is definitely inspired from it.

Nice article,

I am also a firm believer that saving does not make one rich, correct investment does.

But for a 22 year old I would say the first lesson should be How to Respect money.

Thanks for sharing

Yea , thats correct Anshul ! . Do you have some ideas on how can one teach a young person to respect money ?

I can go at length on this, but that will be a repetition of what I have learned from you guys!!

But still I have some pointers:

1> As soon as one starts earning he/she should stop taking money from parents.

2> Don’t envy others for materialistic things. (I have tried explaining this to others, the most common thing I say is ” You don’t need an iPhone, you want one!) :”No offense to iphone users”.

3> One should start his financial life with the very first pay check, it doesn’t matter if you invest 500Rs.

4> Start slow, may be with a recurring of 500Rs

5> Be realistic with your goals.

6> Most important: Read the articles on Jagoinvester.com 😛 it helps!!

Thanks for those points 🙂

That was an excellent post.Though it was an answer to 22 yr old but holds true for any age.Thanks Manish and Yuvraj for sharing it with us.

( Sharing too is a good way to learn and relearn things 🙂 ) Keep up the good work guys.

Thanks,

Suhas

Yea , its actually correct for all age group people !

Glad you liked the answer Suhas.